Panera Bread 2007 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2007 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

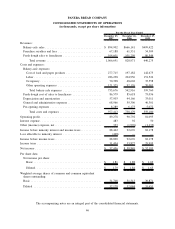

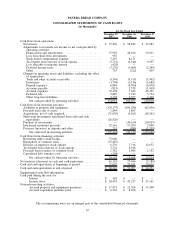

respectively. Annually, and whenever an event or circumstance indicates it is more likely than not our goodwill has

been impaired, management assesses the carrying value of our recorded goodwill. We perform our annual

impairment assessment on the first day of the fourth quarter of each year by comparing discounted cash flows

from reporting units with the carrying value of the underlying net assets inclusive of goodwill. In performing this

analysis, management considers such factors as current results, trends, future prospects and other economic factors.

As of December 25, 2007, the Company determined there was no impairment of goodwill. There can be no

assurance that future goodwill impairment tests will not result in a charge to earnings.

Self-Insurance

We are self-insured for a significant portion of our workers’ compensation, group health, and general, auto, and

property liability insurance with varying levels of deductibles of as much as $0.5 million of individual claims,

depending on the type of claim. We also purchase aggregate stop-loss and/or layers of loss insurance in many

categories of loss. We utilize third party actuarial experts’ estimates of expected losses based on statistical analyses

of historical industry data, as well as our own estimates based on our actual historical data to determine required

self-insurance reserves. The assumptions are closely reviewed, monitored, and adjusted when warranted by

changing circumstances. The estimated accruals for these liabilities could be affected if actual experience related to

the number of claims and cost per claim differs from these assumptions and historical trends. Based on information

known at December 25, 2007, we believe we have provided adequate reserves for our self-insurance exposure. As of

December 25, 2007 and December 26, 2006, self-insurance reserves were $8.9 million and $7.4 million, respec-

tively, and were included in accrued expenses in the accompanying Consolidated Balance Sheets.

Income Taxes

The provision for income taxes is determined in accordance with the provisions of SFAS No. 109, Accounting

for Income Taxes. Under this method, deferred tax assets and liabilities are recognized for the future tax

consequences attributable to differences between the financial statement carrying amounts of existing assets

and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted income

tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be

recovered or settled. Any effect on deferred tax assets and liabilities of a change in tax rates is recognized in income

in the period that includes the enactment date.

In July 2006, the FASB issued Interpretation No. 48, Accounting for Uncertainty in Income Taxes, or

FIN No. 48. FIN No. 48 clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s

financials in accordance with SFAS No. 109. FIN No. 48 prescribes a recognition threshold and measurement

attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a

tax return. This pronouncement also provides guidance on derecognition, classification, interest and penalties,

accounting in interim periods, disclosure, and transition. Effective December 27, 2006, we adopted FIN No. 48 and

have applied it to all income tax positions commencing from that date. The cumulative effect of applying the

provisions of FIN No. 48 was recorded as an adjustment to reduce the fiscal 2007 opening balance of retained

earnings in the Consolidated Balance Sheets as of December 27, 2006. We classify estimated interest and penalties

related to the underpayment of income taxes as a component of income tax expense in the Consolidated Statements

of Operations.

Prior to fiscal year 2007, we determined our tax contingencies in accordance with SFAS No. 5, Accounting for

Contingencies. We recorded estimated tax liabilities to the extent the contingencies were probable and could be

reasonably estimated.

Lease Obligations

We recognize rent expense on a straight-line basis over the reasonably assured lease period. Certain of our

lease agreements provide for scheduled rent increases during the lease terms or for rental payments commencing at

a date other than the date of initial occupancy. We include any rent escalations and construction and other rent

holidays in our straight-line rent expense. In addition, we record landlord allowances for non-structural tenant

improvements as deferred rent, which is included in accrued expenses or deferred rent in the Consolidated Balance

38