HSBC 2001 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2001 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

108

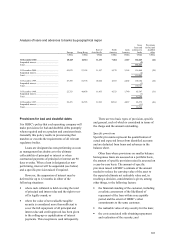

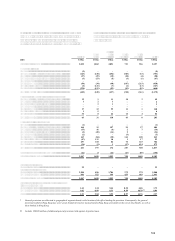

Provisions against loans and advances to

customers

31 December 31 Decembe

r

2001 2000

%%

Total provisions to gross lending*

Specific provisions........................... 1.90 2.17

General provisions

held against Argentine risk............ 0.21

other.............................................. 0.71 0.75

Total provisions ............................... 2.82 2.92

* Net of suspended interest, reverse repo transactions and

settlement accounts.

Risk elements in the loan portfolio

The SEC requires disclosure of credit risk elements

under the following headings that reflect US

accounting practice and classifications:

• loans accounted for on a non-accrual basis;

• accruing loans contractually past due 90 days or

more as to interest or principal; and

• troubled debt restructurings not included in the

above.

HSBC, however, classifies loans in accordance

with UK accounting practice which differs from US

practice as follows:

Suspended interest

Under the UK Statement of Recommended Practice

on Advances, UK banks continue to charge interest

on doubtful debts where there is a realistic prospect

of recovery. This interest is credited to a suspense

account and is not included in the profit and loss

account. In the United States, loans on which interest

has been accrued but suspended would be included

in risk elements as loans accounted for on a non-

accrual basis.

Assets acquired in exchange for advances

Under US GAAP, assets acquired in exchange for

advances in order to achieve an orderly realisation

are usually reported in a separate balance sheet

category, Owned Real Estate. Under UK GAAP,

these assets are reported within loans and advances.

Troubled debt restructurings

US GAAP requires separate disclosure of any loans

whose terms have been modified due to problems

with the borrower. Such disclosures may be

discontinued after the first year if the new terms were

in line with market conditions at the time of the

restructuring and the borrower has remained current

with the new terms.

In addition, US banks typically write off

problem lending more quickly than is the practice in

the United Kingdom. This practice means that

HSBCs reported level of credit risk elements is

likely to be higher than for a comparable US bank.

Potential problem loans

Credit risk elements also cover potential problem

loans. These are loans where known information

about possible credit problems of borrowers causes

management serious doubts as to the borrowers

ability to comply with the loan repayment terms. At

31 December 2001, all loans and advances in

Argentina, and all cross-border loans to Argentina,

which were not included as part of total risk elements

have been designated as potential problem loans.

There were no other significant potential problem

loans at 31 December 2001.

31 December 31 Decembe

r

2001 2000

US$m US$

m

Non-performing loans and

advances*

Banks.................................... 923

Customers............................. 9,649 10,372

Total non-performing loans and

advances .......................... 9,658 10,395

Total provisions cover as a

percentage of non-performing

loans and advances .......... 84.7% 78.9%

*Net of suspended interest.

Total non-performing loans to customers

decreased by US$723 million during 2001. At 31

December 2001, non-performing loans represented

3.0 per cent of total lending compared with 3.5 per

cent at 31 December 2000.

Underlying credit quality remained stable both

in the UK and in France although there was some

weakening of business confidence.

In Hong Kong, non-performing loans decreased

by US$494 million during 2001. This reflected the

impact of write-offs and recoveries, some

improvement in the corporate loan book offset

partially by an increase in delinquency in personal

lending.

In the Rest of Asia-Pacific, non-performing

loans decreased by US$356 million during 2001,

mainly due to the recovery achieved on the historical

Olympia & York loans.

The level of non-performing loans in North

America remained largely unchanged