Sears 2011 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2011 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

|

|

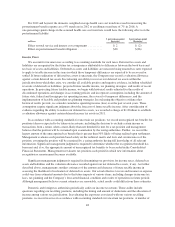

For 2012 and beyond, the domestic weighted-average health care cost trend rates used in measuring the

postretirement benefit expense are a 9% trend rate in 2012 to an ultimate trend rate of 7% in 2016. A

one-percentage-point change in the assumed health care cost trend rate would have the following effects on the

postretirement liability:

millions

1 percentage-point

Increase

1 percentage-point

Decrease

Effect on total service and interest cost components .......... $ 2 $ (2)

Effect on postretirement benefit obligation ................. $30 $(26)

Income Taxes

We account for income taxes according to accounting standards for such taxes. Deferred tax assets and

liabilities are recognized for the future tax consequences attributable to differences between the book basis and

tax basis of assets and liabilities. Deferred tax assets and liabilities are measured using enacted tax rates expected

to apply to taxable income in the years in which those temporary differences are expected to be recovered or

settled. If future utilization of deferred tax assets is uncertain, the Company may record a valuation allowance

against certain deferred tax assets. In evaluating our ability to recover our deferred tax assets within the

jurisdiction from which they arise, we consider all available positive and negative evidence, including scheduled

reversals of deferred tax liabilities, projected future taxable income, tax planning strategies, and results of recent

operations. In projecting future taxable income, we begin with historical results adjusted for the results of

discontinued operations and changes in accounting policies and incorporate assumptions including the amount of

future state, federal and foreign pre-tax operating income, the reversal of temporary differences, and the

implementation of feasible and prudent tax planning strategies. In evaluating the objective evidence that

historical results provide, we consider cumulative operating income (loss) over the past several years. These

assumptions require significant judgment about the forecasts of future taxable income. After consideration of

evidence regarding the ability to realize our deferred tax assets, we recorded a charge of $1.8 billion to establish

a valuation allowance against certain deferred income tax assets in 2011.

In accordance with accounting standards for uncertain tax positions, we record unrecognized tax benefits for

positions taken or expected to be taken on tax returns, including the decision to exclude certain income or

transactions from a return, when a more-likely-than-not threshold is met for a tax position and management

believes that the position will be sustained upon examination by the taxing authorities. Further, we record the

largest amount of the unrecognized tax benefit that is greater than 50% likely of being realized upon settlement.

Management evaluates each position based solely on the technical merits and facts and circumstances of the

position, assuming the position will be examined by a taxing authority having full knowledge of all relevant

information. Significant management judgment is required to determine whether the recognition threshold has

been met and, if so, the appropriate amount of unrecognized tax benefits to be recorded in the Consolidated

Financial Statements. Management reevaluates tax positions each period in which new information about

recognition or measurement becomes available.

Significant management judgment is required in determining our provision for income taxes, deferred tax

assets and liabilities and the valuation allowance recorded against our net deferred tax assets, if any. As further

described above, management considers estimates of the amount and character of future taxable income in

assessing the likelihood of realization of deferred tax assets. Our actual effective tax rate and income tax expense

could vary from estimated amounts due to the future impacts of various items, including changes in income tax

laws, tax planning and the Company’s forecasted financial condition and results of operations in future periods.

Although management believes current estimates are reasonable, actual results could differ from these estimates.

Domestic and foreign tax authorities periodically audit our income tax returns. These audits include

questions regarding our tax filing positions, including the timing and amount of deductions and the allocation of

income among various tax jurisdictions. In evaluating the exposures associated with our various tax filing

positions, we record reserves in accordance with accounting standards for uncertain tax positions. A number of

48