Kodak 2003 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2003 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

Financials

70

used to compute the other postretirement benefit amounts approximate

the U.S. assumptions.

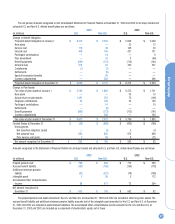

The weighted-average assumptions used to determine the net bene-

fit obligations were as follows:

2003 2002

Discount rate 6.00% 6.50%

Salary increase rate 4.25% 4.25%

The weighted-average assumptions used to determine the net

postretirement benefit cost were as follows:

2003 2002

Discount rate 6.50% 7.25%

Salary increase rate 4.25% 4.25%

The weighted-average assumed healthcare cost trend rates used to

compute the other postretirement amounts were as follows:

2003 2002

Healthcare cost trend 11.00% 12.00%

Rate to which the cost trend rate

is assumed to decline (the ultimate

trend rate) 5.00% 5.00%

Year that the rate reaches the

ultimate trend rate 2010 2010

Assumed healthcare cost trend rates have a significant effect on the

amounts reported for the healthcare plans. A one percentage point change

in assumed healthcare cost trend rates would have the following effects:

1% increase 1% decrease

Effect on total service and interest cost $ 7 $ (7)

Effect on postretirement benefit

obligation 119 (108)

The Company expects to pay benefits of $258 million for its U.S.

other postretirement benefits plan in 2004.

NOTE 19: ACCUMULATED OTHER

COMPREHENSIVE (LOSS) INCOME

The components of accumulated other comprehensive (loss) income at

December 31, 2003, 2002 and 2001 were as follows:

(in millions) 2003 2002 2001

Accumulated unrealized holding

gains (losses) related to

available-for-sale securities $ 11 $ — $ (6)

Accumulated unrealized losses

related to hedging activity (15) (9) (5)

Accumulated translation

adjustments 107 (306) (524)

Accumulated minimum pension

liability adjustments (334) (456) (62)

Total $ (231) $(771) $(597)

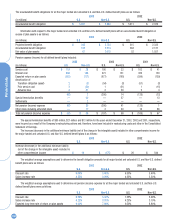

NOTE 20: STOCK OPTION AND

COMPENSATION PLANS

The Company’s stock incentive plans consist of the 2000 Omnibus Long-

Term Compensation Plan (the 2000 Plan), the 1995 Omnibus Long-Term

Compensation Plan (the 1995 Plan) and the 1990 Omnibus Long-Term

Compensation Plan (the 1990 Plan). The Plans are administered by the

Executive Compensation and Development Committee of the Board of

Directors.

Under the 2000 Plan, 22 million shares of the Company’s common

stock may be granted to a variety of employees between January 1, 2000

and December 31, 2004. The 2000 Plan is substantially similar to, and is

intended to replace, the 1995 Plan, which expired on December 31, 1999.

Stock options are generally non-qualified and are at prices not less than

100% of the per share fair market value on the date of grant, and the

options generally expire ten years from the date of grant, but may expire

sooner if the optionee’s employment terminates. The 2000 Plan also pro-

vides for Stock Appreciation Rights (SARs) to be granted, either in tandem

with options or freestanding. SARs allow optionees to receive payment

equal to the increase in the Company’s stock market price from the grant

date to the exercise date. At December 31, 2003, 52,215 freestanding

SARs were outstanding at option prices ranging from $23.25 to $62.44.

Compensation expense recognized in 2003 on those freestanding SARs,

which had option prices less than the market value of the Company’s

underlying common stock, was not material.

Under the 1995 Plan, 22 million shares of the Company’s common

stock were eligible for grant to a variety of employees between February

1, 1995 and December 31, 1999. Stock options are generally non-quali-

fied and are at prices not less than 100% of the per share fair market

value on the date of grant, and the options generally expire ten years from

the date of grant, but may expire sooner if the optionee’s employment ter-

minates. The 1995 Plan also provides for SARs to be granted, either in

tandem with options or freestanding. At December 31, 2003, 319,409

freestanding SARs were outstanding at option prices ranging from $31.30

to $90.63.

Under the 1990 Plan, 22 million shares of the Company’s common

stock were eligible for grant to key employees between February 1, 1990

and January 31, 1995. The stock options, which were generally non-quali-

fied, could not have prices less than 50% of the per share fair market

value on the date of grant; however, no options below fair market value

were granted. The options generally expire ten years from the date of

grant, but may expire sooner if the optionee’s employment terminates.

The 1990 Plan also provided that options with dividend equivalents, tan-

dem SARs and freestanding SARs could be granted. At December 31,

2003, 41,034 freestanding SARs were outstanding at option prices rang-

ing from $30.25 to $44.50.

In January 2002, the Company’s shareholders voted in favor of a vol-

untary stock option exchange program for its employees. Under the pro-

gram, employees were given the opportunity, if they so chose, to cancel

outstanding stock options previously granted to them at exercise prices

ranging from $26.90 to $92.31, in exchange for new options to be granted

on or shortly after August 26, 2002, over six months and one day from

February 22, 2002, the date the old options were canceled. The number of

shares subject to the new options was determined by applying an

exchange ratio in the range of 1:1 to 1:3 (i.e., one new option share for

every three canceled option shares) based on the exercise price of the