Sears 2006 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2006 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

SEARS HOLDINGS CORPORATION

Notes to Consolidated Financial Statements—(Continued)

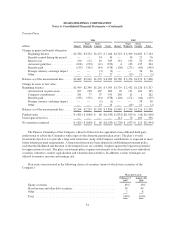

continues to believe that all of the Company’s pre-petition net deferred tax assets will more likely than not be

realized, due to the Merger and the actual and forecasted levels of profitability, and as such the related valuation

allowance has been reduced to zero at January 28, 2006. In accordance with SFAS No. 109, the portion of the

reversal of the valuation allowance attributable to the Merger ($1,073 million) has been recorded as an

adjustment to goodwill attributable to the Merger. In accordance with SOP 90-7, the remaining portion of the

reversal of the valuation allowance is recorded as a direct credit to capital in excess of par.

In connection with the Merger, deferred tax assets of $350 million were recorded related to state net

operating losses (“NOLs”) of Sears. A valuation allowance of $330 million was recorded with respect to this

deferred tax asset. As a result, the Company recognized a net deferred tax asset of $20 million in conjunction

with the initial purchase price allocation related to the Merger. During fiscal 2006, the Company recorded an

additional net $2 million valuation allowance with respect to this deferred tax asset, resulting in a total valuation

allowance of $332 million as of the end of fiscal 2006. In addition, during fiscal 2006, the deferred tax asset for

the Sears NOL decreased by $3 million to $347 million. The Company will continue to assess the likelihood of

realization of these state deferred tax assets and will reduce the valuation allowance on such assets in the future if

it becomes more likely than not that the net deferred tax assets will be utilized. To the extent that these valuation

allowances are reversed in the future, such effects would be recorded as a decrease to goodwill.

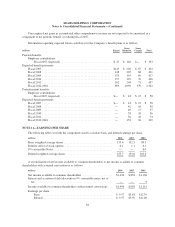

During fiscal 2006, fiscal 2005, and fiscal 2004, the Company reduced its reserves for Predecessor

Company income tax liabilities by $3.5 million, $1 million, and $56 million, respectively, primarily due to

favorable claims settlements. In fiscal years 2006, 2005 and 2004, the Company also received a tax benefit of $4

million, $91 million and $67 million, respectively, relating to certain Class 5 and 6 pre-petition claims paid with

equity. Additionally, in fiscal 2006, the Company increased its deferred tax assets by $126.5 million for income

tax settlements. In accordance with SOP 90-7, subsequent to emergence from Chapter 11, any benefit realized

from an adjustment to pre-confirmation income tax liabilities is recorded as an addition to Capital in excess of

par value.

As a result of reaching various income tax audit settlements during fiscal 2006 pertaining to pre-Merger

periods, the Company reduced approximately $196 million of tax liabilities with an offsetting credit recorded to

goodwill. In accordance with SFAS No. 109, resolution of these matters result in a direct credit to Merger-related

goodwill.

In connection with the reorganization, Kmart Corporation realized income from the cancellation of certain

indebtedness. Although this income was not taxable, as it resulted from reorganization under the Bankruptcy

Code, the Company was required to reduce certain of its tax attributes (NOL carryforwards by $3,743 million,

general business credit carryforwards by $45 million, AMT credit carryforwards by $111 million and basis of

certain assets by $902 million) in an amount equal to the cancellation of indebtedness. The reorganization of

Kmart Corporation on the Effective Date resulted in an ownership change under section 382 of the Internal

Revenue Code and accordingly, the use of any of the Company’s NOL carryforwards and tax credits generated

prior to the ownership change, as well as certain subsequently recognized “built-in” losses, if any, existing as of

the date of the ownership change that are not reduced pursuant to the provisions discussed above, will be subject

to an overall annual limitation of $96 million.

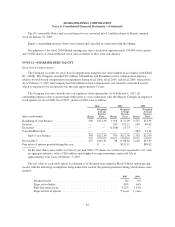

At February 3, 2007, the Company had federal and Canadian NOL carryforwards of approximately

$408 million and $163 million, generating deferred tax assets of approximately $143 million and $56 million,

respectively. The federal NOL carryforwards will expire in 2021, 2022 and 2023. The Canadian NOL

carryforwards will expire in 2015. The Company also has NOL carryforwards attributable to various states

generating deferred tax assets of $74 million which will predominantly expire between 2017 and 2026. The

Company also has credit carryforwards of $42 million which will expire by 2015.

90