Sears 2011 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2011 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

|

|

include actuarial estimates of both claims filed and carried at their expected ultimate settlement value and claims

incurred but not yet reported. Our estimated claim amounts are discounted using a rate with a duration that

approximates the duration of our self-insurance reserve portfolio. Our liability reflected on the Consolidated

Balance Sheets represents an estimate of the ultimate cost of claims incurred at the balance sheet date. In

estimating this liability, we utilize loss development factors based on Company-specific data to project the future

development of incurred losses. Loss estimates are adjusted based upon actual claims settlements and reported

claims. These projections are subject to a high degree of variability based upon future inflation rates, litigation

trends, legal interpretations, benefit level changes and claim settlement patterns. Although we do not expect the

amounts ultimately paid to differ significantly from our estimates, self-insurance reserves could be affected if

future claim experience differs significantly from the historical trends and the actuarial assumptions.

Defined Benefit Retirement Plans

The fundamental components of accounting for defined benefit retirement plans consist of the compensation

cost of the benefits earned, the interest cost from deferring payment of those benefits into the future and the

results of investing any assets set aside to fund the obligation. Such retirement benefits were earned by associates

ratably over their service careers. Therefore, the amounts reported in the income statement for these retirement

plans have historically followed the same pattern. Accordingly, changes in the obligations or the value of assets

to fund them have been recognized systematically and gradually over the associate’s estimated period of service.

The largest drivers of losses or charges in recent years have been the discount rate used to determine the present

value of the obligation and the actual return on pension assets. We recognize the changes by amortizing

experience gains/losses in excess of the 10% corridor into expense over the associate service period and by

recognizing the difference between actual and expected asset returns over a five-year period.

Holdings’ actuarial valuations utilize key assumptions including discount rates and expected returns on plan

assets. We are required to consider current market conditions, including changes in interest rates and plan asset

investment returns, in determining these assumptions. Actuarial assumptions may differ materially from actual

results due to changing market and economic conditions, changes in investment strategies, higher or lower

withdrawal rates, and longer or shorter life spans of participants.

The Investment Committee, made up of select members of senior management, has appointed a

non-affiliated third party professional to advise the Committee with respect to the SHC domestic pension plan

assets. The plan’s overall investment objective is to provide a long-term return that, along with Company

contributions, is expected to meet future benefit payment requirements. A long-term horizon has been adopted in

establishing investment policy such that the likelihood and duration of investment losses are carefully weighed

against the long-term potential for appreciation of assets. The plan’s investment policy requires investments to be

diversified across individual securities, industries, market capitalization and valuation characteristics. In addition,

various techniques are utilized to monitor, measure and manage risk.

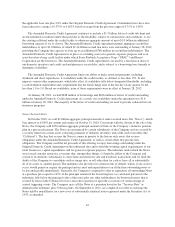

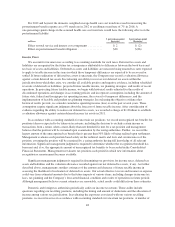

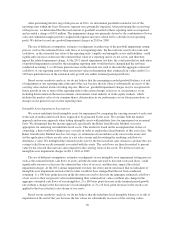

For purposes of determining the periodic expense of our defined benefit plans, we use the fair value of plan

assets as the market related value. A one-percentage-point change in the assumed discount rate would have the

following effects on the pension liability:

millions

1 percentage-point

Increase

1 percentage-point

Decrease

Effect on interest cost component ........................ $ 28 $(37)

Effect on pension benefit obligation ...................... $(771) $935

47