Sears 2006 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2006 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

SEARS HOLDINGS CORPORATION

Notes to Consolidated Financial Statements—(Continued)

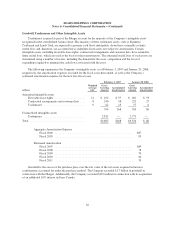

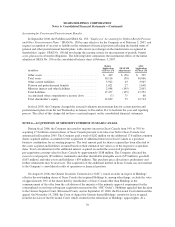

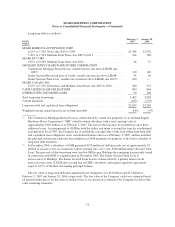

Changes in the carrying amount of goodwill by segment during fiscal 2006 are as follows:

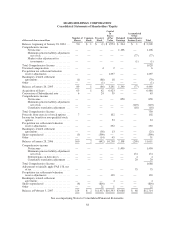

millions

Sears

Domestic

Sears

Canada Total

Balance, January 29, 2006 ................................... $1,585 $ 99 $1,684

Finalization of purchase accounting(1) ...................... 37 — 37

Acquisition of additional interest in Sears Canada ............. — 167 167

Tax settlements affecting Merger-related goodwill ............ (188) (8) (196)

Balance, February 3, 2007 ................................... $1,434 $258 $1,692

(1) The Company completed the purchase price allocation for the Merger during the first quarter of fiscal 2006.

As a result, goodwill attributable to the Merger increased by approximately $37 million, primarily based on

the receipt of additional information regarding the fair values of certain properties and certain pre-Merger

legal contingencies.

As the result of reaching various tax audit settlements during fiscal 2006 pertaining to pre-Merger periods,

the Company reduced approximately $196 million of tax liabilities with an offsetting credit recorded to goodwill.

In accordance with SFAS No. 109, “Accounting for Income Taxes,” resolution of these matters results in a direct

credit to Merger-related goodwill.

In accordance with SFAS No. 142, “Goodwill and Other Intangible Assets,” goodwill is not amortized but

requires testing for potential impairment, at a minimum on an annual basis, or when indications of potential

impairment exist. The impairment test for goodwill utilizes a fair value approach. The impairment test for

identifiable intangible assets not subject to amortization is also performed annually or when impairment

indications exist, and consists of a comparison of the fair value of the intangible asset with its carrying amount.

Identifiable intangible assets that are subject to amortization are evaluated for impairment using a process similar

to that used to evaluate other long-lived assets.

Financial Instruments and Hedging Activities

From time to time, the Company uses derivative financial instruments, including interest rate swaps and

caps to manage its exposure to movements in interest rates, and foreign currency forward contracts to hedge the

foreign currency exposure of its net investment in Sears Canada against adverse changes in exchange rates. In

addition, the Company has entered into a certain number of total return swaps as a means for investing a portion

of the Company’s surplus cash. The Company recognizes all derivative instruments at fair value within either

other assets or other liabilities on its consolidated balance sheet.

When applying hedge accounting treatment to its derivative transactions, the Company formally documents

its hedge relationships, including identification of the hedging instruments and the hedged items, as well as its

risk management objectives and strategies for undertaking the hedge transaction. The Company also formally

assesses, both at inception and at least quarterly thereafter, whether the derivatives that are used in hedging

transactions are highly effective in offsetting changes in either the fair value or cash flows of the hedged item. If

it is determined that a derivative ceases to be a highly effective hedge, the Company discontinues hedge

accounting.

For interest rate swaps and caps that have been designated and qualify as hedges, both the effective and

ineffective portions of the changes in the fair value of the derivative, along with the offsetting gain or loss on the

designated hedged item that is attributable to the hedged risk, are recognized in the consolidated statements of

63