Entergy 2012 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2012 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

Entergy Corporation and Subsidiaries 2012

The annual long-term debt maturities (excluding lease obli-

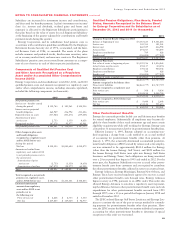

gations and long-term DOE obligations) for debt outstanding

as of December 31, 2012, for the next five years are as follows

(in thousands):

2013 $ 659,720

2014 $ 385,373

2015 $ 860,566

2016 $ 295,441

2017 $1,561,801

In November 2000, Entergy’s non-utility nuclear business pur-

chased the FitzPatrick and Indian Point 3 power plants in a seller-

financed transaction. Entergy issued notes to NYPA with seven annual

installments of approximately $108 million commencing one year

from the date of the closing, and eight annual installments of $20 mil-

lion commencing eight years from the date of the closing. These notes

do not have a stated interest rate, but have an implicit interest rate

of 4.8%. In accordance with the purchase agreement with NYPA,

the purchase of Indian Point 2 in 2001 resulted in Entergy becoming

liable to NYPA for an additional $10 million per year for 10 years,

beginning in September 2003. This liability was recorded upon the

purchase of Indian Point 2 in September 2001, and is included in

the note payable to NYPA balance above. In July 2003, a payment

of $102 million was made prior to maturity on the note payable to

NYPA. Under a provision in a letter of credit supporting these notes,

if certain of the Utility operating companies or System Energy were

to default on other indebtedness, Entergy could be required to post

collateral to support the letter of credit.

Entergy Gulf States Louisiana, Entergy Louisiana, Entergy

Mississippi, Entergy Texas, and System Energy have obtained long-

term financing authorizations from the FERC that extend through

July 2013. Entergy Arkansas has obtained long-term financing

authorization from the APSC that extends through December 2015.

Entergy New Orleans has obtained long-term financing authorization

from the City Council that extends through July 2014.

Capital Funds Agreement

Pursuant to an agreement with certain creditors, Entergy Corpora-

tion has agreed to supply System Energy with sufficient capital to:

n maintain System Energy’s equity capital at a minimum of 35% of

its total capitalization (excluding short-term debt);

n permit the continued commercial operation of Grand Gulf;

n pay in full all System Energy indebtedness for borrowed money

when due; and

n enable System Energy to make payments on specific System

Energy debt, under supplements to the agreement assigning System

Energy’s rights in the agreement as security for the specific debt.

Entergy Arkansas Debt Issuances

In January 2013, Entergy Arkansas arranged for the issuance by

(i) Independence County, Arkansas of $45 million of 2.375% Pol-

lution Control Revenue Refunding Bonds (Entergy Arkansas, Inc.

Project) Series 2013 due January 2021, and (ii) Jefferson County,

Arkansas of $54.7 million of 1.55% Pollution Control Revenue

Refunding Bonds (Entergy Arkansas, Inc. Project) Series 2013 due

October 2017, each of which series is secured by a separate series of

non-interest bearing first mortgage bonds of Entergy Arkansas. The

proceeds of these issuances were applied to the refunding of outstand-

ing series of pollution control revenue bonds previously issued by the

respective issuers.

Entergy Arkansas Securitization Bonds

In June 2010, the APSC issued a financing order authorizing the issu-

ance of bonds to recover Entergy Arkansas’s January 2009 ice storm

damage restoration costs, including carrying costs of $11.5 million

and $4.6 million of up-front financing costs. In August 2010, Entergy

Arkansas Restoration Funding, LLC, a company wholly-owned and

consolidated by Entergy Arkansas, issued $124.1 million of storm cost

recovery bonds. The bonds have a coupon of 2.30% and an expected

maturity date of August 2021. Although the principal amount is not

due until the date given above, Entergy Arkansas Restoration Funding

expects to make principal payments on the bonds over the next five

years in the amount of $12.6 million for 2013, $12.8 million for 2014,

$13.2 million for 2015, $13.4 million for 2016, and $13.8 million for

2017. With the proceeds, Entergy Arkansas Restoration Funding pur-

chased from Entergy Arkansas the storm recovery property, which is

the right to recover from customers through a storm recovery charge

amounts sufficient to service the securitization bonds. The storm

recovery property is reflected as a regulatory asset on the consolidated

Entergy Arkansas balance sheet. The creditors of Entergy Arkansas do

not have recourse to the assets or revenues of Entergy Arkansas Resto-

ration Funding, including the storm recovery property, and the credi-

tors of Entergy Arkansas Restoration Funding do not have recourse to

the assets or revenues of Entergy Arkansas. Entergy Arkansas has no

payment obligations to Entergy Arkansas Restoration Funding except

to remit storm recovery charge collections.

Entergy Louisiana Securitization Bonds – Little Gypsy

In August 2011, the LPSC issued a financing order authorizing the

issuance of bonds to recover Entergy Louisiana’s investment recovery

costs associated with the cancelled Little Gypsy repowering project.

In September 2011, Entergy Louisiana Investment Recovery Fund-

ing I, L.L.C., a company wholly-owned and consolidated by Entergy

Louisiana, issued $207.2 million of senior secured investment recov-

ery bonds. The bonds have an interest rate of 2.04% and an expected

maturity date of June 2021. Although the principal amount is not

due until the date given above, Entergy Louisiana Investment Recov-

ery Funding expects to make principal payments on the bonds over

the next five years in the amounts of $16.6 million for 2013, $21.9

million for 2014, $20.5 million for 2015, $21.6 million for 2016,

and $21.7 million for 2017. With the proceeds, Entergy Louisiana

Investment Recovery Funding purchased from Entergy Louisiana

the investment recovery property, which is the right to recover from

customers through an investment recovery charge amounts suffi-

cient to service the bonds. In accordance with the financing order,

Entergy Louisiana will apply the proceeds it received from the sale

of the investment recovery property as a reimbursement for previ-

ously-incurred investment recovery costs. The investment recovery

property is reflected as a regulatory asset on the consolidated Entergy

Louisiana balance sheet. The creditors of Entergy Louisiana do not

have recourse to the assets or revenues of Entergy Louisiana Invest-

ment Recovery Funding, including the investment recovery property,

and the creditors of Entergy Louisiana Investment Recovery Funding

do not have recourse to the assets or revenues of Entergy Louisiana.

Entergy Louisiana has no payment obligations to Entergy Louisiana

Investment Recovery Funding except to remit investment recovery

charge collections.

Entergy Texas Securitization Bonds – Hurricane Rita

In April 2007, the PUCT issued a financing order authorizing the

issuance of securitization bonds to recover $353 million of Entergy

Texas’s Hurricane Rita reconstruction costs and up to $6 million of

transaction costs, offset by $32 million of related deferred income

tax benefits. In June 2007, Entergy Gulf States Reconstruction Fund-

ing I, LLC, a company that is now wholly-owned and consolidated

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS continued

81