Kroger 2011 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2011 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

|

|

A-54

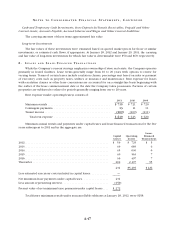

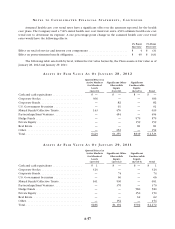

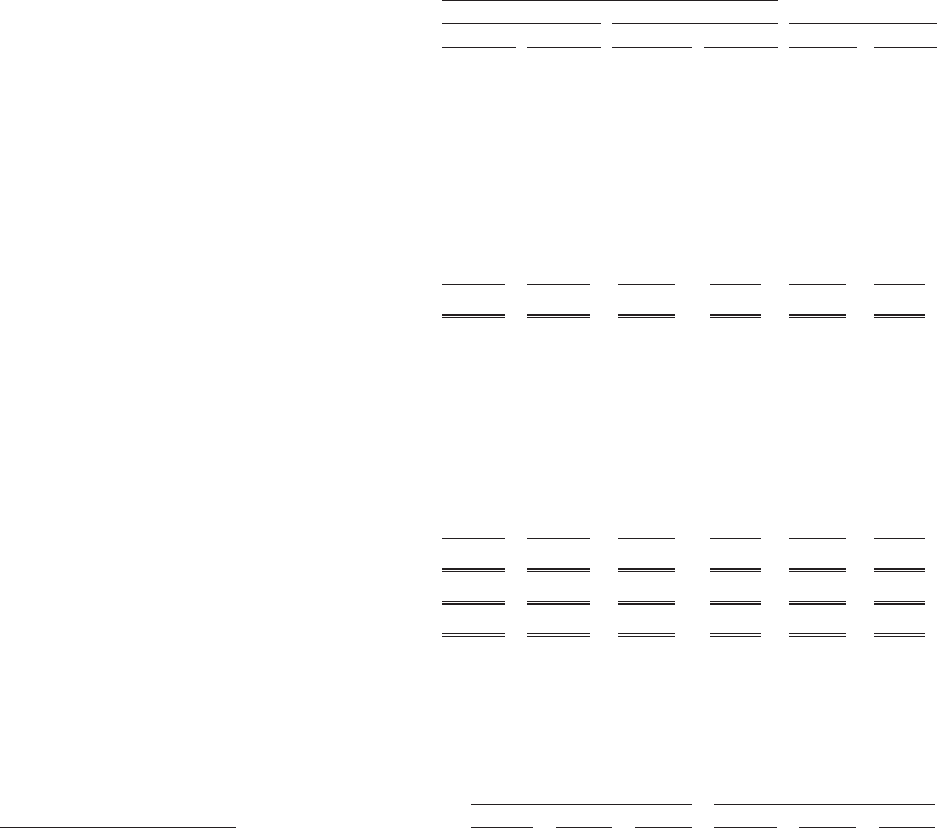

NO T E S T O CO N S O L I D A T E D FI N A N C I A L ST A T E M E N T S , CO N T I N U E D

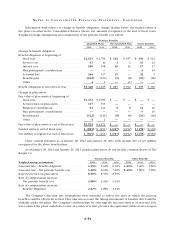

Information with respect to change in benefit obligation, change in plan assets, the funded status of

the plans recorded in the Consolidated Balance Sheets, net amounts recognized at the end of fiscal years,

weighted average assumptions and components of net periodic benefit cost follow:

Pension Benefits

Qualified Plans Non-Qualified Plan Other Benefits

2011 2010 2011 2010 2011 2010

Change in benefit obligation:

Benefit obligation at beginning of

fiscal year .............................. $2,923 $ 2,706 $ 192 $ 187 $ 330 $ 312

Service cost ............................ 41 40 3213 12

Interest cost ............................ 158 158 10 12 17 17

Plan participants’ contributions ............. ————910

Actuarial loss ........................... 344 137 21 —32 5

Benefits paid ........................... (122) (120) (9) (8) (23) (26)

Other ................................. 42—(1) ——

Benefit obligation at end of fiscal year .......... $3,348 $ 2,923 $ 217 $ 192 $ 378 $ 330

Change in plan assets:

Fair value of plan assets at beginning of

fiscal year .............................. $2,472 $ 2,096 $ — $ — $ — $ —

Actual return on plan assets ................ 117 353 ————

Employer contributions ................... 52 141 9814 16

Plan participants’ contributions ............. ————910

Benefits paid ........................... (122) (120) (9) (8) (23) (26)

Other ................................. 42————

Fair value of plan assets at end of fiscal year . . . . . $2,523 $ 2,472 $ — $ — $ — $ —

Funded status at end of fiscal year . . . . . . . . . . . . . $ (825) $ (451) $ (217) $(192) $ (378) $(330)

Net liability recognized at end of fiscal year . . . . . $ (825) $ (451) $ (217) $(192) $ (378) $(330)

Other current liabilities as of January 28, 2012 and January 29, 2011 both include $27 of net liability

recognized for the above benefit plans.

As of January 28, 2012 and January 29, 2011, pension plan assets do not include common shares of The

Kroger Co.

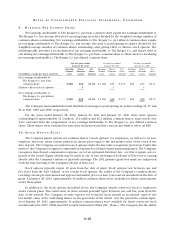

Pension Benefits Other Benefits

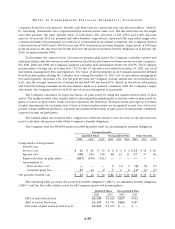

Weighted average assumptions 2011 2010 2009 2011 2010 2009

Discount rate – Benefit obligation . . . . . . . . . . . . . . 4.55% 5.60% 6.00% 4.40% 5.40% 5.80%

Discount rate – Net periodic benefit cost . . . . . . . . 5.60% 6.00% 7.00% 5.40% 5.80% 7.00%

Expected return on plan assets . . . . . . . . . . . . . . . . 8.50% 8.50% 8.50%

Rate of compensation increase –

Net periodic benefit cost ................... 2.88% 2.92% 2.92%

Rate of compensation increase –

Benefit Obligation ........................ 2.82% 2.88% 2.92%

The Company’s discount rate assumptions were intended to reflect the rates at which the pension

benefits could be effectively settled. They take into account the timing and amount of benefits that would be

available under the plans. The Company’s methodology for selecting the discount rates as of year-end 2011

was to match the plan’s cash flows to that of a yield curve that provides the equivalent yields on zero-coupon