ComEd 2002 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2002 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

The cessation of the amortization of negative goodwill of

AmerGen on January 1, 2002 did not have a material impact on

Exelon’s reported net income for 2002.

EITF Issue 02-3

In the third quarter of 2002,Exelon and Generation adopted the

provision of EITF Issue 02-3, “Accounting for Contracts Involved

in Energy Trading and Risk Management Activities” (EITF 02-3)

issued by the FASB EITF in June 2002 that requires revenues and

energy costs related to energy trading contracts to be presented

on a net basis in the income statement. Prior to the adoption,

revenues from trading activity were presented in Revenue and

the energy costs related to energy trading were presented

as either Purchased Power or Fuel expense on Exelon and

Generation’s Consolidated Statements of Income. For compara-

tive purposes, energy costs related to energy trading have been

reclassified in prior periods to revenue to conform to the net

basis of presentation required by EITF 02-3. Exelon commenced

trading activities in April 2001, as such $207 million of pur-

chased power expense and $15 million of fuel expense, respec-

tively, was reclassified and reflected as a reduction to revenue

for the year ended December 31, 2001.

SFAS No. 144

In September 2001,the FASB issued SFAS No.144,“Accounting for

the Impairment or Disposal of Long-Lived Assets”(SFAS No.144).

Exelon adopted SFAS No. 144 on January 1, 2002. SFAS No. 144

establishes accounting and reporting standards for both the

impairment and disposal of long-lived assets. SFAS No. 144 is

effective for fiscal years beginning after December 15, 2001 and

its provisions are generally applied prospectively. The adoption

of SFAS No. 144 had no effect on Exelon’s reported financial

position, results of operations or cash flows.

SFAS No. 145

In April 2002, the FASB issued SFAS No. 145, “Rescission of FASB

Statements No. 4, 44 and 64, Amendment of FASB Statement

No. 13, and Technical Corrections” (SFAS No. 145). SFAS No. 145

eliminates SFAS No. 4 “Reporting Gains and Losses from

Extinguishment of Debt”and thus allows for only those gains or

losses on the extinguishment of debt that meet the criteria of

extraordinary items to be treated as such in the financial state-

ments. SFAS No. 145 also amends Statement of Financial

Accounting Standards No. 13,“Accounting for Leases” to require

sale-leaseback accounting for certain lease modifications that

have economic effects that are similar to sale-leaseback trans-

actions.The adoption of SFAS No. 145 required a reclassification

of the 2000 extraordinary item of $4 million, net of income

taxes, to interest expense;otherwise,it had no effect on Exelon’s

reported financial position or cash flows.

SFAS No. 133

SFAS No. 133 applies to all derivative instruments and requires

that such instruments be recorded on the balance sheet either

as an asset or a liability measured at their fair value through

earnings,with special accounting permitted for certain qualify-

ing hedges. On January 1, 2001, Exelon adopted SFAS No. 133.

Generation recognized a non-cash gain of $12 million, net of

income taxes, in earnings and deferred a non-cash gain of $4

million, net of income taxes,in accumulated other comprehen-

sive income and PECO deferred a non-cash gain of $40 million,

net of income taxes, in accumulated other comprehensive

income.

Nuclear Outage Costs

During the fourth quarter of 2000, as a result of the synchro-

nization of accounting policies with Unicom in connection with

the Merger,PECO changed its method of accounting for nuclear

outage costs to record such costs as incurred. Previously, PECO

accrued these costs over the operating unit cycle. As a result of

the change in accounting method for nuclear outage costs,

PECO recorded income of $24 million, net of income taxes of

$16 million. The change is reported as a cumulative effect of a

change in accounting principle on the Consolidated Statements

of Income as of December 31, 2000, representing the balance of

the nuclear outage cost reserve at January 1, 2000.

SFAS No. 148

In December 2002, the FASB issued SFAS No. 148, “Accounting

for Stock-Based Compensation—Transition and Disclosure—

an amendment of FASB Statement No. 123” (SFAS No. 148). SFAS

No. 148 provides alternative methods of transition for a volun-

tary change to the fair value based method of accounting for

stock-based employee compensation and requires disclosures

in both annual and interim financial statements regarding the

method of accounting for stock-based compensation and the

effect of the method on financial results. SFAS No. 148 is effec-

tive for financial statements for fiscal years ending after

December 15,2002.As of December 31,2002,Exelon has adopted

the additional disclosure requirements of SFAS No.148 and con-

tinues to account for its stock-compensation plans under the

disclosure only provision of SFAS No.123.

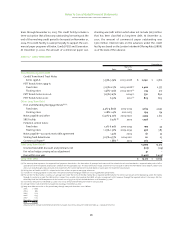

Changes in Accounting Estimates

Effective July 1, 2002, ComEd decreased its depreciation rates

based on a new depreciation study reflecting its significant con-

struction program in recent years,changes in and development

of new technologies, and changes in estimated plant service

lives since the last depreciation study.The annualized reduction

in depreciation expense, based on December 31, 2001 plant bal-

ances, is estimated to be approximately $100 million ($60 mil-

lion, net of income taxes). As a result of the change, net income

Notes To Consolidated Financial Statements

exelon corporation and subsidiary companies

91