Kodak 2003 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2003 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

Proxy Statement

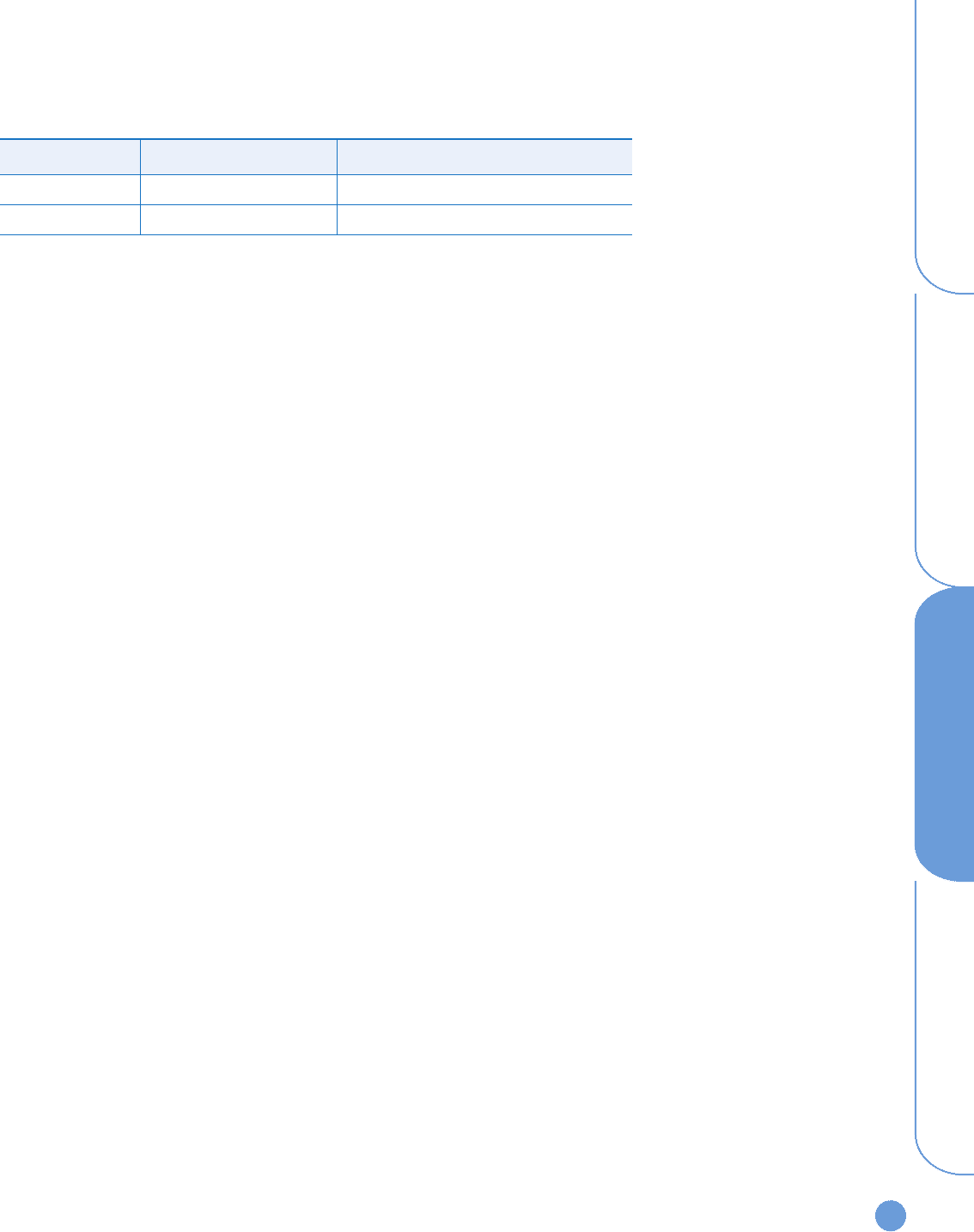

113

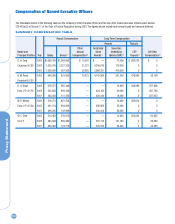

The following table shows the years of service credited as of December 31, 2003, to Mr. Carp and Mr. Morley. This table also shows the amount of Mr.

Carp’s and Mr. Morley’s APC at the end of 2003. Messrs. Perez, Brust and Shih, who participated in the cash balance feature in 2003, are not listed.

Retirement Plan Table

Name Years of Service Average Participating Compensation

D. A. Carp 33 $ 2,181,619

M. P. Morley 39(a) 884,096

(a) Under Mr. Morley’s retention agreement, if he elects upon his retirement to take a lump sum distribution of his retirement benefit, the amount of his benefit will be cal-

culated using a discount rate no less favorable than the discount rate used under the Company’s pension plan to calculate the retirement benefits of participants who

retired effective November 1, 2003.

Cash Balance Feature

Under the cash balance feature of the Company’s pension plan, the Company establishes an account for each participating employee. Every month the

employee works, the Company credits the employee’s account with an amount equal to four percent of the employee’s monthly pay. In addition, the

ongoing balance of the employee’s account earns interest at the 30-year Treasury bond rate. To the extent federal laws place limitations on the amount

of pay that may be taken into account under the plan, four percent of the excess pay is credited to an account established for the employee in an

unfunded supplementary plan. If a participating employee leaves the Company and is vested (five or more years of service), the employee’s account bal-

ance will be distributed to the employee in the form of a lump sum or monthly annuity. Participating employees whose account balance exceeds $5,000

also have the choice of leaving their account balances in the plan to continue to earn interest.

In addition to the benefits described above, Mr. Brust is covered under a special supplemental pension arrangement established under his amended offer

letter. This arrangement provides Mr. Brust a single life annuity of $12,500 per month upon his retirement if he remains employed with the Company for

at least five years. If Mr. Brust remains employed until January 3, 2006, he will, in lieu of receiving the $12,500 per month annuity, be treated as if eligi-

ble for the non-cash balance portion of the plan. For this purpose, Mr. Brust will be credited with 14 years of extra service in addition to his actual serv-

ice. If Mr. Brust remains employed until January 2, 2007, he will be credited with 18 years of extra service in addition to his actual service for purposes

of the non-cash balance portion of the plan. In any case, Mr. Brust’s supplemental benefit will be offset by his cash balance benefit.

Mr. Perez is also eligible for a supplemental pension benefit under the terms of his March 3, 2003 offer letter. Under this arrangement, if Mr. Perez

remains employed for three years, he will be treated as if eligible for the non-cash balance portion of the plan. For this purpose, he will be considered to

have completed eight years of service with the Company and attained age 65. If, instead, Mr. Perez remains employed for nine years, he will be consid-

ered to have completed 25 years of service with the Company. Mr. Perez’s supplemental pension benefit will be offset by his cash balance benefit.