HTC 2011 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2011 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115

|

|

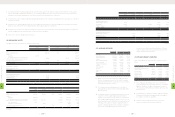

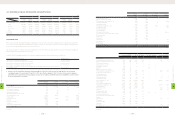

6. OTHER MATTERS REQUIRING SUPPLEMENTARY EXPLANATION

(1) The company should disclose the financial impact to the company if the company and its affiliated

companies have incurred any financial or cash flow difficulties in 2011.

None.

(2) Explanation of significant accounting policies:

1. Revenue recognition and allowance for doubtful accounts

Revenue is measured at fair value as the transaction price agreed between HTC and buyers (considering trade discounts and volume

discounts). Trade discounts include price protection, marketing development fund, and mail-in rebate. Allowances for doubtful accounts are

estimated using aging analysis, which is reviewed and updated regularly by assessing the probability of recovering outstanding receivables,

credit ratings and general economic factors. HTC assigns a rating to each customer based on their financial health. Allowance accounts of

customers with good credit ratings are accrued by 1% ~ 5% when receivables are 31~90 days overdue and by 5% ~ 100% when receivables

are over 91 days overdue. Individual determinations are made for customers with poor credit, which include making reasonable estimates of

allowances for receivables not yet due.

2. Inventory write-downs

Assessments of allowances for loss on decline in inventory value or loss on items retired are based on analysis of obsolete inventory items. HTC

began on 1 January 2008 to adopt newly released Statement of Financial Accounting Standards No. 10 to assess inventory value on a category

by category basis and write off as losses currently-held inventory with no practical market value.

3. Accrued marketing expenses

Reasonable estimates for marketing expenses and trade discounts such as price protection, marketing development fund, and mail-in rebate

are made according to contract stipulations and other related factors and recognized as marketing expenses, and are entered as expenses or

deductions from revenue depending on their category.

4. Reserve for warranty expenses

HTC provides a one- to two-year period of free warranty maintenance in after sales service. It makes reasonable estimates of possible amounts

for that service and recognizes warranty liabilities based on historical experience and other relevant factors. Allocation to product warranty

reserve stands at around 3-4% of revenue currently.

5. Financial assets/liabilities at fair value through profit or loss

HTC's financial assets/liabilities at fair value through profit or loss comprise forward foreign exchange contracts. We calculated the fair value of

each outstanding contract at the close of 2011 based on its maturation date, average closing rates, and swap point quotations provided by the

Reuters.

6. Available-for-sale financial assets

The available-for-sale financial assets are listed stocks and quasi money market fund. Estimates of fair value are based on the closing price for

exchange- or OTC-listed securities on the balance sheet date.

Investments in equity instruments are classified as at FVTPL, unless the Company designates an investment that is not held for trading as at

FVTOCI on initial recognition. If investments in equity instruments are classified as at fair value through other comprehensive income (FVTOCI),

except for dividends that are usually recognized in profit or loss in accordance with IAS 18 - Revenue, all gains and losses are recognised in OCI

and will not be reclassified to profit or loss.

For financial liabilities, the main difference in classification and measurement refers to financial liabilities that are classified as at FVTPL. Under

IFRS 9 - Financial Instruments, for financial liabilities that are designated as at FVTPL, the amount of change in the fair value of the financial

liability that is attributable to changes in the credit risk of that liability is recognised in OCI, unless the recognition of the effects of changes in

the liability's credit risk in OCI would create or enlarge an accounting mismatch in profit or loss. Changes in fair value attributable to a financial

liability's credit risk are not subsequently reclassified to profit or loss. For financial liabilities previously classified as at FVTPL under IAS 39 -

Financial Instruments: Recognition and Measurement, the amount of change in the fair value of the financial liability is recognized in profit or

loss.

For its first-time adoption of IFRS 9 - Financial instruments, the Company expects that these items will be designated as at FVTOCI: (a)

investments in equity instruments (not held for trading) that are initially classified as available-for-sale and measured at fair value at the end

of each reporting period in accordance with IAS 39 - Financial Instruments: Recognition and Measurement; and (b) financial assets initially

classified as financial assets carried at cost. In addition, the investment in mutual funds initially classified as available-for-sale will be reclassified

to financial asset at FVTPL.

8

FINANCIAL INFORMATION

| 220 |

8

FINANCIAL INFORMATION

| 221 |