Kroger 2011 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2011 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

|

|

A-53

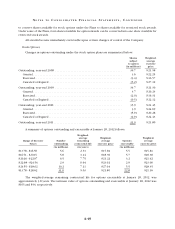

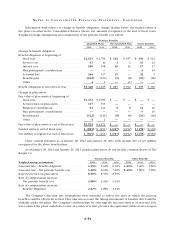

NO T E S T O CO N S O L I D A T E D FI N A N C I A L ST A T E M E N T S , CO N T I N U E D

In addition to providing pension benefits, the Company provides certain health care benefits for retired

employees. The majority of the Company’s employees may become eligible for these benefits if they reach

normal retirement age while employed by the Company. Funding of retiree health care benefits occurs as

claims or premiums are paid.

The Company recognizes the funded status of its retirement plans on the Consolidated Balance Sheet.

Actuarial gains or losses, prior service costs or credits and transition obligations that have not yet been

recognized as part of net periodic benefit cost are required to be recorded as a component of AOCI. All plans

are measured as of the Company’s fiscal year end.

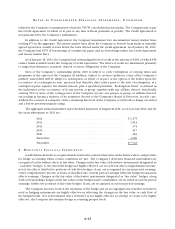

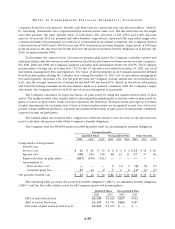

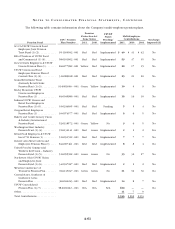

Amounts recognized in AOCI as of January 28, 2012 and January 29, 2011 consist of the following

(pre-tax):

Pension Benefits Other Benefits Total

2011 2010 2011 2010 2011 2010

Net actuarial loss (gain) . . . . . . . . . . . . . . . . . . . . . . $1,329 $942 $ (21) $ (55) $1,308 $887

Prior service cost (credit) ..................... 34(12) (17) (9) (13)

Transition obligation ......................... 11——11

Total. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,333 $947 $ (33) $ (72) $1,300 $875

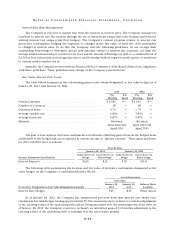

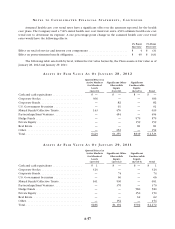

Amounts in AOCI expected to be recognized as components of net periodic pension or postretirement

benefit costs in the next fiscal year are as follows (pre-tax):

Pension

Benefits Other Benefits Total

2012 2012 2012

Net actuarial loss (gain) . . . . . . . . . . . . . . . . . . . . . . $101 $ — $101

Prior service cost (credit) ..................... 1 (4) (3)

Total. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $102 $ (4) $ 98

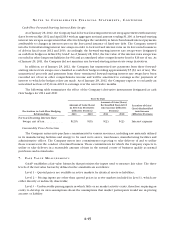

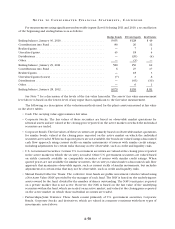

Other changes recognized in other comprehensive income in 2011, 2010, and 2009 were as follows

(pre-tax):

Pension Benefits Other Benefits Total

2011 2010 2009 2011 2010 2009 2011 2010 2009

Incurred net actuarial loss (gain) .... $451 $ (18) $142 $32 $ 4 $21 $483 $ (14) $163

Incurred prior service cost ......... —— — —— — —— —

Amortization of prior service

credit (cost) .................. (1) (1) (2) 55 7 44 5

Amortization of net actuarial

gain (loss) ................... (64) (50) (14) 23 5 (62) (47) (9)

Total recognized in other

comprehensive income ......... 386 (69) 126 39 12 33 425 (57) 159

Total recognized in net periodic

benefit cost and other

comprehensive income ......... $456 $ (4) $157 $62 $33 $49 $518 $ 29 $206