Kroger 2011 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2011 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124

|

|

A-60

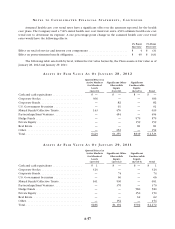

NO T E S T O CO N S O L I D A T E D FI N A N C I A L ST A T E M E N T S , CO N T I N U E D

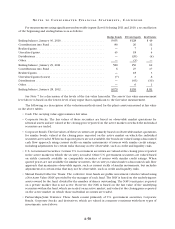

Under the terms of the MOU, the locals of the UFCW agreed to a future pension benefit formula through

2021. The Company was designated as the named fiduciary of the new consolidated pension plan with sole

investment authority over the assets. The Company committed to contribute sufficient funds to cover the

actuarial cost of current accruals and to fund the pre-consolidation Unfunded Actuarial Accrued Liability

( “ UA A L” ) t h a t e x i s t e d a s o f D e ce m b e r 31, 2 011, i n a s e r i e s o f i n s t a l l m e n t s o n or b efo r e M a r c h 31, 2 018 . A t Ja n u a r y 1,

2012, the UAAL was estimated to be $911 (pre-tax). In accordance with GAAP, the Company expensed $911 in

2011 related to the UAAL. The expense was based on a preliminary estimate of the contractual commitment.

As the estimate is updated, we may incur additional expense. We do not expect any adjustments to be material.

In the fourth quarter of 2011, the Company contributed $650 to the consolidated multi-employer pension plan

of which $600 was allocated to the UAAL and $50 was allocated to service and interest costs and expensed in

2011. Future contributions will be dependent, among other things, on the investment performance of assets

in the plan. The funding commitments under the MOU replace the prior commitments under the four existing

funds to pay an agreed upon amount per hour worked by eligible employees.

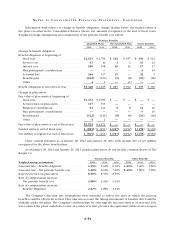

The Company recognizes expense in connection with these plans as contributions are funded, or in the

case of the UFCW consolidated pension plan, when commitments are made. The Company made contributions

to these funds of $946 in 2011, $262 in 2010 and $233 in 2009. The cash contributions for 2011 include the

Company’s $650 contribution to the UFCW consolidated pension plan in the fourth quarter of 2011.

The risks of participating in multi-employer pension plans are different from the risks of participating in

single-employer pension plans in the following respects:

a. Assets contributed to the multi-employer plan by one employer may be used to provide benefits to

employees of other participating employers.

b. If a participating employer stops contributing to the plan, the unfunded obligations of the plan

allocable to such withdrawing employer may be borne by the remaining participating employers.

c. If the Company stops participating in some of its multi-employer pension plans, the Company may

be required to pay those plans an amount based on its allocable share of the underfunded status of

the plan, referred to as a withdrawal liability.

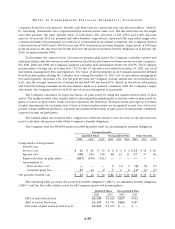

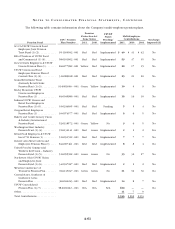

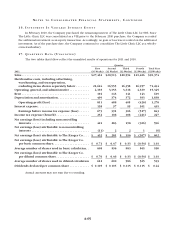

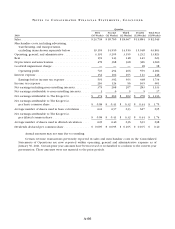

The Company’s participation in these plans is outlined in the following tables. The EIN / Pension Plan

Number column provides the Employer Identification Number (“EIN”) and the three-digit pension plan

number. The most recent Pension Protection Act Zone Status available in 2011 and 2010 is for the plan’s

year-end at December 31, 2010 and December 31, 2009, respectively. Among other factors, generally, plans

in the red zone are less than 65 percent funded, plans in yellow zone are less than 80 percent funded, and

plans in the green zone are at least 80 percent funded. The FIP/RP Status Pending / Implemented Column

indicates plans for which a funding improvement plan (“FIP”) or a rehabilitation plan (“RP”) is either pending

or has been implemented. Unless otherwise noted, the information for these tables was obtained from the

Forms 5500 filed for each plan’s year-end at December 31, 2010 and December 31, 2009. The multi-employer

contributions listed in the table below are the Company’s multi-employer contributions made in fiscal years

2011, 2010, and 2009.