Kroger 2011 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2011 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

A-45

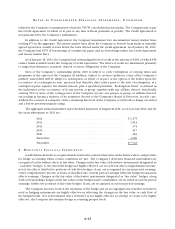

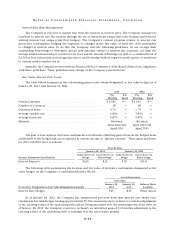

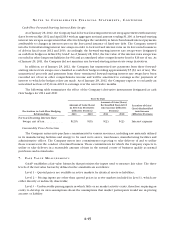

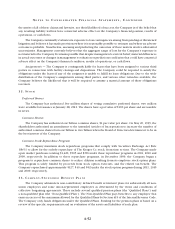

NO T E S T O CO N S O L I D A T E D FI N A N C I A L ST A T E M E N T S , CO N T I N U E D

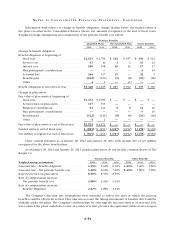

Cash Flow Forward-Starting Interest Rate Swaps

As of January 28, 2012, the Company had 24 forward-starting interest rate swap agreements with maturity

dates between May 2012 and April 2013 with an aggregate notional amount totaling $1,200. A forward-starting

interest rate swap is an agreement that effectively hedges the variability in future benchmark interest payments

attributable to changes in interest rates on the forecasted issuance of fixed-rate debt. The Company entered

into the forward-starting interest rate swaps in order to lock in fixed interest rates on its forecasted issuances

of debt in fiscal years 2012 and 2013. Accordingly, the forward-starting interest rate swaps were designated

as cash-flow hedges as defined by GAAP. As of January 28, 2012, the fair value of the interest rates swaps was

recorded in other long term liabilities for $41 and accumulated other comprehensive loss for $26 net of tax. As

of January 29, 2011, the Company did not maintain any forward-starting interest rate swap derivatives.

In addition, as of January 28, 2012, the Company has unamortized net payments from three forward-

starting interest rate swaps once classified as cash flow hedges totaling approximately $5 ($3 net of tax). The

unamortized proceeds and payments from these terminated forward-starting interest rate swaps have been

recorded net of tax in other comprehensive income and will be amortized to earnings as the payments of

interest to which the hedges relate are made. As of January 28, 2012, the Company expects to reclassify an

unrealized net loss of $3 from AOCI to earnings over the next twelve months.

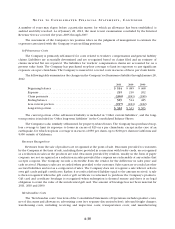

The following table summarizes the effect of the Company’s derivative instruments designated as cash

flow hedges for 2011 and 2010:

Year-To-Date

Derivatives in Cash Flow Hedging

Relationships

Amount of Gain/(Loss)

in AOCI on Derivative

(Effective Portion)

Amount of Gain/(Loss)

Reclassified from AOCI

into Income (Effective

Portion)

Location of Gain/

(Loss) Reclassified

into Income

(Effective Portion)2011 2010 2011 2010

Forward-Starting Interest Rate

Swaps, net of tax . . . . . . . . . . . . $(29) $(5) $(2) $(2) Interest expense

Commodity Price Protection

The Company enters into purchase commitments for various resources, including raw materials utilized

in its manufacturing facilities and energy to be used in its stores, warehouses, manufacturing facilities and

administrative offices. The Company enters into commitments expecting to take delivery of and to utilize

those resources in the conduct of normal business. Those commitments for which the Company expects to

utilize or take delivery in a reasonable amount of time in the normal course of business qualify as normal

purchases and normal sales.

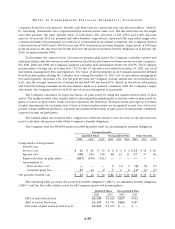

7. FA I R VA L U E ME A S U R E M E N T S

GAAP establishes a fair value hierarchy that prioritizes the inputs used to measure fair value. The three

levels of the fair value hierarchy defined in the standards are as follows:

Level 1 – Quoted prices are available in active markets for identical assets or liabilities;

Level 2 – Pricing inputs are other than quoted prices in active markets included in Level 1, which are

either directly or indirectly observable;

Level 3 – Unobservable pricing inputs in which little or no market activity exists, therefore requiring an

entity to develop its own assumptions about the assumptions that market participants would use in pricing

an asset or liability.