Metro PCS 2010 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2010 Metro PCS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

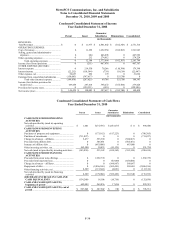

MetroPCS Communications, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

December 31, 2010, 2009 and 2008

F-24

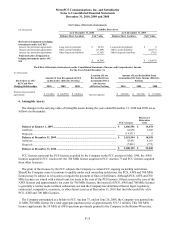

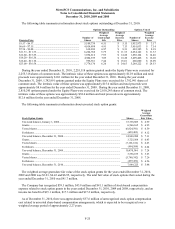

The value of the options is determined by using a Black-Scholes pricing model that includes the following

variables: 1) exercise price of the instrument, 2) fair market value of the underlying stock on date of grant,

3) expected life, 4) estimated volatility and 5) the risk-free interest rate. The Company utilized the following

weighted-average assumptions in estimating the fair value of the option grants in the years ended December 31,

2010, 2009 and 2008:

2010 2009 2008

Expected dividends ............................................................................................................... 0.00% 0.00% 0.00%

Expected volatility ................................................................................................................ 54.74% 50.01% 45.20%

Ris

k

-free interest rate ............................................................................................................ 2.24% 1.99% 2.49%

Expected lives in years ......................................................................................................... 5.00 5.00 5.00

Weighte

d

-average fair value of options:

Granted at fair value ............................................................................................................. $ 3.23 $ 6.43 $ 6.95

Weighte

d

-average exercise price of options:

Granted at fair value ............................................................................................................. $ 6.62 $ 14.23 $ 16.36

The Black-Scholes model requires the use of subjective assumptions including expectations of future dividends

and stock price volatility. Such assumptions are only used for making the required fair value estimate and should not

be considered as indicators of future dividend policy or stock price appreciation. Because changes in the subjective

assumptions can materially affect the fair value estimate, and because employee stock options have characteristics

significantly different from those of traded options, the use of the Black-Scholes option pricing model may not

provide a reliable estimate of the fair value of employee stock options.

A summary of the status of the Company’s Equity Plans as of December 31, 2010, 2009 and 2008, and changes

during the periods then ended, is presented in the table below:

2010 2009 2008

Shares

Weighted

Average

Exercise

Price Shares

Weighted

Average

Exercise

Price Shares

Weighted

Average

Exercise

Price

Outstanding, beginning of yea

r

.............................. 31,420,264 $ 13.69 30,677,588 $ 13.21 27,643,794 $ 11.70

Grante

d

.................................................................. 3,556,675 $ 6.62 3,725,564 $ 14.23 6,566,165 $ 16.36

Exercise

d

............................................................... (2,255,318) $ 4.49 (1,792,991) $ 4.81 (2,810,245) $ 4.48

Forfeite

d

................................................................ (1,079,089) $ 14.62 (1,189,897) $ 16.47 (722,126) $ 18.09

Outstanding, end of yea

r

........................................ 31,642,532 $ 13.52 31,420,264 $ 13.69 30,677,588 $ 13.21

Options vested or expected to vest at

yea

r

-en

d

............................................................... 31,138,160 $ 13.57 30,711,160 $ 13.63 29,633,907 $ 13.07

Options exercisable at yea

r

-en

d

............................. 23,653,307 $ 13.97 20,949,920 $ 12.24 15,920,318 $ 10.04

Options vested at yea

r

-en

d

..................................... 23,653,307 $ 13.97 20,949,920 $ 12.24 15,836,608 $ 10.05

Options outstanding under the Equity Plans as of December 31, 2010 have a total aggregate intrinsic value of

approximately $71.1 million and a weighted average remaining contractual life of 6.42 years. Options outstanding

under the Equity Plans as of December 31, 2009 and 2008 have a weighted average remaining contractual life of

6.83 and 7.54 years, respectively. Options vested or expected to vest under the Equity Plans as of December 31,

2010 have a total aggregate intrinsic value of approximately $69.4 million and a weighted average remaining

contractual life of 6.39 years. Options exercisable under the Equity Plans as of December 31, 2010 have a total

aggregate intrinsic value of approximately $49.8 million and a weighted average remaining contractual life of

5.82 years.