Kroger 2011 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2011 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

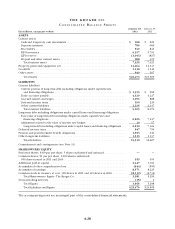

A-19

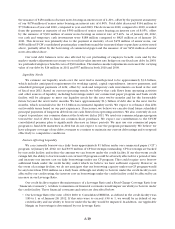

the issuance of $450 million of senior notes bearing an interest rate of 2.20%, offset by the payment at maturity

of our $478 million of senior notes bearing an interest rate of 6.80%. Total debt decreased $164 million to

$7.9 billion as of year-end 2010, compared to year-end 2009. The decrease in 2010, compared to 2009, resulted

from the payment at maturity of our $500 million of senior notes bearing an interest rate of 8.05%, offset

by the issuance of $300 million of senior notes bearing an interest rate of 5.40%. As of January 28, 2012,

our cash and temporary cash investments were $188 million compared to $825 million as of January 29,

2011. This decrease was primarily due to the payment at maturity of our $478 million of senior notes, our

$650 million UFCW consolidated pension plan contribution and the increased share repurchase activity noted

above, partially offset by the borrowing of commercial paper and the issuance of our $450 million of senior

notes described above.

Our total debt balances were also affected by our prefunding of employee benefit costs and by the

mark-to-market adjustments necessary to record fair value interest rate hedges on our fixed rate debt. In 2009,

we prefunded employee benefit costs of $300 million. The mark-to-market adjustments increased the carrying

value of our debt by $24 million in 2011 and $57 million in both 2010 and 2009.

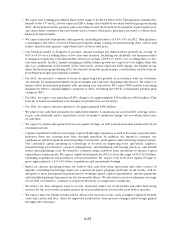

Liquidity Needs

We estimate our liquidity needs over the next twelve month period to be approximately $3.6 billion,

which includes anticipated requirements for working capital, capital expenditures, interest payments, and

scheduled principal payments of debt, offset by cash and temporary cash investments on hand at the end

of fiscal year 2011. Based on current operating trends, we believe that cash flows from operating activities

and other sources of liquidity, including borrowings under our commercial paper program and bank credit

facility, will be adequate to meet our liquidity needs for the next twelve months and for the foreseeable

future beyond the next twelve months. We have approximately $1.3 billion of debt due in the next twelve

months, which is included in the $3.6 billion in estimated liquidity needs. We expect to refinance this debt

on favorable terms based on our past experience. If necessary, we believe we can also fund future scheduled

principal payments of long-term debt from our cash flows from operating activities. We also currently do not

expect to purchase our common shares at the levels we did in 2011. We used our commercial paper program

toward the end of 2011 to fund our common share purchases. We expect our contributions to the UFCW

consolidated pension plan to significantly decrease in future periods. We may use our commercial paper

program to fund debt maturities in 2012 but do not expect to use the program permanently. We believe we

have adequate coverage of our debt covenants to continue to maintain our current debt ratings and to respond

effectively to competitive conditions.

Factors Affecting Liquidity

We can currently borrow on a daily basis approximately $1 billion under our commercial paper (“CP”)

program. At January 28, 2012, we had $370 million of CP borrowings outstanding. CP borrowings are backed

by our credit facility, and reduce the amount we can borrow under the credit facility. If our short-term credit

ratings fall, the ability to borrow under our current CP program could be adversely affected for a period of time

and increase our interest cost on daily borrowings under our CP program. This could require us to borrow

additional funds under the credit facility, under which we believe we have sufficient capacity. However, in

the event of a ratings decline, we do not anticipate that our borrowing capacity under our CP program would

be any lower than $500 million on a daily basis. Although our ability to borrow under the credit facility is not

affected by our credit rating, the interest cost on borrowings under the credit facility could be affected by an

increase in our Leverage Ratio.

Our credit facility requires the maintenance of a Leverage Ratio and a Fixed Charge Coverage Ratio (our

“financial covenants”). A failure to maintain our financial covenants would impair our ability to borrow under

the credit facility. These financial covenants and ratios are described below:

• OurLeverageRatio(theratioofNetDebttoConsolidatedEBITDA,asdefinedinthecreditfacility)was

1.85 to 1 as of January 28, 2012. If this ratio were to exceed 3.50 to 1, we would be in default of our

credit facility and our ability to borrow under the facility would be impaired. In addition, our Applicable

Margin on borrowings is determined by our Leverage Ratio.