LensCrafters 2006 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2006 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

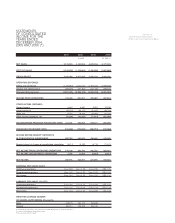

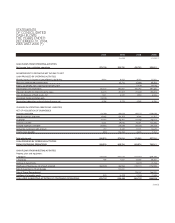

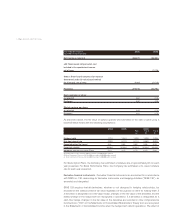

NOTES TO CONSOLIDATED

FINANCIAL STATEMENTS |111 <

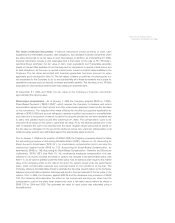

Company changed its method of valuing certain of its retail inventory from the last-in, first-out

method (“LIFO”) to FIFO in order to reduce the number of valuation methods among retail divisions.

The effect of the change in the inventory valuation method had an immaterial effect on the 2005

Statements of Consolidated Income. Inventories are recorded net of allowances for estimated

losses among other reserves. These reserves are calculated using various factors including sales

volume, historical shrink results and current trends.

Property, plant and equipment -Property, plant and equipment are stated at historical cost.

Depreciation is computed on the straight-line method over the estimated useful lives of the related

assets as follows:

Estimated useful life

Buildings and building improvements 19 to 40 years

Machinery and equipment 3 to 12 years

Aircraft 25 years

Other equipment 5 to 8 years

Leasehold improvements Lesser of 15 years or the remaining life of the lease

Maintenance and repair expenses are expensed as incurred. Upon the sale or disposition of

property and equipment, the cost of the asset and the related accumulated depreciation and

leasehold amortization are removed from the accounts and any resulting gain or loss is included in

the Statements of Consolidated Income.

Capitalized leased property -Capitalized leased assets are amortized using the straight-line

method over the term of the lease, or in accordance with practices established for similar owned

assets if ownership transfers to the Company at the end of the lease term.

Goodwill -Goodwill represents the excess of the purchase price (including acquisition-related

expenses) over the value assigned to the net tangible and identifiable intangible assets acquired.

The Company’s goodwill is tested annually for impairment as of December 31 of each year in

accordance with SFAS no. 142, Goodwill and Other Intangible Assets (“SFAS 142”). Additional

impairment tests are performed if, for any reason, the Company believes that an event has occurred

that may impair goodwill. Such tests are performed at the reporting unit level which consists of two

units, Wholesale and Retail, as required by the provisions of SFAS 142. For the years ended

December 31, 2004, 2005 and 2006, the result of this process was the determination that the

carrying value of each reporting unit of the Company was not impaired and, as a result, the

Company has not recorded a goodwill impairment charge in such years.

Other trade names and intangibles -In connection with various acquisitions, Luxottica Group has

recorded as intangible assets certain trade names and other intangibles which the Company

believes have a finite life. Trade names are amortized on a straight-line basis over periods ranging

from 20 to 25 years (see Note 7). Other intangibles include, among other items, distributor networks,

customer lists and contracts, franchise agreements and license agreements, and are amortized

over the respective useful lives. All intangibles are subject to test for impairment in accordance with

SFAS no. 144, Accounting for the Impairment or Disposal of Long-Lived Assets (“SFAS 144”).

Aggregate amortization expense of trade names and other intangibles for the years ended

December 31, 2004, 2005 and 2006 was Euro 50.7 million, Euro 61.9 million and Euro 68.8 million,

respectively.

Impairment of long-lived assets -Luxottica Group’s long-lived assets, other than goodwill, are