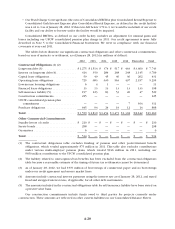

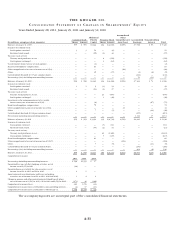

Kroger 2011 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2011 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

A-25

• Theextenttowhichtheadjustmentswearemakingtoourstrategycreatevalueforourshareholderswill

depend primarily on the reaction of our customers and our competitors to these adjustments, as well

as operating conditions, including inflation or deflation, increased competitive activity, and cautious

spending behavior of our customers.

• Ourproductcostinflationcouldvaryfromourestimateduetogeneraleconomicconditions,weather,

availability of raw materials and ingredients in the products that we sell and their packaging, and other

factors beyond our control.

• Our ability to pass on product cost increases will depend on the reactions of our customers and

competitors to those increases.

• Ourabilitytousefreecashflowtocontinuetomaintainourdebtcoverageandtorewardourshareholders

could be affected by unanticipated increases in net total debt, our inability to generate free cash flow at

the levels anticipated, and our failure to generate expected earnings.

• OurLIFOchargeandthetimingofourrecognitionofLIFOexpensewillbeaffectedprimarilybychanges

in product costs during the year.

• Ifactualresultsdiffersignificantlyfromanticipatedfutureresultsforcertainreportingunitsincluding

variable interest entities, an impairment loss for any excess of the carrying value of the reporting units’

goodwill over the implied fair value would have to be recognized.

• Inadditiontothefactorsidentifiedabove,ouridenticalstoresalesgrowthcouldbeaffectedbyincreases

in Kroger private label sales, the effect of our “sister stores” (new stores opened in close proximity to an

existing store) and reductions in retail pricing.

• Ouroperatingmargins,withoutfuel,coulddeclineorfailtomeetexpectationsifweareunabletopass

on any cost increases, if we fail to deliver the cost savings contemplated or if changes in the cost of our

inventory and the timing of those changes differ from our expectations.

• Wehaveestimatedourexposuretotheclaimsandlitigationarisinginthenormalcourseofbusiness,

as well as to the material litigation facing Kroger, and believe we have made provisions where it is

reasonably possible to estimate and where an adverse outcome is probable. Unexpected outcomes in

these matters, however, could result in an adverse effect on our earnings.

• Consolidationinthefoodindustryislikelytocontinueandtheeffectsonourbusiness,eitherfavorable

or unfavorable, cannot be foreseen.

• Rentexpense,whichincludessubtenantrentalincome,couldbeadverselyaffectedbythestateofthe

economy, increased store closure activity and future consolidation.

• Depreciation expense, which includes the amortization of assets recorded under capital leases, is

computed principally using the straight-line method over the estimated useful lives of individual assets,

or the remaining terms of leases. Use of the straight-line method of depreciation creates a risk that future

asset write-offs or potential impairment charges related to store closings would be larger than if an

accelerated method of depreciation were followed.

• Oureffectivetaxratemaydifferfromtheexpectedrateduetochangesinlaws,thestatusofpending

items with various taxing authorities, and the deductibility of certain expenses.

• The actual amount of automatic and matching cash contributions to our 401(k) Retirement Savings

Account Plan will depend on the number of participants, savings rate, compensation as defined by the

plan, and length of service of participants.

• Theamountsofourcontributionsandrecordedexpenserelatedtomulti-employerpensionfundscould

vary from the amounts that we expect, and could increase more than anticipated. Should asset values in

these funds deteriorate, if employers withdraw from these funds without providing for their share of the

liability, or should our estimates prove to be understated, our contributions could increase more rapidly

than we have anticipated.