Washington Post 2013 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2013 Washington Post annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

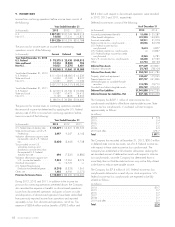

|

|

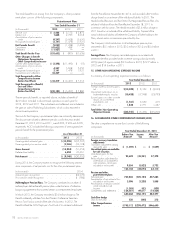

the consolidated U.S. Federal tax return filing considered the only major

tax jurisdiction. The statute of limitations has expired on all consolidated

U.S. Federal corporate income tax returns filed through 2009, and the

Internal Revenue Service is not currently examining any of the post-2009

returns filed by the Company.

The Company endeavors to comply with tax laws and regulations

where it does business, but cannot guarantee that, if challenged, the

Company’s interpretation of all relevant tax laws and regulations will

prevail and that all tax benefits recorded in the financial statements will

ultimately be recognized in full. The Company has taken reasonable

efforts to address uncertain tax positions and has determined that there

are no material transactions and no material tax positions taken by the

Company that would fail to meet the more-likely-than-not threshold for

recognizing transactions or tax positions in the financial statements.

Accordingly, the Company has not recorded a reserve for uncertain

tax positions in the financial statements, and the Company does not

expect any significant tax increase or decrease to occur within the next

12 months with respect to any transactions or tax positions taken and

reflected in the financial statements. In making these determinations, the

Company presumes that taxing authorities pursuing examinations of the

Company’s compliance with tax law filing requirements will have full

knowledge of all relevant information, and, if necessary, the Company

will pursue resolution of disputed tax positions by appeals or litigation.

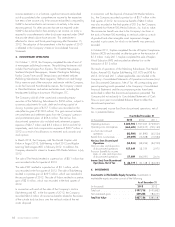

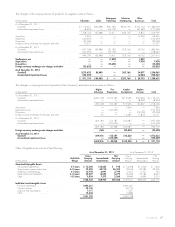

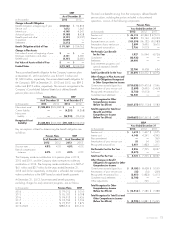

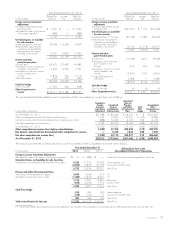

10. DEBT

The Company’s borrowings consist of the following:

As of December 31

(in thousands) 2013 2012

7.25% unsecured notes due

February 1, 2019 ............... $397,893 $ 397,479

USD Revolving credit borrowing ....... —240,121

AUD Revolving credit borrowing ....... 44,625 51,915

Other indebtedness ................ 8,258 7,196

Total Debt ....................... 450,776 696,711

Less: current portion ................ (3,168) (243,327)

Total Long-Term Debt ............... $447,608 $ 453,384

The Company did not borrow funds under its USD revolving credit facility

in 2013. On December 20, 2012, the Company borrowed $240

million under its revolving credit facility at an interest rate of 1.5107%;

this was fully repaid on January 11, 2013. The Company’s other

indebtedness at December 31, 2013, is at interest rates of 0% to 6%

and matures between 2014 and 2017.

In January 2009, the Company issued $400 million in unsecured ten-

year fixed-rate notes due February 1, 2019 (the Notes). The Notes

have a coupon rate of 7.25% per annum, payable semiannually on

February 1 and August 1. Under the terms of the Notes, unless the

Company has exercised its right to redeem the Notes, the Company

is required to offer to repurchase the Notes in cash at 101% of the

principal amount, plus accrued and unpaid interest, upon the occurr-

ence of both a Change of Control and Below Investment Grade Rating

Events as described in the Prospectus Supplement of January 27, 2009.

On June 17, 2011, the Company entered into a credit

agreement (the Credit Agreement) providing for a U.S. $450

million, AUD 50 million four-year revolving credit facility (the

Facility) with each of the lenders party thereto, JPMorgan Chase

Bank,N.A.asAdministrativeAgent,andJ.P.MorganAustralia

Limited as Australian Sub-Agent. The Facility consists of two

tranches: (a) U.S. $450 million and (b) AUD 50 million (subject,

at the Company’s option, to conversion of the unused Australian

dollar commitments into U.S. dollar commitments at a specified

exchange rate). The Credit Agreement provides for an option to

increase the total U.S. dollar commitments up to an aggregate

amount of U.S. $700 million. The Company is required to pay a

facility fee on a quarterly basis, based on the Company’s long-

term debt ratings, of between 0.08% and 0.20% of the amount

of the Facility. Any borrowings are made on an unsecured basis

and bear interest at (a) for U.S. dollar borrowings, at the

Company’s option, either (i) a fluctuating interest rate equal to the

highest of JPMorgan’s prime rate, 0.5% above the Federal funds

rate or the one-month eurodollar rate plus 1%, or (ii) the

eurodollar rate for the applicable interest period; or (b) for

Australian dollar borrowings, the bank bill rate, in each case plus

an applicable margin that depends on the Company’s long-term

debt ratings. The Facility will expire on June 17, 2015, unless

the Company and the banks agree to extend the term. Any

outstanding borrowings must be repaid on or prior to the final

termination date. The Credit Agreement contains terms and

conditions, including remedies in the event of a default by the

Company, typical of facilities of this type and, among other

things, requires the Company to maintain at least $1.5 billion of

consolidated stockholders’ equity.

On September 7, 2011, the Company borrowed AUD 50 million

under its revolving credit facility. On the same date, the Company

entered into interest rate swap agreements with a total notional value of

AUD 50 million and a maturity date of March 7, 2015. These interest

rate swap agreements will pay the Company variable interest on the

AUD 50 million notional amount at the three-month bank bill rate, and

the Company will pay the counterparties a fixed rate of 4.5275%.

These interest rate swap agreements were entered into to convert the

variable rate Australian dollar borrowing under the revolving credit

facility into a fixed rate borrowing. Based on the terms of the interest

rate swap agreements and the underlying borrowing, these interest rate

swap agreements were determined to be effective and thus qualify as a

cash flow hedge. As such, any changes in the fair value of these interest

rate swaps are recorded in other comprehensive income on the

accompanying condensed consolidated balance sheets until earnings

are affected by the variability of cash flows.

During 2013 and 2012, the Company had average borrowings

outstanding of approximately $471.4 million and $483.3 million,

respectively, at average annual interest rates of approximately

6.7%. The Company incurred net interest expense of $33.8 million,

$32.6 million and $29.1 million during 2013, 2012 and 2011,

respectively. At December 31, 2013 and 2012, the fair value of

the Company’s 7.25% unsecured notes, based on quoted market

prices, totaled $475.2 million and $481.4 million, respectively,

compared with the carrying amount of $397.9 million and $397.5

million. The carrying value of the Company’s other unsecured debt

at December 31, 2013, approximates fair value.

70 GRAHAM HOLDINGS COMPANY