Energizer 2014 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2014 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

ENERGIZER HOLDINGS, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in millions, except per share)

The Company also holds a derivative instrument contract to mitigate a portion of the risk associated with the change in the

market value of its unfunded deferred compensation liabilities, which is tied to change in the market value of the Company's

common stock.

The Company uses raw materials that are subject to price volatility. The Company may use hedging instruments as it desires to

reduce exposure to variability in cash flows associated with future purchases of commodities. In September 2012, the Company

discontinued hedge accounting treatment for its then-existing zinc contracts as these contracts no longer met the accounting

requirements for classification as cash flow hedges because of an ineffective correlation to the underlying zinc exposure being

hedged. There were no outstanding derivative contracts for the future purchases of commodities as of September 30, 2014.

Through December 2012, the Company had specific interest rate risk with respect to interest expense on the Company's term

loan, which was fully repaid by the end of the first quarter of fiscal 2013. As a result, the then-existing interest rate swap

agreement in place to hedge this specific risk was settled on November 30, 2012 for a $0.3 loss. This loss was included in

interest expense in the Consolidated Statements of Earnings and Comprehensive Income. At September 30, 2014, the Company

had $289.5 of variable rate debt outstanding.

For further discussion see Notes 13 and 16 of the Notes to Consolidated Financial Statements.

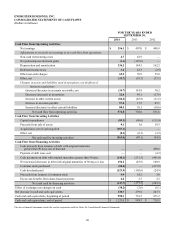

Cash Equivalents – Cash equivalents are all considered to be highly liquid investments with a maturity of three months or less

when purchased. At September 30, 2014, the Company had $1,129.0 in available cash, substantially all of which was outside of

the U.S. The Company has extensive operations, including a significant manufacturing footprint outside of the U.S. We

manage our worldwide cash requirements by reviewing available funds among the many subsidiaries through which we

conduct our business and the cost effectiveness with which those funds can be accessed. The repatriation of cash balances from

certain of our subsidiaries could have adverse tax consequences or be subject to regulatory capital requirements; however, those

balances are generally available without legal restrictions to fund ordinary business operations. U.S. income taxes have not

been provided on a significant portion of undistributed earnings of international subsidiaries. Our intention is to reinvest these

earnings indefinitely.

As of September 30, 2014, our unremitted cash in Venezuela had accumulated to approximately $83, or 7% of our total cash

balance. There is substantial uncertainty with respect to the exchange rate that might apply to any future remittance of our local

currency cash in Venezuela. As of September 30, 2014, we continue to value our Venezuela cash balance at the official

exchange rate of 6.30 bolivars to one U.S. dollar. To date, we have not been invited to participate in the SICAD I auction

process nor chosen to utilize the SICAD II auction system. Whether we will be able to access or participate in either SICAD

system in the foreseeable future or what volume of currency exchange, if any, we would be able to transact through these

alternative mechanisms is unclear. Due to the future uncertainty and volatility of the foreign exchange markets in Venezuela we

believe that any future remittance of our local currency cash balances from Venezuela would be substantially less than the

amount recorded as of September 30, 2014 on our Consolidated Balance Sheets per U.S. GAAP. As such, we cannot give

assurance as to the exchange rate at which such balances might be converted in the future and/or when we might be able to

repatriate such balances, if at all. U.S. GAAP does not permit the establishment of reserves against cash balances, and for this

reason we have not done so.

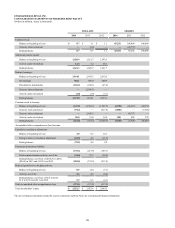

Cash Flow Presentation – The Consolidated Statements of Cash Flows are prepared using the indirect method, which

reconciles net earnings to cash flow from operating activities. The reconciliation adjustments include the removal of timing

differences between the occurrence of operating receipts and payments and their recognition in net earnings. The adjustments

also remove cash flows arising from investing and financing activities, which are presented separately from operating activities.

Cash flows from foreign currency transactions and operations are translated at an average exchange rate for the period. Cash

flows from hedging activities are included in the same category as the items being hedged, which is primarily operating

activities. Cash payments related to income taxes are classified as operating activities.

Accounts Receivable Valuation – Accounts receivable are stated at their net realizable value. The allowance for doubtful

accounts reflects the Company’s best estimate of probable losses inherent in the receivables portfolio determined on the basis of

historical experience, specific allowances for known troubled accounts and other currently available information. Bad debt

expense is included in Selling, general and administrative expense (SG&A) in the Consolidated Statements of Earnings and

Comprehensive Income.

Inventories – Inventories are valued at the lower of cost or market, with cost generally being determined using average cost or

the first-in, first-out (FIFO) method.

61