OfficeMax 2007 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2007 OfficeMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

payments do not include contingent rental payments that may be due based on a percentage of

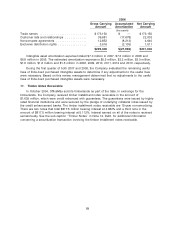

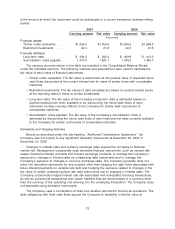

sales in excess of stipulated amounts. These future minimum lease payment requirements have not

been reduced by $62.3 million of minimum sublease rentals due in the future under noncancelable

subleases. These sublease rentals include amounts related to closed stores and other facilities that

are accounted for in the integration activities and facility closures reserve. See Note 3, Integration

Activities and Facility Closures.

The Company capitalizes lease obligations for which it assumes substantially all property rights

and risks of ownership. The Company did not have any material capital leases during any of the

periods presented.

8. Sales of Accounts Receivable

Prior to July 2007, the Company sold, on a revolving basis, an undivided interest in a defined

pool of receivables while retaining a subordinated interest in a portion of the receivables. The

Company continued servicing the sold receivables and charged the third party conduits a monthly

servicing fee at market rates. The program qualified for sale treatment under SFAS No. 140,

‘‘Accounting for Transfers and Servicing of Financial Assets and Extinguishment of Liabilities.’’ At

December 30, 2006, $180.0 million of sold accounts receivable were excluded from receivables in

the accompanying Consolidated Balance Sheets. The Company’s subordinated retained interest in

the transferred receivables was $111.2 million at December 30, 2006 and was included in

receivables, net in the Consolidated Balance Sheet. Expenses associated with the securitization

program totaled $5.6 million, $10.6 million and $5.5 million in 2007, 2006 and 2005, respectively.

These expenses relate primarily to the loss on sale of receivables and discount on retained

interests, facility fees and professional fees associated with the program, and were included in the

Consolidated Statements of Income (Loss).

On July 12, 2007, the Company entered into a new loan agreement that amended the

Company’s existing revolving credit facility and replaced the Company’s accounts receivable

securitization program. The transferred accounts receivable under the accounts receivable

securitization program at that date were refinanced with borrowings under the new loan agreement

and excess cash. The Company no longer sells any of its accounts receivable. For additional

information on the new loan agreement see Note 12, Debt.

9. Investments in Affiliates

In connection with the sale of the paper, forest products and timberland assets in 2004 (the

‘‘Sale’’), the Company invested $175 million in the equity units of affiliates of the buyer, Boise

Cascade, L.L.C. A portion (approximately $66 million) of the equity units received in exchange for

the Company’s investment carries no voting rights. This investment is accounted for under the cost

method as Boise Cascade, L.L.C. does not maintain separate ownership accounts for its members,

and the Company does not have the ability to significantly influence its operating and financial

policies. This investment is included in investment in affiliates in the Consolidated Balance Sheets.

The Company has determined that it is not practicable to estimate the fair value of this investment.

However, the Company did not observe any events or changes in circumstances that would have

had a significant adverse effect on the fair value of the investment.

The Boise Cascade, L.L.C. non-voting equity units accrue dividends daily at the rate of 8% per

annum on the liquidation value plus accumulated dividends. Dividends accumulate semiannually to

the extent not paid in cash on the last day of any June and December. The Company recognized

dividend income on this investment of $6.1 million in 2007, $5.9 million in 2006 and $5.5 million in

2005.

67