HSBC 2001 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2001 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

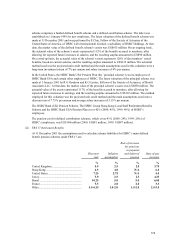

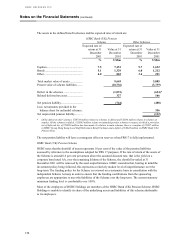

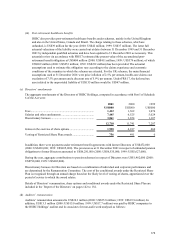

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

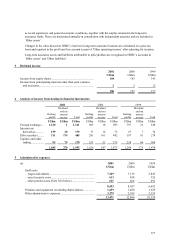

166

the costs of a continuing service to, or risk borne for, the customer, or is interest in nature. In these cases, it is

recognised on an appropriate basis over the relevant period.

(b) Loans and advances and doubtful debts

It is HSBC’ s policy that each operating company will make provisions for bad and doubtful debts promptly

where required and on a prudent and consistent basis.

Loans are designated as non-performing as soon as management has doubts as to the ultimate collectibility of

principal or interest or when contractual payments of principal or interest are 90 days overdue. When a loan is

designated as non-performing, interest will be suspended (see below) and a specific provision raised if required.

However, the suspension of interest may exceptionally be deferred for up to 12 months past due in the following

situations:

− where cash collateral is held covering the total of principal and interest due and the right of set-off is

legally sound; or

− where the value of net realisable tangible security is considered more than sufficient to cover the full

repayment of all principal and interest due and credit approval has been given to the rolling-up or

capitalisation of interest payments.

There are two basic types of provision, specific and general, each of which is considered in terms of the charge

and the amount outstanding.

Specific provisions

Specific provisions represent the quantification of actual and expected losses from identified accounts and are

deducted from loans and advances in the balance sheet.

Other than where provisions on smaller balance homogenous loans are assessed on a portfolio basis, the amount

of specific provision raised is assessed on a case by case basis. The amount of specific provision raised is HSBC’ s

conservative estimate of the amount needed to reduce the carrying value of the asset to the expected ultimate net

realisable value, and in reaching a decision consideration is given, among other things, to the following factors:

− the financial standing of the customer, including a realistic assessment of the likelihood of repayment of

the loan within an acceptable period and the extent of HSBC’ s other commitments to the same customer;

− the realisable value of any security for the loan;

− the costs associated with obtaining repayment and realisation of the security; and

− if loans are not in local currency, the ability of the borrower to obtain the relevant foreign currency.

Where specific provisions are raised on a portfolio basis, the level of provisioning takes into account

management’ s assessment of the portfolio's structure, past and expected credit losses, business and economic

conditions, and any other relevant factors. The principal portfolios evaluated on this basis are credit cards and

other consumer lending products.

General provisions

General provisions augment specific provisions and provide cover for loans which are impaired at the balance

sheet date but which will not be identified as such until some time in the future. HSBC requires operating

companies to maintain a general provision which is determined taking into account the structure and risk

characteristics of each company’ s loan portfolio. Historical levels of latent risk are regularly reviewed by each

operating company to determine that the level of general provisioning continues to be appropriate. Where

entities operate in a significantly higher risk environment, an increased level of general provisioning will apply

taking into account local market conditions and economic and political factors. General provisions are deducted

from loans and advances to customers in the balance sheet.