Starwood 2007 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2007 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

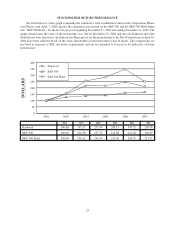

|

|

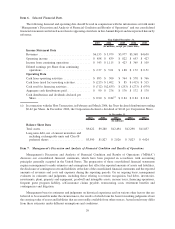

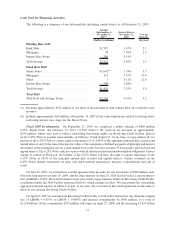

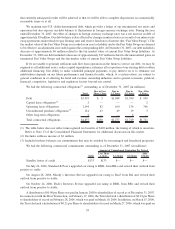

cash used to fund our operating expenses, interest payments on debt, capital expenditures, dividend payments and

share repurchases. Our day-to-day operations are financed through a net working capital deficit, a practice that is

common in our industry. The ratio of our current assets to current liabilities was 0.87 and 0.74 as of December 31,

2007 and 2006, respectively. Consistent with industry practice, we sweep the majority of the cash at our hotels on a

daily basis and fund payables as needed by drawing down on our existing revolving credit facility. We believe that

our existing borrowing availability together with capacity for additional borrowings and cash from operations will

be adequate to meet all funding requirements for our operating expenses, principal and interest payments on debt,

capital expenditures, dividend payments and share repurchases in the foreseeable future.

State and local regulations governing sales of VOIs and residential properties allow the purchaser of such a

VOI or property to rescind the sale subsequent to its completion for a pre-specified number of days. In addition, cash

payments received from buyers of products under construction are held in escrow during the period prior to

obtaining a certificate of occupancy. These payments and the deposits collected from sales during the rescission

period are the primary components of our restricted cash balances in our consolidated balance sheets. At

December 31, 2007 and 2006, we had short-term restricted cash balances of $196 million and $329 million,

respectively.

Cash From Investing Activities

In limited cases, we have made loans to owners of or partners in hotel or resort ventures for which we have a

management or franchise agreement. Loans outstanding under this program, excluding the Westin Boston, Seaport

Hotel discussed below, totaled $34 million at December 31, 2007. We evaluate these loans for impairment, and at

December 31, 2007, believe these loans are collectible. Unfunded loan commitments aggregating $69 million were

outstanding at December 31, 2007, of which $1 million are expected to be funded in 2008 and $51 million are

expected to be funded in total. These loans typically are secured by pledges of project ownership interests and/or

mortgages on the projects. We also have $100 million of equity and other potential contributions associated with

managed or joint venture properties, $28 million of which is expected to be funded in 2008.

During 2004, we entered into a long-term management contract to manage the Westin Boston, Seaport Hotel in

Boston, Massachusetts, which opened in June 2006. In connection with this project, we agreed to provide up to

$28 million in mezzanine loans and other investments (all of which was funded). In January 2007, this hotel was

sold and the senior debt was repaid in full. In connection with this sale, the $28 million in mezzanine loans and other

investments, together with accrued interest, were repaid in full. In accordance with the management agreement, the

sale of the hotel also resulted in the payment of a fee to us of approximately $18 million, which is included in

management fees, franchise fees and other income in the consolidated statement of income for the year ended

December 31, 2007. We continue to manage this hotel subject to the pre-existing management agreement.

Surety bonds issued on our behalf at December 31, 2007 totaled $99 million, the majority of which were

required by state or local governments relating to our vacation ownership operations and by our insurers to secure

large deductible insurance programs.

To secure management contracts, we may provide performance guarantees to third-party owners. Most of these

performance guarantees allow us to terminate the contract rather than fund shortfalls if certain performance levels

are not met. In limited cases, we are obliged to fund shortfalls in performance levels through the issuance of loans.

At December 31, 2007, excluding the Le Méridien management agreement mentioned below, we had six

management contracts with performance guarantees with possible cash outlays of up to $74 million, $50 million

of which, if required, would be funded over several years and would be largely offset by management fees received

under these contracts. Many of the performance tests are multi-year tests, are tied to the results of a competitive set

of hotels, and have exclusions for force majeure and acts of war and terrorism. We do not anticipate any significant

funding under these performance guarantees in 2008. In connection with the Le Méridien Acquisition, discussed

below, we assumed the obligation to guarantee certain performance levels at one Le Méridien managed hotel for the

periods 2007 through 2013. This guarantee is uncapped. However, we have estimated the exposure under this

guarantee and do not anticipate that payments made under the guarantee will be significant in any single year. The

estimated present fair value of this guarantee of $7 million and $6 million is reflected in other liabilities in the

35