Washington Post 2013 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2013 Washington Post annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

The Company’s borrowings at December 31, 2013, are mostly

from $400.0 million of 7.25% unsecured notes due February 1,

2019, and AUD 50 million revolving credit borrowings; the interest

on $400.0 million of 7.25% unsecured notes is payable semi-

annually on February 1 and August 1. The Company did not have

any outstanding commercial paper borrowing or USD revolving

credit borrowing as of December 31, 2013. The Company’s

borrowings at December 31, 2012, are mostly from $400.0 million

of 7.25% unsecured notes due February 1, 2019, $240.1 million

in USD revolving credit borrowings and AUD 50 million revolving

credit borrowings. The Company fully repaid the $240 million USD

revolving credit borrowing on January 11, 2013.

On June 17, 2011, the Company entered into a credit agreement

(the Credit Agreement) providing for a U.S. $450 million, AUD

50 million four-year revolving credit facility (the Facility) with each of

the lenders party thereto, JPMorgan Chase Bank, N.A. as

Administrative Agent, and J.P. Morgan Australia Limited as Australian

Sub-Agent. The Credit Agreement provides for an option to increase

the total U.S. dollar commitments up to an aggregate amount of U.S.

$700 million. The Facility will expire on June 17, 2015, unless the

Company and the banks agree to extend the term.

On September 7, 2011, the Company borrowed AUD 50 million

under its revolving credit facility. On the same date, the Company

entered into interest rate swap agreements with a total notional

value of AUD 50 million and a maturity date of March 7, 2015.

These interest rate swap agreements will pay the Company variable

interest on the AUD 50 million notional amount at the three-month

bank bill rate, and the Company will pay the counterparties a fixed

rate of 4.5275%. These interest rate swap agreements were

entered into to convert the variable rate Australian dollar borrowing

under the revolving credit facility into a fixed rate borrowing. Based

on the terms of the interest rate swap agreements and the underlying

borrowing, these interest rate swap agreements were determined to

be effective and thus qualify as a cash flow hedge. As such, any

changes in the fair value of these interest rate swaps are recorded

in other comprehensive income on the accompanying condensed

consolidated balance sheets until earnings are affected by the

variability of cash flows.

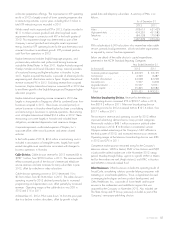

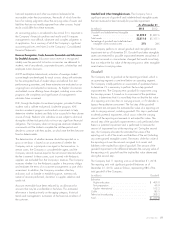

In September 2013, Standard & Poor’s affirmed the Company’s

“BBB” long-term corporate debt rating and changed the outlook

from Negative to Stable. In addition, S&P upgraded the Company’s

short-term corporate debt rating from “A-3” to “A-2.” The Company’s

current credit ratings are as follows:

Moody’s Standard

& Poor’s

Long-term ........................... Baa1 BBB

Short-term ........................... Prime-2 A-2

During 2013 and 2012, the Company had average borrowings

outstanding of approximately $471.4 million and $483.3 million,

respectively, at average annual interest rates of approximately

6.7%. The Company incurred net interest expense of $33.8 million

and $32.6 million, respectively, during 2013 and 2012.

At December 31, 2013 and 2012, the Company had working

capital of $768.3 million and $327.5 million, respectively. The

Company maintains working capital levels consistent with its

underlying business requirements and consistently generates cash

from operations in excess of required interest or principal payments.

The Company’s net cash provided by operating activities, as

reported in the Company’s Consolidated Statements of Cash Flows,

was $327.9 million in 2013, compared to $477.2 million in

2012. The decline is largely due to an increase in income tax

payments in 2013 and expenses incurred related to the sale of the

Publishing Subsidiaries.

In November 2013, the Company announced that its headquarters

building was to be sold for approximately $159 million. The sale is

currently expected to close at the end of March 2014.

The Company expects to fund its estimated capital needs primarily

through existing cash balances and internally generated funds and,

to a lesser extent, borrowings under its revolving credit facility. In

management’s opinion, the Company will have ample liquidity to

meet its various cash needs in 2014.

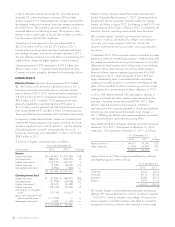

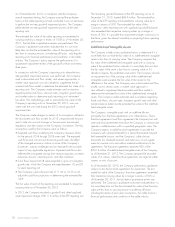

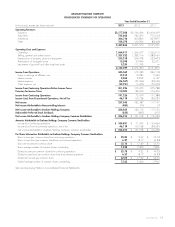

The following reflects a summary of the Company’s contractual

obligations as of December 31, 2013:

(in thousands) 2014 2015 2016 2017 2018 Thereafter Total

Debt and

interest .... $ 35,168$ 79,750$ 29,000$ 29,000$ 29,000$414,500 $ 616,418

Programming

purchase

commitments (1) 180,825 108,804 90,723 15,969 5,888 — 402,209

Operating

leases ..... 119,129 106,041 99,167 88,119 73,520 411,466 897,442

Other

purchase

obligations (2) 118,187 56,704 32,505 10,392 4,050 4,005 225,843

Long-term

liabilities (3) 7,052 6,484 6,284 6,107 5,848 39,693 71,468

Total ..... $460,361 $357,783 $257,679 $149,587 $118,306 $869,664 $2,213,380

(1) Includes commitments for the Company’s television broadcasting and cable businesses that are

reflected in the Company’s Consolidated Financial Statements and commitments to purchase

programming to be produced in future years.

(2) Includes purchase obligations related to employment agreements, capital projects and other

legally binding commitments. Other purchase orders made in the ordinary course of business

are excluded from the table above. Any amounts for which the Company is liable under

purchase orders are reflected in the Company’s Consolidated Balance Sheets as accounts

payable and accrued liabilities.

(3) Primarily made up of postretirement benefit obligations other than pensions. The Company has

other long-term liabilities excluded from the table above, including obligations for deferred

compensation, long-term incentive plans and long-term deferred revenue.

Other. The Company does not have any off-balance-sheet

arrangements or financing activities with special-purpose entities

(SPEs). Transactions with related parties, as discussed in Note 4 to

the Company’s Consolidated Financial Statements, are in the

ordinary course of business and are conducted on an arm’s-length

basis.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation of financial statements in conformity with generally

accepted accounting principles requires management to make

estimates and judgments that affect the amounts reported in the

financial statements. On an ongoing basis, the Company evaluates

its estimates and assumptions. The Company bases its estimates on

48 GRAHAM HOLDINGS COMPANY