Rosetta Stone 2009 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2009 Rosetta Stone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

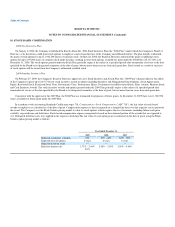

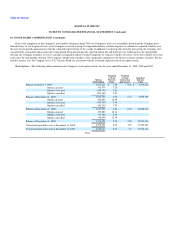

Table of Contents

ROSETTA STONE INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

statement. ASC 810 clarifies that changes in a parent's ownership interest in a subsidiary that do not result in deconsolidation are equity transactions if the

parent retains its controlling financial interest. In addition, this statement requires that a parent recognize a gain or loss in net income when a subsidiary is

deconsolidated. Such gain or loss will be measured using the fair value of the noncontrolling equity investment on the deconsolidation date. ASC 810 also

includes expanded disclosure requirements regarding the interests of the parent and its noncontrolling interest. ASC 810 is effective for fiscal years, and

interim periods within those fiscal years, beginning on or after December 15, 2008. Earlier adoption is prohibited. The adoption of ASC 810 did not have a

material impact on the Company's financial position, results of operations or cash flows.

In March 2008, the FASB issued Accounting Standards Codification topic 815, Derivatives and Hedging ("ASC 815"), which requires enhanced

disclosures about an entity's derivative and hedging activities. This Statement is effective for financial statements issued for fiscal years and interim periods

beginning after November 15, 2008. Entities are required to provide enhanced disclosures about (a) how and why an entity uses derivative instruments,

(b) how derivative instruments and related hedged items are accounted for and (c) how derivative instruments and related hedged items affect an entity's

financial position, financial performance and cash flows. The adoption of ASC 815 did not have a significant impact on the Company's financial position,

results of operations or cash flows.

In May 2008, the FASB issued Accounting Standards Codification topic ASC 105, Generally Accepted Accounting Principles, ("ASC 105"), which

identifies the sources of accounting principles and provides the framework for selecting the principles used in the preparation of financial statements of

nongovernmental entities that are presented in conformity with generally accepted accounting principles in the United States. ASC 105 is effective for

financial statements issued for fiscal years and interim periods beginning after November 15, 2008. The adoption of ASC 105 did not have significant impact

on the Company's financial position, results of operation, or cash flows.

On October 10, 2008, the FASB issued Accounting Standards Codification topic 820, Fair Value Measurements and Disclosures ("ASC 820"), which

was effective upon issuance, including periods for which financial statements have not been issued. ASC 820 provided an illustrative example to demonstrate

how the fair value of a financial asset is determined when the market for that financial asset is inactive. The adoption of ASC 820 did not have a material

impact on the Company's consolidated financial position and the results of operations.

In April 2009, the FASB issued Accounting Standards Codification topic 820-10-65-4, Fair Value Measurements and Disclosures ("ASC 820"), which

provides guidance on how to determine the fair value of assets and liabilities when the volume and level of activity for the asset or liability has significantly

decreased. ASC 820 also provides guidance on identifying circumstances that indicate a transaction is not orderly. In addition, ASC 820 requires disclosure in

interim and annual periods of the inputs and valuation methods used in determining fair value and a discussion of any changes in those valuation methods.

ASC 820 is effective for annual and interim periods ending on or after June 15, 2009. The adoption of ASC 820 did not have a material impact on the

Company's consolidated financial position and the results of operations.

On May 28, 2009, the FASB issued Accounting Standards Codification topic 855, Subsequent Events ("ASC 855"). Although ASC 855 does not

significantly change current practice surrounding the disclosure of subsequent events, it provides guidance on management's assessment of subsequent events

and the requirement to disclose the date through which subsequent events have been evaluated.

F-16