HTC 2011 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2011 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

|

|

3. Capital Surplus

Under the Company Law, capital surplus can only be used to

offset a deficit. However, the capital surplus from shares issued in

excess of par (additional paid-in capital from issuance of common

shares, conversion of bonds and treasury stock transactions)

and donations may be capitalized, with capitalization limited to

a certain percentage of the Company's paid-in capital. Also, the

capital surplus from long-term investments may not be used for

any purpose.

(1) Additional paid-in capital - issuance of shares in excess of par

The additional paid-in capital was NT$9,056,323 thousand as

of January 1, 2010. In April 2010, the retirement of treasury

stock caused a decrease of NT$172,188 thousand in additional

paid-in capital. The bonus to employees of NT$4,859,236

thousand for 2009 was approved in the stockholders' meeting

in June 2010. Of the approved bonus, NT$1,943,694 thousand

was in the form of common stock, consisting of 5,021 thousand

common shares at their fair value, which were distributed

in 2010. The difference between par value and fair value of

NT$1,893,488 thousand was accounted for as additional paid-

in capital in 2010. As a result, the additional paid-in capital as

of December 31, 2010 was NT$10,777,623 thousand.

Also, in June 2011, the bonus to employees of NT$8,491,704

thousand (US$280,449 thousand) for 2010 was approved

in the stockholders' meeting. Of the approved bonus,

NT$4,245,851 thousand (US$140,224 thousand) was in the

form of common stock, consisting of 4,006 thousand common

shares at their fair value, which were distributed in 2011. The

difference between par value and fair value of NT$4,205,796

thousand (US$138,901 thousand) was accounted for as

additional paid-in capital in 2011. In December 2011, the

retirement of treasury stock caused a decrease of NT$173,811

thousand (US$5,740 thousand) in additional paid-in capital.

As a result, the additional paid-in capital as of December 31,

2011 was NT$14,809,608 thousand (US$489,105 thousand).

(2) Treasury stock transactions and expired stock options

In June 2011, the Company resolved to transfer treasury

shares to employees. In 2011, the number of shares for

transfer to employees was 6,000 thousand, with 5,875

thousand shares exercised. Based on the fair value at the

grant date, NT$1,750,767 thousand (US$57,821 thousand) was

accounted for as capital surplus - treasury stock transactions,

and NT$37,503 thousand (US$1,239 thousand) for the

unexercised 125 thousand shares was accounted for as capital

surplus - expired stock options. Also, in December 2011, the

retirement of treasury stock caused decreases in treasury

stock transactions and expired stock options of NT$20,309

thousand (US$671 thousand) and NT$435 thousand (US$15

thousand), respectively. As a result, the treasury stock

transactions and expired stock options as of December 31,

2011 were NT$1,730,458 thousand (US$57,150 thousand) and

NT$37,068 thousand (US$1,224 thousand), respectively.

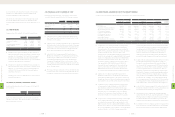

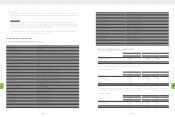

The fair values at the grant date for the fifth and sixth

stock option buyback were NT$394.105 and NT$210.121,

respectively. These fair values were estimated using the

Black-Scholes option valuation model. The inputs to the

model were as follows:

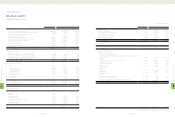

5th Buyback 6th Buyback

Assumption Exercise price (NT$) $598.83 $797.30

Expected dividend yield 3.71% 3.71%

Expected life 1.67 months 1.67 months

Expected price volatility 56.99% 56.99%

Risk-free interest rate 0.7157% 0.7157%

Fair value $394.105 $210.121

(3) Long-term equity investments

As of January 1, 2010, the capital surplus from long-term

equity-method investments was NT$18,411 thousand. When

the Company did not subscribe for the new shares issued

by an equity-method investee, Huada Digital Corporation,

in September 2011, the Company's total investment carrying

value and capital surplus decreased by NT$374 thousand

(US$12 thousand) each in 2011. As a result, the capital surplus

from long-term equity-method investments as of December

31, 2011 was NT$18,037 thousand (US$596 thousand).

(4) Merger

The additional paid-in capital from a merger was NT$25,189

thousand as of January 1, 2010. In April 2010, the retirement

of treasury stock caused a decrease of NT$479 thousand

in additional paid-in capital from a merger. As a result, the

additional paid-in capital from a merger as of December 31,

2010 was NT$24,710 thousand. Also, in December 2011, the

retirement of treasury stock caused a decrease of NT$287

thousand (US$9 thousand) in additional paid-in capital from

a merger. As a result, the additional paid-in capital from a

merger as of December 31, 2011 was NT$24,423 thousand

(US$807 thousand).

4. Appropriation of Retained Earnings and Dividend Policy

(1) Based on the Company Law of the ROC and the Company's

Articles of Incorporation, 10% of the Company's annual net

income less any deficit should first be appropriated as legal

reserve. From the remainder, there should be appropriations

of not more than 3 as remuneration to directors and

supervisors and at least 5% as bonuses to employees.

(2) Legal reserve shall be appropriated until it has reached the

Company's paid-in capital. This reserve may be used to

offset a deficit. Under the revised Company Law issued on

January 4, 2012, when the legal reserve has exceeded 25% of

the Company's paid-in capital, the excess may be transferred

to capital or distributed in cash.

