Kodak 2003 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2003 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

Proxy Statement

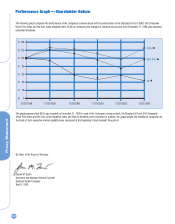

127

Exhibit II—Audit and Non-Audit Services Pre-Approval Policy

I. STATEMENT OF PRINCIPLES

The Audit Committee is responsible for the appointment, compensation and oversight of the work of the independent auditor. As part of this responsibili-

ty, the Audit Committee is required to pre-approve the audit and non-audit services performed by the independent auditor in order to assure that they do

not impair the auditor’s independence from the Company. Accordingly, the Audit Committee has adopted this Pre-Approval Policy which sets forth the

procedures and the conditions pursuant to which services proposed to be performed by the independent auditor may be pre-approved.

This Pre-Approval Policy establishes two different approaches to pre-approving services: proposed services either may be pre-approved without specific

consideration by the Audit Committee (“general pre-approval”) or require the specific pre-approval of the Audit Committee (“specific pre-approval”). The

Audit Committee believes that the combination of these two approaches in this policy will result in an effective and efficient procedure to pre-approve

services performed by the independent auditor. As set forth in this policy, unless a type of service has received general pre-approval, it will require spe-

cific pre-approval by the Audit Committee. Any proposed services exceeding pre-approved budgeted amounts will also require specific pre-approval by

the Audit Committee. For both types of pre-approval, the Audit Committee shall consider whether such services are consistent with the SEC’s rules on

auditor independence. The Audit Committee shall determine whether the audit firm is best positioned to provide the most effective and efficient service.

The non-audit services that have the general pre-approval of the Audit Committee will be reviewed on an annual basis unless the Audit Committee con-

siders a different period and states otherwise. The Audit Committee shall annually review and pre-approve the audit, audit-related and tax services that

can be provided by the independent auditor without obtaining specific pre-approval from the Audit Committee. The Audit Committee will revise the list of

general pre-approved services from time to time, based upon subsequent determinations.The Audit Committee does not delegate its responsibilities to

pre-approve services performed by the independent auditor to management or to others.

The independent auditor has reviewed this policy and believes that implementation of the policy will not adversely affect the auditor’s independence.

II. AUDIT SERVICES

The Audit Committee shall approve the annual audit services engagement terms and fees no later than its review of the independent auditor’s audit plan.

Audit services may include the annual financial statement audit (including required quarterly reviews), subsidiary audits and other procedures required to

be performed by the independent auditor to be able to form an opinion on the Company’s consolidated financial statements. These other procedures

include information systems and procedural reviews and testing performed in order to understand and place reliance on the systems of internal control,

and consultations occurring during, and as a result of, the audit. Audit services also include the attestation engagement for the independent auditor’s

report on management’s report on internal control over financial reporting. The Audit Committee shall also approve, if necessary, any significant changes

in terms, conditions and fees resulting from changes in audit scope, company structure or other items.

In addition to the annual audit services engagement approved by the Audit Committee, the Audit Committee may grant general pre-approval to other

audit services, which are those services that only the independent auditor reasonably can provide. Other audit services may include statutory audits or

financial audits for subsidiaries or affiliates of the Company and services associated with SEC registration statements, periodic reports and other docu-

ments filed with the SEC or other documents issued in connection with securities offerings.

III. AUDIT-RELATED SERVICES

Audit-related services are assurance and related services that traditionally are performed by the independent auditor. Because the Audit Committee

believes that the provision of audit-related services does not impair the independence of the auditor and is consistent with the SEC’s rules on auditor

independence, the Audit Committee may grant general pre-approval to audit-related services. Audit-related services include, among others, due diligence

services pertaining to potential business acquisitions/dispositions; accounting consultations for significant or unusual transactions not classified as “audit

services”; assistance with understanding and implementing new accounting and financial reporting guidance from rulemaking authorities; financial

audits of employee benefit plans; agreed-upon or expanded audit procedures performed at the request of management; and assistance with internal

control reporting requirements.

IV. TAX SERVICES

The Audit Committee believes that the independent auditor can provide traditional tax services to the Company such as U.S. and international tax plan-

ning and compliance. The Audit Committee will not pre-approve the retention of the independent auditor in connection with a transaction initially recom-

mended by the independent auditor, the purpose of which may be tax avoidance and the tax treatment of which may not be supported in the Internal

Revenue Code and related regulations.

V. OTHER PERMISSIBLE NON-AUDIT SERVICES

The Audit Committee may grant general pre-approval to those permissible non-audit services (other than tax services, which are addressed above) that

it believes are routine and recurring services, would not impair the independence of the auditor and are consistent with the SEC’s rules on auditor inde-

pendence.