LensCrafters 2005 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2005 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

|7<

To our shareholders,

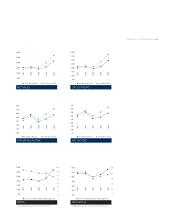

2005 was another year of significant growth for our Group. The Group’s excellent performance

confirmed our position of global leadership in premium and luxury eyewear. For the first time,

consolidated sales exceeded Euro 4 billion, thanks to significant improvements in both our retail and

wholesale businesses. Profitability continued to be strong.

The key principles of our business model - full vertical integration of manufacturing and distribution

combined with the most comprehensive wholesale-retail coverage of key eyewear markets worldwide -

once again proved our strategy right. We are uniquely positioned to help maximize opportunities for growth

of some of the world’s leading fashion and luxury brands - and this helps us to attract new ones. In fact,

in 2005 we added another prestigious brand - Burberry - to our already strong and well-balanced portfolio.

In early 2006, we further strengthened it for the future by signing with Polo Ralph Lauren, the global brand.

On the retail front, we posted excellent results in all key markets, especially in North America, where

the performance of our LensCrafters and Sunglass Hut retail brands was well above averages for the

overall retail segment. Results like these are the best demonstration of the excellent work we are carrying

out on our store base, the product mix and the positioning of our retail brands. The operational portion

of the integration of Cole National, which was acquired in 2004, was successfully concluded after one

year of intense work. The first positive results will be confirmed in 2006 and beyond, especially from

Pearle Vision, for which we have high expectations.

In 2005, our entry into the retail market in China was a key step in our strategy for growth. Today we

manage the leading premium optical chain in China and Hong Kong. Our nearly 300 stores are only a

starting point. In coming years, we will see growing sales and increasing market shares in this key

market, where we expect to sell plenty of our premium and luxury eyewear Made in Italy.

For wholesale, 2005 was a particularly positive year. The significant increase in sales and profitability

reflected our ongoing improvement in distribution and stronger brand portfolio. Ray-Ban continues to

grow year after year, as do our main license brands Bvlgari, Chanel, Prada and Versace. The new Dolce

& Gabbana collections, launched in October, were an immediate success. As a result, today we enjoy

greater penetration in both existing and new markets, with already excellent results overall and

opportunities for additional growth.

Finally, 2005 was a year of positive developments also from an organizational perspective. We are now

stronger and more effective in the market, thanks to more impactful resources. As a result, today we are

more integrated, flexible, rapid and effective. Our wholesale-retail distribution model efficiently and uniquely

covers all key markets worldwide, China included. Thanks to that, our strong results for the year allow us

to look to a future with the expectation of more growth coming from the challenges that lay ahead.

May 2006

CHAIRMAN’S

LETTER

TO SHAREHOLDERS

Chairman