(3) As part of a high-technology industry and as a growing

enterprise, the Company considers its operating

environment, industry developments, and long-term interests

of stockholders as well as its programs to maintain operating

Bank of Taiwan in the committee's name. The pension fund balances

were NT$447,728 thousand and NT$481,685 thousand (US$15,908

thousand) as of December 31, 2010 and 2011, respectively.

Based on the Statement of Financial Accounting Standards No. 18 -

"Accounting for Pensions," issued by the Accounting Research and

Development Foundation of the ROC, pension cost under a defined

benefit pension plan should be calculated by the actuarial method.

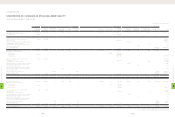

1. The Company's net pension costs under the defined

benefit plan in 2010 and 2011 were as follows:

2010 2011

NT$ NT$ US$ (Note 3)

Service cost $4,915 $5,980 $197

Interest cost 6,539 6,858 227

Projected return on plan assets (8,582) (9,206) (304)

Amortization of unrecognized

net transition obligation, net - - -

Amortization of net pension

benefit 297 492 16

Net pension cost $3,169 $4,124 $136

2. The reconciliations between pension fund status and

prepaid pension cost as of December 31, 2010 and 2011

were as follows:

2010 2011

NT$ NT$ US$ (Note 3)

Present actuarial value of benefit

obligation

Vested benefit obligation $1,525 $10,026 $331

Non-vested benefit obligation

190,908 192,737 6,365

Accumulated benefit obligation

192,433 202,763 6,696

Additional benefits on future salaries

150,480 162,889 5,380

Projected benefit obligation 342,913 365,652 12,076

Fair value of plan assets (447,728) (481,685) (15,908)

Funded status (104,815) (116,033) (3,832)

Unrecognized pension loss (54,130) (67,794) (2,239)

Prepaid pension cost $(158,945) $(183,827) $(6,071)

3. Assumptions used in actuarially determining the

present value of the projected benefit obligation were

as follows:

2010 2011

Weighted-average discount rate 2.00% 2.00%

Assumed rate of increase in future compensation 3.75% 4.00%

Expected long-term rate of return on plan assets 2.00% 2.00%

The payments from the fund amounted to NT$1,702 thousand in 2010

and NT$793 thousand (US$26 thousand) in 2011.

(19) STOCKHOLDERS' EQUITY

1. Capital Stock

The Company's outstanding common stock as of January 1,

2010 amounted to NT$7,889,358 thousand, divided into 788,936

thousand common shares at NT$10.00 par value. In April 2010,

the Company retired 15,000 thousand treasury shares amounting

to NT$150,000 thousand. In June 2010, the stockholders

approved the transfer of retained earnings of NT$386,968

thousand and employee bonuses of NT$50,206 thousand

to capital stock. As a result, the amount of the Company's

outstanding common stock as of December 31, 2010 increased to

NT$8,176,532 thousand, divided into 817,653 thousand common

shares at NT$10.00 par value.

In June 2011, the stockholders approved the transfer of retained

earnings of NT$403,934 thousand (US$13,340 thousand) and

employee bonuses of NT$40,055 thousand (US$1,323 thousand)

to capital stock. Also, in December 2011, the Company retired

10,000 thousand treasury shares amounting to NT$100,000

thousand (US$3,303 thousand). As a result, the amount of the

Company's outstanding common stock as of December 31, 2011

increased to NT$8,520,521 thousand (US$281,400 thousand),

divided into 852,052 thousand common shares at NT$10.00

(US$0.33) par value.

2. Global Depositary Receipts

The Company issued 14,400 thousand common shares

corresponding to 3,600 thousand units of Global Depositary

Receipts (GDRs). For this GDR issuance, the Company's

stockholders, including Via Technologies, Inc., also issued

12,878.4 thousand common shares, corresponding to 3,219.6

thousand GDR units. Thus, the entire offering consisted of 6,819.6

thousand GDR units. Each GDR represents four common shares,

and was issued, at a premium, at NT$131.1. For this common

share issuance, net of related expenses, NT$1,696,855 thousand

was accounted for as capital surplus. This share issuance for

cash was completed and registered on November 19, 2003.

The holders of these GDRs have the same rights and obligations

as the stockholders of the Company. However, the distribution

of the offering and sales of GDRs and the shares represented

thereby in certain jurisdictions may be restricted by law. In

addition, the GDRs offered and the shares represented are not

transferable, except in accordance with the restrictions described

in the GDR offering circular and related laws applied in Taiwan.

Through the depositary custodian in Taiwan, GDR holders are

entitled to exercise these rights:

(1) To vote; and

(2) To receive dividends and participate in new share issuance

for cash subscription.

Taking into account the effect of stock dividends, the GDRs

increased to 9,015.1 thousand units (36,060.5 thousand

shares). The holders of these GDRs requested the Company to

redeem the GDRs to get the Company's common shares. As of

December 31, 2011, there were 6,404.4 thousand units of GDRs

redeemed, representing 25,617.5 thousand common shares, and

the outstanding GDRs represented 10,443 thousand common

shares or 1.25% of the Company's common shares.

8

FINANCIAL INFORMATION

| 162 |

8

FINANCIAL INFORMATION

| 163 |