HSBC 2001 Annual Report Download - page 252

Download and view the complete annual report

Please find page 252 of the 2001 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

HSBC HOLDINGS PLC

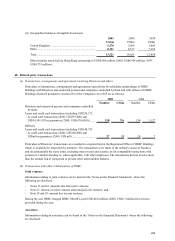

Notes on the Financial Statements (continued)

250

UK GAAP US GAAP

Interest rate swaps are also used to alter synthetically

the interest rate characteristics of financial instruments.

In order to qualify for synthetic alteration, a derivative

instrument must be linked to specific individual, or

pools of similar, assets or liabilities by the notional

principal and interest rate risks of the associated

instruments, and must achieve a result that is consistent

with defined risk management objectives. If these

criteria are met, accrual based accounting is applied,

i.e. income or expense is recognised and accrued to the

next settlement date in accordance with the contractual

terms of the agreement.

– For net investment hedges, in which derivatives

hedge the foreign currency exposure of a net

investment in a foreign operation, the change in

fair value of the derivative associated with the

effective portion of the hedge is included as a

component of other comprehensive income,

together with the associated loss or gain on the

hedged item. The ineffective portion is reported in

earnings immediately.

For a derivative not designated as a hedging

instrument, the gain or loss is recognised in

earnings in the period of change in fair value.

Any gain or loss arising on the termination of a

qualifying derivative is deferred and amortised to

earnings over the original life of the terminated

contract. Where the underlying asset, liability or

position is sold or terminated, the qualifying derivative

is immediately marked-to-market through the profit

and loss account.

Derivatives that do not qualify as hedges or synthetic

alterations at inception are marked-to-market through

the profit and loss account, with gains and losses

included within ‘Dealing profits’ .

The effect of adoption of SFAS 133 is treated as a

change in accounting principles.

Own shares held

UK GAAP allows for the inclusion of own shares held

within equity shares.

AICPA Accounting Research Bulletin 51

‘Consolidated Financial Statements’ requires a

reduction in shareholders’ equity for own shares held.

Dividends payable

Dividends declared after the period end are recorded in

the period to which they relate.

Dividends are recorded in the period in which they are

declared.