OfficeMax 2007 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2007 OfficeMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

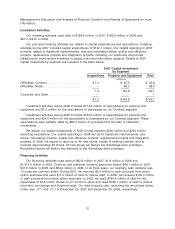

important new-year office supply restocking month of January, the back-to-school period and the

holiday selling season, respectively.

Disclosures of Financial Market Risks

Our debt is predominantly fixed-rate. At December 29, 2007, the estimated current market value

of our debt, based on quoted market prices when available or then-current interest rates for similar

obligations with like maturities, including the timber notes, was approximately $109.9 million greater

than the amount of debt reported in the Consolidated Balance Sheet. Our timber notes receivable

also bear interest at a fixed rate. At December 29, 2007, the estimated fair value of these

instruments exceeded their carrying amount by $128.5 million. The estimated fair values of our

other financial instruments, including cash and cash equivalents, receivables and short-term

borrowings are the same as their carrying values. In the opinion of management, we do not have

any significant concentration of credit risks. Concentration of credit risks with respect to trade

receivables is limited due to the wide variety of vendors, customers and channels to and through

which our products are sourced and sold, as well as their dispersion across many geographic

areas.

Changes in interest and currency rates expose us to financial market risk. In the past we have

used derivative financial instruments, such as interest rate swaps, rate hedge agreements, forward

purchase contracts and forward exchange contracts, to hedge underlying debt obligations or

anticipated transactions. We do not use them for trading purposes.

Except as described in the sub-heading ‘‘Additional Consideration Agreement’’ in Note 13,

Financial Instruments, Derivatives and Hedging Activities of the Notes to Consolidated Financial

Statements in ‘‘Item 8. Financial Statements and Supplementary Data’’ in this Form 10-K, at

December 29, 2007, we were not a party to any significant derivative financial instruments.

Additional Consideration Agreement

Pursuant to an Additional Consideration Agreement between OfficeMax and Boise Cascade,

L.L.C. entered into in connection with the Sale, we may have been required to make substantial

cash payments to, or entitled to receive substantial cash payments from, Boise Cascade, L.L.C. As

described below, the Additional Consideration Agreement terminated in the first quarter of 2008.

Under the Additional Consideration Agreement, the Sale proceeds were adjusted upward or

downward based on paper prices following the Sale, subject to annual and aggregate caps.

Specifically, we agreed to pay Boise Cascade, L.L.C. $710,000 for each dollar by which the average

market price per ton of a specified benchmark grade of cut-size office paper during any 12-month

period ending on September 30 was less than $800. Boise Cascade, L.L.C. agreed to pay us

$710,000 for each dollar by which the average market price per ton exceeded $920. Under the

terms of the agreement, neither party was obligated to make a payment in excess of $45 million in

any one year. Payments by either party were also subject to an aggregate cap of $125 million that

declined to $115 million in the fifth year and $105 million in the sixth year.

In connection with recording the Sale in 2004, we recognized a $42 million projected future

obligation related to the Additional Consideration Agreement based on internal estimates and

published industry paper price projections. We recognized accretion expense totaling approximately

$6.0 million in our Consolidated Statements of Income (Loss) in 2006 and 2005.

The Company recorded changes in the fair value of the Additional Consideration Agreement in

net income (loss) in the period they occured; however, any potential payments from Boise

Cascade, L.L.C. to us were not recorded in net income (loss) until all contingencies had been

satisfied, which was generally at the end of a 12-month measurement period ending on

September 30. Due to increases in actual and projected paper prices, the change in fair value of

36