LensCrafters 2005 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2005 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

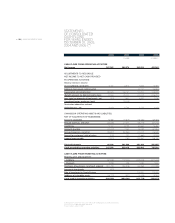

> 114 | ANNUAL REPORT 2005

Derivative financial instruments - Derivative financial instruments are accounted for in accordance

with SFAS No. 133, Accounting for derivative instruments and hedging activities (“SFAS 133”), as

amended and interpreted.

SFAS 133 requires that all derivatives, whether or not designed in hedging relationships, be recorded on

the balance sheet at fair value regardless of the purpose or intent for holding them. If a derivative is

designated as a fair-value hedge, changes in the fair value of the derivative and the related change in

the hedge item are recognized in operations. If a derivative is designated as a cash-flow hedge,

changes in the fair value of the derivative are recorded in other comprehensive income/(loss) (“OCI”) in

the Statements of Consolidated Shareholders’ Equity and are recognized in the Statements of

Consolidated Income when the hedged item affects operations. The effect of these derivatives in the

Statements of Consolidated Operations depends on the item hedged (for example, interest rate hedges

are recorded in interest expense). For a derivative that does not qualify as a hedge, changes in fair value

are recognized in the statements of consolidated operations, under the caption “Other - net”.

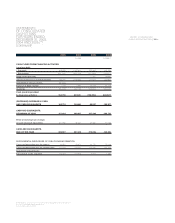

Certain transactions and other future events, such as (i) the derivative no longer effectively offsetting

changes to the cash flow of the hedged instrument, (ii) the expiration, termination or sale of the

derivative, or (iii) any other reason of which the Company becomes aware that the derivative no longer

qualifies as a cash flow hedge, would cause the balance remaining in other comprehensive income to

be realized immediately as earnings. Based on current interest rates and market conditions, the

estimated aggregate amount to be recognized as earnings from other comprehensive income relating

to these cash flow hedges in fiscal 2006 is approximately Euro 0.5 million, net of taxes.

Luxottica Group uses derivative financial instruments, principally interest rate and currency swap

agreements, as part of its risk management policy to reduce its exposure to market risks from changes

in interest and foreign exchange rates. Although it has not done so in the past, the Company may enter

into other derivative financial instruments when it assesses that the risk can be hedged effectively.

Recent accounting pronouncements - In November 2004, the Financial Accounting Standards

Board (“FASB”) issued SFAS No. 151, Inventory costs - an amendment of ARB No. 43, Chapter 4, to

clarify that abnormal amounts of idle facility expense, freight, handling costs and wasted material

should be recognized as period costs. In addition, this statement requires that the allocation of fixed

production costs of conversion be based on the normal capacity of the production facilities. The

adoption of such standard is for fiscal years beginning after June 15, 2005. The Company believes the

adoption will not have a material effect on the Consolidated Financial Statements.

In December 2004, the FASB issued SFAS No. 123-R (revised 2004), Share-based payment (“SFAS

123-R”), which replaces the existing SFAS 123 and supersedes APB 25. SFAS 123-R requires

companies to measure and record compensation expense for Stock Options and other share-based

payment methods based on the instruments’ fair value. SFAS 123-R became effective for the Company

beginning on January 1, 2006. The Company has evaluated the impact of the adoption of SFAS No.

123-R and determined that the additional compensation costs which would have been recorded in

fiscal 2005 were not material. Based on current options outstanding as of December 31, 2005,

excluding the incentive and shareholder grants for which the effect of adopting SFAS 123-R would vary

significantly due to numerous variables, including, but not limited to, future stock price and estimated

date of vesting, the effect of the adoption of SFAS 123-R on the 2006 statement of consolidated income

would be a reduction of pre-tax income by approximately Euro 4.4 million.

In December 2004, the FASB issued SFAS No. 153, Exchanges of nonmonetary assets - an amendment

of APB Opinion No. 29 (“SFAS 153”). SFAS 153 amends APB No. 29, Accounting for nonmonetary

transactions, to eliminate the exception for nonmonetary exchanges of similar productive assets and