Sears 2006 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2006 Sears annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

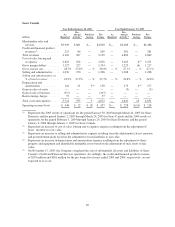

Contractual Obligations and Off-Balance-Sheet Arrangements

Information concerning the Company’s obligations and commitments to make future payments under

contracts such as debt and lease agreements, and under contingent commitments, is aggregated in the following

tables.

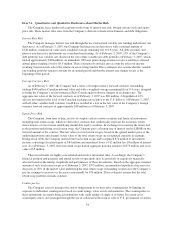

Payments Due by Period

Contractual Obligations Total

Within

1 Year

1-3

Years

4-5

Years

After 5

Years

millions

Operating leases ....................................... $ 7,023 $ 820 $1,390 $1,038 $3,775

Short-term debt ........................................ 95 95 — — —

Capital lease obligations ................................ 1,444 148 274 252 770

Royalty license fees(1) ................................... 273 187 66 13 7

Pension funding obligations .............................. 828 192 379 257 —

Long-term debt ........................................ 3,662 705 809 1,091 1,057

Total contractual obligations ............................. $13,325 $2,147 $2,918 $2,651 $5,609

(1) The Company pays royalties under various merchandise license agreements, which are generally based on

sales of products covered under these agreements. The Company currently has license agreements for which

it pays royalties, including those to use the Jaclyn Smith, Joe Boxer, and Martha Stewart Everyday

trademarks. Royalty license fees represent the minimum Holdings is obligated to pay, regardless of sales, as

guaranteed royalties under these license agreements.

Other Commercial Commitments

millions

Bank

Issued

SRAC

Issued Other Total

Standby letters of credit ............................................. $888 $119 $— $1,007

Commercial letters of credit .......................................... 71 178 — 249

Secondary lease obligations and performance guarantee .................... — — 90 90

Application of Critical Accounting Policies

In preparing the financial statements, certain accounting policies require considerable judgment to select the

appropriate assumptions to calculate financial estimates. These estimates are complex and subject to an inherent

degree of uncertainty. The Company bases its estimates on historical experience, terms of existing contracts,

evaluation of trends and other assumptions that the Company believes to be reasonable under the circumstances.

The Company continually evaluates the information used to make these estimates as its business and the

economic environment change. Although the use of estimates is pervasive throughout the financial statements,

the Company considers an accounting estimate to be critical if:

• it requires assumptions to be made about matters that were highly uncertain at the time the estimate

was made, and

• changes in the estimate that are reasonably likely to occur from period to period or different estimates

that could have been selected would have a material effect on the Company’s financial condition, cash

flows or results of operations.

Management believes the current assumptions and other considerations used to estimate amounts reflected

in the financial statements are appropriate. However, if actual experience differs from the assumptions and the

47