Kroger 2011 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2011 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

A-51

NO T E S T O CO N S O L I D A T E D FI N A N C I A L ST A T E M E N T S , CO N T I N U E D

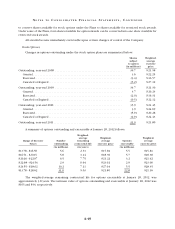

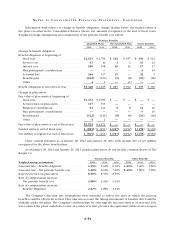

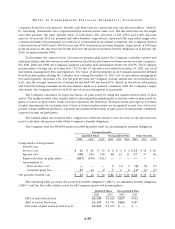

Total stock compensation recognized in 2011, 2010 and 2009 was $81, $79 and $83, respectively. Stock

option compensation recognized in 2011, 2010 and 2009 was $22, $25 and $29, respectively. Restricted shares

compensation recognized in 2011, 2010 and 2009 was $59, $54 and $54 respectively.

The total intrinsic value of options exercised was $24, $11 and $17 in 2011, 2010 and 2009, respectively.

The total amount of cash received in 2011 by the Company from the exercise of options granted under

share-based payment arrangements was $118. As of January 28, 2012, there was $100 of total unrecognized

compensation expense remaining related to non-vested share-based compensation arrangements granted

under the Company’s equity award plans. This cost is expected to be recognized over a weighted-average

period of approximately two years. The total fair value of options that vested was $33, $37 and $39 in 2011,

2010 and 2009, respectively.

Shares issued as a result of stock option exercises may be newly issued shares or reissued treasury shares.

Proceeds received from the exercise of options, and the related tax benefit, may be utilized to repurchase

the Company’s common shares under a stock repurchase program adopted by the Company’s Board of

Directors. During 2011, the Company repurchased approximately five million common shares of stock in

such a manner.

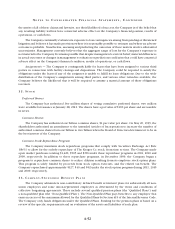

11. CO M M I T M E N T S A N D CO N T I N G E N C I E S

The Company continuously evaluates contingencies based upon the best available evidence.

The Company believes that allowances for loss have been provided to the extent necessary and that its

assessment of contingencies is reasonable. To the extent that resolution of contingencies results in amounts

that vary from the Company’s estimates, future earnings will be charged or credited.

The principal contingencies are described below:

Insurance — The Company’s workers’ compensation risks are self-insured in most states. In addition,

other workers’ compensation risks and certain levels of insured general liability risks are based on retrospective

premium plans, deductible plans, and self-insured retention plans. The liability for workers’ compensation risks

is accounted for on a present value basis. Actual claim settlements and expenses incident thereto may differ

from the provisions for loss. Property risks have been underwritten by a subsidiary and are all reinsured with

unrelated insurance companies. Operating divisions and subsidiaries have paid premiums, and the insurance

subsidiary has provided loss allowances, based upon actuarially determined estimates.

Litigation — On October 6, 2006, the Company petitioned the Tax Court (Ralphs Grocery Company

and Subsidiaries, formerly known as Ralphs Supermarkets, Inc. v. Commissioner of Internal Revenue,

Docket No. 20364-06) for a redetermination of deficiencies asserted by the Commissioner of Internal

Revenue. The dispute at issue involves a 1992 transaction in which Ralphs Holding Company acquired the

stock of Ralphs Grocery Company and made an election under Section 338(h)(10) of the Internal Revenue

Code. The Commissioner determined that the acquisition of the stock was not a purchase as defined by

Section 338(h)(3) of the Internal Revenue Code and that the acquisition therefore did not qualify for a Section

338(h)(10) election. On January 27, 2011, the Tax Court issued its opinion upholding the Company’s position

that the acquisition of the stock qualified as a purchase, granting the Company’s motion for partial summary

judgment and denying the Tax Commissioner’s motion. The Company anticipates that all remaining issues in

the matter will be resolved and the Tax Court will enter its decision. The parties will then have 90 days to file

an appeal. As of January 28, 2012, an adverse decision would require a cash payment of up to approximately

$553, including interest. Any accounting implications of an adverse decision in this case would be charged

through the statement of operations.

Various claims and lawsuits arising in the normal course of business, including suits charging violations

of certain antitrust, wage and hour, or civil rights laws, are pending against the Company. Some of these suits

purport or have been determined to be class actions and/or seek substantial damages. Any damages that may

be awarded in antitrust cases will be automatically trebled. Although it is not possible at this time to evaluate