Nike 2013 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2013 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

PART II

ITEM 7A. Quantitative and Qualitative Disclosures about

Market Risk

In the normal course of business and consistent with established policies and

procedures, we employ a variety of financial instruments to manage exposure

to fluctuations in the value of foreign currencies and interest rates. It is our

policy to utilize these financial instruments only where necessary to finance

our business and manage such exposures; we do not enter into these

transactions for trading or speculative purposes.

We are exposed to foreign currency fluctuations, primarily as a result of our

international sales, product sourcing and funding activities. Our foreign

exchange risk management program is intended to lessen both the positive

and negative effects of currency fluctuations on our consolidated results of

operations, financial position and cash flows. We use forward exchange

contracts and options to hedge certain anticipated but not yet firmly

committed transactions as well as certain firm commitments and the related

receivables and payables, including third-party and intercompany

transactions. We have, and may in the future, also use forward contracts to

hedge our investment in the net assets of certain international subsidiaries to

offset foreign currency translation adjustments related to our net investment in

those subsidiaries. Where exposures are hedged, our program has the effect

of delaying the impact of exchange rate movements on our consolidated

financial statements.

The timing for hedging exposures, as well as the type and duration of the

hedge instruments employed, are guided by our hedging policies and

determined based upon the nature of the exposure and prevailing market

conditions. Generally, hedged transactions are expected to be recognized

within 12 to 18 months. When intercompany loans are hedged, it is typically

for their expected duration. Hedged transactions are principally denominated

in Euros, British Pounds and Japanese Yen. See section “Foreign Currency

Exposures and Hedging Practices” under Item 7 for additional detail.

Our earnings are also exposed to movements in short- and long-term market

interest rates. Our objective in managing this interest rate exposure is to limit

the impact of interest rate changes on earnings and cash flows and to reduce

overall borrowing costs. To achieve these objectives, we maintain a mix of

commercial paper, bank loans and fixed rate debt of varying maturities and

have entered into receive-fixed, pay-variable interest rate swaps for a portion

of our fixed rate debt.

Market Risk Measurement

We monitor foreign exchange risk, interest rate risk and related derivatives

using a variety of techniques including a review of market value, sensitivity

analysis, and Value-at-Risk (“VaR”). Our market-sensitive derivative and other

financial instruments are foreign currency forward contracts, foreign currency

option contracts, interest rate swaps, intercompany loans denominated in

non-functional currencies, fixed interest rate U.S. Dollar denominated debt,

and fixed interest rate Japanese Yen denominated debt.

We use VaR to monitor the foreign exchange risk of our foreign currency

forward and foreign currency option derivative instruments only. The VaR

determines the maximum potential one-day loss in the fair value of these

foreign exchange rate-sensitive financial instruments. The VaR model

estimates assume normal market conditions and a 95% confidence level.

There are various modeling techniques that can be used in the VaR

computation. Our computations are based on interrelationships between

currencies and interest rates (a “variance/co-variance” technique). These

interrelationships are a function of foreign exchange currency market changes

and interest rate changes over the preceding one year period. The value of

foreign currency options does not change on a one-to-one basis with

changes in the underlying currency rate. We adjust the potential loss in option

value for the estimated sensitivity (the “delta” and “gamma”) to changes in the

underlying currency rate. This calculation reflects the impact of foreign

currency rate fluctuations on the derivative instruments only and does not

include the impact of such rate fluctuations on non-functional currency

transactions (such as anticipated transactions, firm commitments, cash

balances, and accounts and loans receivable and payable), including those

which are hedged by these instruments.

The VaR model is a risk analysis tool and does not purport to represent actual

losses in fair value that we will incur nor does it consider the potential effect of

favorable changes in market rates. It also does not represent the full extent of

the possible loss that may occur. Actual future gains and losses will differ from

those estimated because of changes or differences in market rates and

interrelationships, hedging instruments and hedge percentages, timing and

other factors.

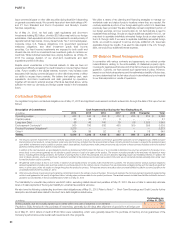

The estimated maximum one-day loss in fair value on our foreign currency

sensitive derivative financial instruments, derived using the VaR model, was

$34 million and $21 million at May 31, 2013 and 2012, respectively. The VaR

increased year-over-year as a result of an increase in the total notional value of

our foreign currency derivative portfolio combined with a longer average

duration on our outstanding trades at May 31, 2013. Such a hypothetical loss

in the fair value of our derivatives would be offset by increases in the value of

the underlying transactions being hedged. The average monthly change in the

fair values of foreign currency forward and foreign currency option derivative

instruments was $49 million and $87 million during fiscal 2013 and fiscal

2012, respectively.

The instruments not included in the VaR are intercompany loans

denominated in non-functional currencies, fixed interest rate Japanese Yen

denominated debt, fixed interest rate U.S. Dollar denominated debt and

interest rate swaps. Intercompany loans and related interest amounts are

eliminated in consolidation. Furthermore, our non-functional currency

intercompany loans are substantially hedged against foreign exchange risk

through the use of forward contracts, which are included in the VaR

calculation above. Therefore, we consider the interest rate and foreign

currency market risks associated with our non-functional currency

intercompany loans to be immaterial to our consolidated financial position,

results from operations and cash flows.

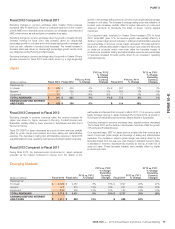

Details of third-party debt and interest rate swaps are provided in the table

below. The table presents principal cash flows and related weighted average

interest rates by expected maturity dates. Weighted average interest rates for

the fixed rate swapped to floating rate debt reflect the effective interest rates at

May 31, 2013.

NIKE, INC. 2013 Annual Report and Notice of Annual Meeting 85

FORM 10-K