Entergy 2012 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2012 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112

|

|

Entergy Corporation and Subsidiaries 2012

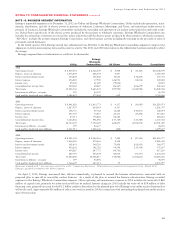

NOTE 17. DECOMMISSIONING TRUST FUNDS

Entergy holds debt and equity securities, classified as available-for-

sale, in nuclear decommissioning trust accounts. The NRC requires

Entergy subsidiaries to maintain trusts to fund the costs of decom-

missioning ANO 1, ANO 2, River Bend, Waterford 3, Grand Gulf,

Pilgrim, Indian Point 1 and 2, Vermont Yankee, and Palisades (NYPA

currently retains the decommissioning trusts and liabilities for Indian

Point 3 and FitzPatrick). The funds are invested primarily in equity

securities, fixed-rate fixed-income securities, and cash and cash

equivalents.

Entergy records decommissioning trust funds on the balance sheet

at their fair value. Because of the ability of the Registrant Subsidiaries

to recover decommissioning costs in rates and in accordance with the

regulatory treatment for decommissioning trust funds, the Registrant

Subsidiaries have recorded an offsetting amount of unrealized gains/

(losses) on investment securities in other regulatory liabilities/assets.

For the nonregulated portion of River Bend, Entergy Gulf States

Louisiana has recorded an offsetting amount of unrealized gains/

(losses) in other deferred credits. Decommissioning trust funds for

Pilgrim, Indian Point 1 and 2, Vermont Yankee, and Palisades do not

meet the criteria for regulatory accounting treatment. Accordingly,

unrealized gains recorded on the assets in these trust funds are recog-

nized in the accumulated other comprehensive income component of

shareholders’ equity because these assets are classified as available for

sale. Unrealized losses (where cost exceeds fair market value) on the

assets in these trust funds are also recorded in the accumulated other

comprehensive income component of shareholders’ equity unless the

unrealized loss is other than temporary and therefore recorded in

earnings. Generally, Entergy records realized gains and losses on its

debt and equity securities using the specific identification method to

determine the cost basis of its securities.

The securities held as of December 31, 2012 and 2011 are

summarized as follows (in millions):

Total Total

Fair Unrealized Unrealized

Value Gains Losses

2012

Equity securities $2,459 $662 $ 1

Debt securities 1,731 116 5

Total $4,190 $778 $ 6

2011

Equity securities $2,129 $423 $14

Debt securities 1,659 115 5

Total $3,788 $538 $19

Deferred taxes on unrealized gains/(losses) are recorded in other

comprehensive income for the decommissioning trusts which do not

meet the criteria for regulatory accounting treatment as described

above. Unrealized gains/(losses) above are reported before deferred

taxes of $211 million and $149 million as of December 31, 2012

and 2011, respectively. The amortized cost of debt securities was

$1,637 million as of December 31, 2012 and $1,530 million as of

December 31, 2011. As of December 31, 2012, the debt securities

have an average coupon rate of approximately 3.78%, an average

duration of approximately 5.43 years, and an average maturity of

approximately 8.50 years. The equity securities are generally held

in funds that are designed to approximate or somewhat exceed the

return of the Standard & Poor’s 500 Index. A relatively small per-

centage of the securities are held in funds intended to replicate the

return of the Wilshire 4500 Index or the Russell 3000 Index.

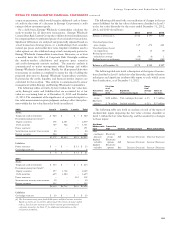

The fair value and gross unrealized losses of available-for-sale

equity and debt securities, summarized by investment type and length

of time that the securities have been in a continuous loss position, are

as follows as of December 31, 2012 (in millions):

Equity Securities Debt Securities

Gross Gross

Fair Unrealized Fair Unrealized

Value Losses Value Losses

Less than 12 months $37 $1 $175 $1

More than 12 months 20 – 48 4

Total $57 $1 $223 $5

The fair value and gross unrealized losses of available-for-sale

equity and debt securities, summarized by investment type and length

of time that the securities have been in a continuous loss position, are

as follows as of December 31, 2011 (in millions):

Equity Securities Debt Securities

Gross Gross

Fair Unrealized Fair Unrealized

Value Losses Value Losses

Less than 12 months $130 $ 9 $123 $3

More than 12 months 43 5 60 2

Total $173 $14 $183 $5

The unrealized losses in excess of twelve months on equity

securities above relate to Entergy’s Utility operating companies and

System Energy.

The fair value of debt securities, summarized by contractual matur-

ities, as of December 31, 2012 and 2011 are as follows (in millions):

2012 2011

Less than 1 year $ 53 $ 69

1 year - 5 years 681 566

5 years - 10 years 562 583

10 years - 15 years 164 187

15 years - 20 years 61 42

20 years+ 210 212

Total $1,731 $1,659

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS continued

104