HSBC 2001 Annual Report Download - page 246

Download and view the complete annual report

Please find page 246 of the 2001 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

244

− Notes 15 and 16: amounts due from associates;

− Note 22: interests in associates; principal associates and interests in loan capital; and

− Notes 28 and 29: amounts due to associates.

Pension funds

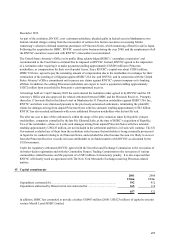

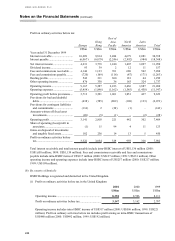

At 31 December 2001, US$12.5 billion (2000: US$14.0 billion) of HSBC pension fund assets were under

management by HSBC companies of which US$1,167 million (2000: US$1,195 million) is included in HSBC’ s

balance sheet under ‘Other assets’ in ‘Long-term assurance assets attributable to policyholders’ . Fees to HSBC

companies in connection with such management amounted to US$27 million (2000: US$27 million). HSBC’ s

pension funds had deposits of US$275 million (2000: US$303 million) with banking subsidiaries within HSBC.

49 UK and Hong Kong accounting requirements

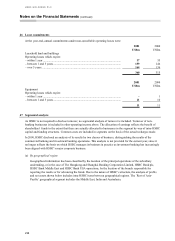

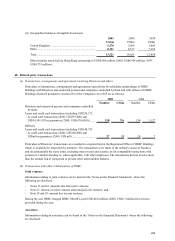

The financial statements have been prepared in accordance with UK accounting requirements; there would be no

material differences had they been prepared in accordance with Hong Kong Accounting Standards, except as set out

below.

The presentation of the cash flow statement is in accordance with Financial Reporting Standard 1 (revised 1996)

‘Cash Flow Statements’ rather than Hong Kong Statement of Standard Accounting Practice 15 ‘Cash Flow

Statements’ .

In accordance with Financial Reporting Standard 11 ‘Impairment of Fixed Assets and Goodwill’ , no charge has been

made in the profit and loss account in respect of those decreases in the valuation of HSBC properties that do not

represent impairments. If HSBC had prepared its financial statements under Hong Kong Statement of Standard

Accounting Practice 17 ‘Property, plant and equipment’ , there would have been a net charge to the profit and loss

account of US$38.9 million (2000: US$17 million) in respect of valuations below depreciated historical cost (of

which a credit of US$1.4 million (2000: US$1.4 million) relates to minority interests).

If HSBC had prepared its financial statements under Hong Kong Statement of Standard Accounting Practice 24

‘Accounting for Investments in Securities’ , US$419 million (2000: US$968 million) would have been credited to

reserves in respect of changes in the fair value of its long-term equity investments.

In accordance with Statement of Standard Accounting Practice 17 ‘Post balance sheet events’ , HSBC has recorded

dividends declared after the period end in the period to which they relate. If HSBC had prepared its financial

statements in accordance with Hong Kong Statement of Standard Accounting Practice 9 ‘Events after the balance

sheet date’ , dividends would be recorded in the period in which they are declared and there would have been an

increase in reserves at 31 December 2001 of US$2,700 million (at 31 December 2000: US$2,627 million).

HSBC Holdings has recorded its investment in HSBC undertakings at net asset value, including attributable

goodwill. If HSBC Holdings had prepared its individual financial statements in accordance with Hong Kong

Statement of Standard Accounting Practice 32 ‘Consolidated Financial Statements and Accounting for Investments

in Subsidiaries’ , and recorded its investment in HSBC undertakings at cost, there would have been a reduction in the

reserves of HSBC Holdings at 31 December 2001 of US$8,962 million (at 31 December 2000: US$8,466 million).

There would have been no impact on the consolidated financial statements of HSBC.