LensCrafters 2005 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2005 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

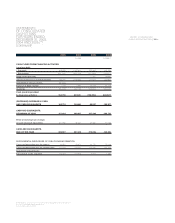

NOTES TO CONSOLIDATED

FINANCIAL STATEMENTS | 115 <

replaces it with a general exception for exchanges of nonmonetary assets that do not have commercial

substance. A nonmonetary exchange has commercial substance if the future cash flows of the entity

are expected to change significantly as a result of the exchange. SFAS 153 is effective for reporting

periods beginning after June 15, 2005. The adoption of SFAS 153 is not expected to have a material

effect on the Company’s Consolidated Financial Statements.

In March 2005, the FASB issued Interpretation No. 47, Accounting for conditional asset retirement

obligations - an interpretation of FASB Statement No. 143 (“FIN 47”), which clarifies the term “conditional

asset retirement obligation” as used in SFAS 143 and requires the recognition of a liability for a

“conditional asset retirement obligation” if the fair value of the liability can be reasonably estimated. FIN

47 is effective for reporting periods beginning after December 15, 2005. The adoption of FIN 47 is not

expected to have a material effect on the Company’s Consolidated Financial Statements.

In May 2005, the FASB issued SFAS No. 154, Accounting changes and error corrections - a

replacement of APB Opinion No. 20 and FASB Statement No. 3 (“SFAS 154”). SFAS 154 applies to all

voluntary changes in accounting principles and changes required by accounting pronouncements in

instances where the pronouncement does not include a specific transition provisions. This Statement

replaces APB No. 20, Accounting changes, and SFAS No. 3, Reporting accounting changes in interim

financial statements. SFAS 154 requires retroactive application to prior periods’ financial statements of

changes in accounting principles unless it is impracticable to do so. SFAS 154 is effective for

accounting changes and corrections of errors made in fiscal years beginning after December 15, 2005.

In June 2005, the Emerging Issues Task Force (“EITF”) reached a consensus on Issue No. 05-6,

Determining the amortization period for leasehold improvements (“EITF 05-6”), which requires that

leasehold improvements acquired in a business combination or purchased significantly after, and not

contemplated at the inception of the lease, be amortized over the lesser of the useful life of the asset or

a term that includes lease renewals that are reasonably assured. This consensus is applicable for

leasehold improvements acquired or purchased beginning after June 29, 2005 and will be followed in

future periods if and when necessary.

In October 2005, the FASB issued FASB Staff Position No. 13-1, Accounting for rental costs incurred

during a construction period (“FSP 13-1”), which concluded that rental costs associated with ground

and building operating leases that are incurred during the construction period should be recognized as

rental expense in such period. This guidance is effective for reporting periods beginning after December

15, 2005. The adoption of FSP 13-1 is not expected to have a material effect on the Company’s

Consolidated Financial Statements and will be followed in future periods if and when necessary.

In February 2006, the FASB issued SFAS No. 155, Accounting for certain hybrid financial instruments - an

amendment of FASB Statements No. 133 and 140 (“SFAS 155”), which amends SFAS 133, and SFAS 140,

Accounting for transfers and servicing of financial assets and extinguishments of liabilities. The statement:

• permits fair value remeasurement for any hybrid financial instrument that contains an embedded

derivative that otherwise would require bifurcation;

• clarifies which interest-only strips and principal-only strips are not subject to the requirements of

Statement No. 133;

• establishes a requirement to evaluate interests in securitized financial assets to identify interests that

are freestanding derivatives or that are hybrid financial instruments that contain an embedded

derivative requiring bifurcation; and

• clarifies that concentrations of credit risk in the form of subordination are not embedded derivatives; and

• amends Statement No. 140 to eliminate the prohibition on a qualifying special-purpose entity from

holding a derivative financial instrument that pertains to a beneficial interest other than another

derivative financial instrument.