Google 2012 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2012 Google annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

42 GOOGLE INC. |Form10-K

PART II

ITEM7A.Quantitative and Qualitative Disclosures About MarketRisk

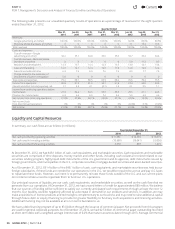

During the second quarter of 2012, we began to hedge the variability of forecasted interest payments using forward-starting interest

swaps. The total notional amount of these swaps was $1.0billion as of December31,2012, with terms calling for us to receive

interest at a variable rate and to pay interest at a fi xed rate. These forward-starting interest swaps eff ectively fi x the benchmark

interest rate on an anticipated debt issuance of $1.0billion in 2014, and they will be terminated upon issuance of the debt.

When entering into forward-starting interest rate swaps, we are subject to market risk with respect to changes in the underlying

benchmark interest rate that impacts the fair value of the forward-starting interest swaps. We manage market risk by matching

the terms of the swaps with the critical terms of the expected debt issuance.

We considered the historical volatility of short-term interest rates and determined that it was reasonably possible that an adverse

change of 100 basis points could be experienced in the near term. Ahypothetical 1.00% (100 basis points) increase in interest rates

would have resulted in a decrease in the fair values of our marketable securities of approximately $934million and $1.1billion at

December31, 2011 and 2012, after taking into consideration the off setting eff ect from interest rate derivative contracts outstanding

as of December31,2011 and 2012. A hypothetical 1.00% (100 basis points) decrease in interest rates would have resulted in a

decrease in the fair values of our forward-starting interest swaps of approximately $107million at December31, 2012.

Contents

44