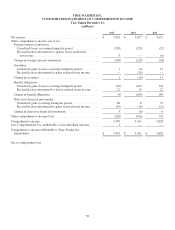

Time Magazine 2015 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2015 Time Magazine annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

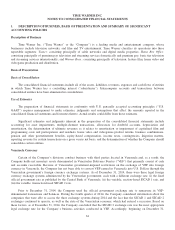

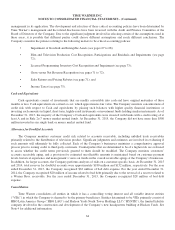

TIME WARNER INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

and 50% criteria are not satisfied (e.g., if there is a plan to sell the security in the near term and the fair value is below the

Company’s cost basis).

For investments accounted for using the cost or equity method of accounting, the Company evaluates information

available (e.g., budgets, business plans, financial statements, etc.) in addition to quoted market prices, if any, in determining

whether an other-than-temporary decline in value exists. Factors indicative of an other-than-temporary decline include

recurring operating losses, credit defaults and subsequent rounds of financing at an amount below the cost basis of the

Company’s investment. For more information, see Note 4.

Goodwill and Indefinite-Lived Intangible Assets

Goodwill and indefinite-lived intangible assets, primarily tradenames, are tested annually for impairment as of

December 31 or earlier upon the occurrence of certain events or substantive changes in circumstances. Goodwill is tested for

impairment at the reporting unit level. A reporting unit is either the “operating segment level,” such as Warner Bros.

Entertainment Inc. (“Warner Bros.”), Home Box Office, Inc. (“Home Box Office”) and Turner Broadcasting System, Inc.

(“Turner”), or one level below, which is referred to as a “component” (e.g., Warner Bros. Theatrical, Warner Bros.

Television). The level at which the impairment test is performed requires judgment as to whether the components constitute a

self-sustaining business and, if so, whether their operations are similar such that they should be aggregated for purposes of

the impairment test. For purposes of the goodwill impairment test, management has concluded that the operations below the

operating segment level met the criteria to be aggregated and therefore has determined its reporting units are the same as its

operating segments.

In assessing Goodwill for impairment, the Company has the option to first perform a qualitative assessment to

determine whether the existence of events or circumstances leads to a determination that it is more likely than not that the

fair value of a reporting unit is less than its carrying amount. If the Company determines that it is not more likely than not

that the fair value of a reporting unit is less than its carrying amount, the Company is not required to perform any additional

tests in assessing Goodwill for impairment. However, if the Company concludes otherwise or elects not to perform the

qualitative assessment, then it is required to perform the first step of a two-step impairment review process. The first step of

the two-step process involves a comparison of the estimated fair value of a reporting unit to its carrying amount. In

performing the first step, the Company determines the fair value of a reporting unit using a discounted cash flow (“DCF”)

analysis and, in certain cases, a combination of a DCF analysis and a market-based approach. Determining fair value requires

the exercise of significant judgment, including judgments about appropriate discount rates, perpetual growth rates, the

amount and timing of expected future cash flows, as well as relevant comparable public company earnings multiples. The

cash flows employed in the DCF analyses are based on the Company’s most recent budgets and long range plans and

perpetual growth rates are assumed for years beyond the current long range plan period. Discount rate assumptions are based

on an assessment of market rates, capital structures and the risk inherent in the future cash flows included in the budgets and

long range plans.

In 2015, the Company did not elect to perform a qualitative assessment of Goodwill and instead performed a

quantitative impairment test. The results of the quantitative test did not result in any impairments of Goodwill because the

fair values of each of the Company’s reporting units exceeded their respective carrying values. None of the carrying values

of the Company’s reporting units were within 30% of their respective fair values as of December 31, 2015. If the carrying

value of a reporting unit exceeded its fair value, the second step of the impairment review process would need to be

performed to determine the ultimate amount of impairment loss to record. Significant assumptions utilized in the DCF

analysis included discount rates that ranged from 9.0% to 9.5% and a terminal revenue growth rate of 3.25%. Significant

assumptions utilized in the market-based approach were market EBITDA multiples ranging from 9.5x to 10.0x for the

Company’s reporting units where a market-based approach was performed.

In assessing other intangible assets not subject to amortization for impairment, the Company also has the option to

perform a qualitative assessment to determine whether the existence of events or circumstances leads to a determination that

it is more likely than not that the fair value of such an intangible asset is less than its carrying amount. If the Company

determines that it is not more likely than not that the fair value of such an intangible asset is less than its carrying amount,

67