Time Magazine 2015 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2015 Time Magazine annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

|

|

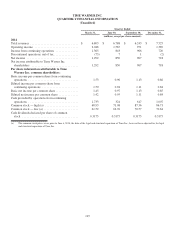

TIME WARNER INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS - (Continued)

Contingencies

In the ordinary course of business, the Company and its subsidiaries are defendants in or parties to various legal claims,

actions and proceedings. These claims, actions and proceedings are at varying stages of investigation, arbitration or

adjudication, and involve a variety of areas of law.

On April 4, 2007, the National Labor Relations Board (“NLRB”) issued a complaint against CNN America Inc. (“CNN

America”) and Team Video Services, LLC (“Team Video”) related to CNN America’s December 2003 and January 2004

terminations of its contractual relationships with Team Video, under which Team Video had provided electronic news

gathering services in Washington, DC and New York, NY. The National Association of Broadcast Employees and

Technicians, under which Team Video’s employees were unionized, initially filed charges of unfair labor practices with the

NLRB in February 2004, alleging that CNN America and Team Video were joint employers, that CNN America was a

successor employer to Team Video, and/or that CNN America discriminated in its hiring practices to avoid becoming a

successor employer or due to specific individuals’ union affiliation or activities. In the complaint, the NLRB sought, among

other things, the reinstatement of certain union members and monetary damages. On November 19, 2008, the presiding

NLRB Administrative Law Judge (“ALJ”) issued a non-binding recommended decision and order finding CNN America

liable. On September 15, 2014, a three-member panel of the NLRB affirmed the ALJ’s decision and adopted the ALJ’s order

with certain modifications. On November 12, 2014, both CNN America and the NLRB General Counsel filed motions with

the NLRB for reconsideration of the panel’s decision. On March 20, 2015, the NLRB granted the NLRB General Counsel’s

motion for reconsideration to correct certain inadvertent errors in the panel’s decision, and it denied CNN America’s motion

for reconsideration. On July 9, 2015, CNN America filed a notice of appeal with the U.S. Court of Appeals for the D.C.

Circuit regarding the panel’s decision and the denial of CNN America’s motion for reconsideration.

In April 2013, the Internal Revenue Service (the “IRS”) Appeals Division issued a notice of deficiency to the Company

relating to the appropriate tax characterization of stock warrants received from Google Inc. in 2002. On May 6, 2013, the

Company filed a petition with the United States Tax Court seeking a redetermination of the deficiency set forth in the

notice. The Company’s petition asserted that the IRS erred in determining that the stock warrants were taxable upon exercise

(in 2004) rather than at the date of grant based on, among other things, a misapplication of Section 83 of the Internal

Revenue Code. In December 2014, the Company reached a preliminary agreement with the IRS, subject to agreement

regarding certain necessary computations and the preparation and execution of definitive documentation. In February 2016,

the parties reached a final agreement to resolve the issues raised in the notice of deficiency.

The Company establishes an accrued liability for legal claims when the Company determines that a loss is both

probable and the amount of the loss can be reasonably estimated. Once established, accruals are adjusted from time to time,

as appropriate, in light of additional information. The amount of any loss ultimately incurred in relation to matters for which

an accrual has been established may be higher or lower than the amounts accrued for such matters.

For matters disclosed above for which a loss is probable or reasonably possible, the Company has estimated a range of

possible loss. The Company believes the estimate of the aggregate range of possible loss for such matters in excess of

accrued liabilities is between $0 and $130 million at December 31, 2015. The estimated aggregate range of possible loss is

subject to significant judgment and a variety of assumptions. The matters represented in the estimated aggregate range of

possible loss will change from time to time and actual results may vary significantly from the current estimate.

In view of the inherent difficulty of predicting the outcome of litigation and claims, the Company often cannot predict

what the eventual outcome of the pending matters will be, what the timing of the ultimate resolution of these matters will be,

or what the eventual loss, fines or penalties related to each pending matter may be. An adverse outcome in one or more of

these matters could be material to the Company’s results of operations or cash flows for any particular reporting period.

111