ComEd 2002 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2002 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

58

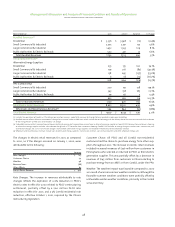

We account for derivative financial instruments under SFAS

No.133.To the extent thatchanges in SFAS No.133 modify current

guidance, including the standards for determining whether

contracts can be accounted for as normal purchases and normal

sales,the accounting treatment for derivatives may change.

We are required under SFAS No. 133 to record derivative

instruments at fair value. Depending on the designation of the

derivative, the fair value is either recorded in the income state-

ment or as a component of other comprehensive income in

shareholders’ equity (OCI). We use quoted exchange prices to

the extent they are available or external broker quotes in order

to determine the fair value of energy contracts.When external

prices are not available, we use internal models to determine

the fair value.These internal models include assumptions of the

future prices of energy based on the specific energy market the

energy is being purchased in using externally available forward

market pricing curves for all periods possible under the pricing

model. We use the Black model, a standard industry valuation

model, to determine the fair value of energy derivative con-

tracts that are marked-to-market.To determine the fair value of

our outstanding interest rate swap agreements we use external

broker quotes or calculate the fair value internally using the

Bloomberg swap valuation tool. This tool uses the most recent

market inputs and a widely accepted valuation methodology.

During 2002,Generation recognized unrealized and realized

net gains of $6 million and $20 million, respectively, relating

to mark-to-market adjustments of certain non-trading power

purchase and sale contracts pursuant to SFAS No. 133 and

unrealized and realized net losses aggregating $9 million and

$20 million, respectively, relating to mark-to-market adjustments

of derivative instruments entered into for trading purposes.

Hedge Accounting. As part of our energy marketing business,

we enter into contracts to purchase or sell electricity, gas and

ancillary products such as transmission rights,congestion credits

and emission allowances, using contracts that are considered

derivatives under SFAS No. 133. Certain of these derivatives

qualify as hedge transactions.

A derivative instrument can be designated as a hedge of the

fair value of a recognized asset or liability or of an unrecognized

firm commitment (fair value hedge) or a hedge of a forecasted

transaction or the variability of cash flows to be received or paid

related to a recognized asset or liability (cash flow hedge). To

qualify for hedge accounting, the fair value changes in the

derivative must be expected to offset 80%-120% of the changes

in fair value or cash flows of the hedged item. Changes in the

fair value of a derivative that is designated and qualifies as a

fair value hedge and is highly effective, along with the gain or

loss on the hedged asset or liability that is attributable to the

hedged risk, are recorded in earnings. Changes in the fair value

of a derivative that is designated as and qualifies as a cash flow

hedge and is highly effective,are recorded in OCI,until earnings

are affected by the variability of cash flows being hedged.

Exelon continually assesses these cash flow hedges to deter-

mine if they continue to be effective and that the forecasted

future transaction is probable.At the point in time that the con-

tract does not meet the effective or probable criteria of SFAS No.

133, hedge accounting is discontinued and the fair value of the

derivative is recorded through earnings.

Energy Contracts. We enter into contracts designated as cash

flow hedges in which we manage the variability of our cash

flows related to the purchase or sale of energy. At the initiation

of the contract the contract is identified as a cash flow hedge,

which requires us to determine whether the contract is in

accordance with our RMP, that the forecasted future transac-

tion is probable,and that the hedging relationship between the

energy contract and the expected future purchase or sale of

energy is expected to be highly effective at the initiation of

the hedge and throughout the hedging relationship. Internal

models that measure the statistical correlation between the

derivative and the associated hedged item determine the

effectiveness of an energy contract designated as a hedge. An

example of a contract that would qualify for hedge accounting

would be a forward over-the-counter sales contract used to

hedge an expected sale of generation exposed to market prices.

Interest Rate Derivative Instruments. We enter into interest rate

swap contracts related to variable rate debt in order to convert

the variable interest payments into fixed interest payments to

manage the variability of cash flows.Additionally,we enter into

forward starting interest rate swaps in order to lock in an interest

rate at a future date in anticipation of a future debt issuance to

manage the variability of changes in interest rates between the

date of the decision to issue and the actual date of issue.

We also enter into interest rate swap contracts related to

fixed rate debt in order to maintain our targeted percentage of

variable rate debt.

The fair value of derivatives generally reflects the estimated

amounts that we would receive or pay to terminate the

contracts at the balance sheet date,thereby taking into account

the current unrealized gains or losses of open contracts.

Normal Purchases and Normal Sales Exemption. As part of our

energy marketing business,we enter into contracts to purchase

or sell electricity, gas and ancillary products such as transmis-

sion rights, congestion credits and emission allowances using

contracts that are considered derivatives under SFAS No. 133.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

exelon corporation and subsidiary companies