Energizer 2014 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2014 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

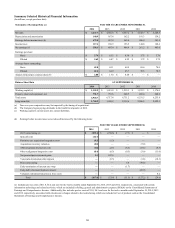

ENERGIZER HOLDINGS, INC.

(Dollars in millions, except per share data)

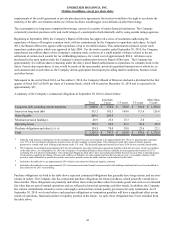

Operating Activities

Cash flow from operating activities is the primary funding source for operating needs and capital investments. Cash flow from

operating activities was $572.0 in fiscal 2014, $750.0 in fiscal 2013 and $631.6 in fiscal 2012.

The change in cash flow from operating activities in fiscal 2014 as compared to fiscal 2013 and as compared to fiscal 2012 was

due primarily to improved working capital. Cash flow from operating activities related to changes in assets and liabilities used

in operations was a source of cash of $41.4, $208.7 and $45.5 in fiscal years 2014, 2013 and 2012, respectively. This

significant improvement in three consecutive periods was due primarily to the Company's multi-year initiative to improve

managed working capital. We define managed working capital as accounts receivable (less trade allowance in accrued

liabilities), inventory and accounts payable. The Company realized a significant improvement in accounts receivable in fiscal

2013. Cash flow from operating activities in fiscal 2014 was lower than fiscal 2013 due to less of an impact from our working

capital improvement initiative and lower net earnings.

Investing Activities

Net cash used by investing activities was $263.4, $89.1 and $94.9 in fiscal years 2014, 2013 and 2012, respectively. The

primary driver of the change in net cash used by investing activities versus the prior year was the cash used to fund the feminine

care brands acquisition in fiscal 2014. Capital expenditures were $85.3, $90.6 and $111.0 in fiscal 2014, 2013 and 2012,

respectively. These capital expenditures were funded by cash flow from operations. See Note 21 of the Notes to Consolidated

Financial Statements for capital expenditures by segment.

Capital expenditures of approximately $110 to $120 are anticipated in fiscal 2015 with a large percentage of the disbursements

for cost reduction-related capital, new products and information technology system enhancements. These estimated amounts do

not include potential expenditures related to the proposed spin-off transaction. Total capital expenditures are expected to be

financed with funds generated from operations.

Financing Activities

Net cash used by financing activities was $147.7, $377.5 and $283.3 in fiscal years 2014, 2013 and 2012, respectively. Total

debt increased approximately $54 in fiscal 2014. Share repurchases during fiscal 2014 totaled approximately $94.

Additionally, the Company paid cash dividends to common shareholders totaling approximately $124 in fiscal 2014. The

Company’s total borrowings were $2,288.4 at September 30, 2014, including $289.5 tied to variable interest rates. The

Company maintains total debt facilities of $2,603.4, of which $302.8 remains available at September 30, 2014, as reduced by

$12.2 of outstanding letters of credit.

Under the terms of the Company’s credit agreement, the ratio of the Company’s indebtedness to its earnings before interest,

taxes, depreciation and amortization (EBITDA), as defined in the agreement and detailed below, cannot be greater than 4.0 to 1,

and may not remain above 3.5 to 1 for more than four consecutive quarters. If and so long as the ratio is above 3.5 to 1 for any

period, the Company is required to pay additional interest expense for the period in which the ratio exceeds 3.5 to 1. The

interest rate margin and certain fees vary depending on the indebtedness to EBITDA ratio. Under the Company’s private

placement note agreements, indebtedness to EBITDA may not be greater than 4.0 to 1; if the ratio is above 3.5 to 1 for any

quarter, the Company is required to pay additional interest on the private placement notes of 0.75% per annum for each quarter

until the ratio is reduced to not more than 3.5 to 1. In addition, under the credit agreement, the ratio of its current year earnings

before interest and taxes (EBIT), as defined in the agreement, to total interest expense must exceed 3.0 to 1. Under the credit

agreement, EBITDA is defined as net earnings, as adjusted to add-back interest expense, income taxes, depreciation and

amortization, all of which are determined in accordance with GAAP. In addition, the credit agreement allows certain non-cash

charges such as stock award amortization and asset write-offs including, but not limited to, impairment and accelerated

depreciation, to be “added-back” in determining EBITDA for purposes of the indebtedness ratio. Severance and other cash

charges incurred as a result of restructuring and realignment activities as well as expenses incurred in acquisition integration

activities are included as reductions in EBITDA for calculation of the indebtedness ratio. In the event of an acquisition,

EBITDA is calculated on a pro forma basis to include the trailing twelve-month EBITDA of the acquired company or brands.

Total debt is calculated in accordance with GAAP, but excludes outstanding borrowings under the receivable securitization

program. EBIT is calculated in a fashion identical to EBITDA except that depreciation and amortization are not “added-back”.

Total interest expense is calculated in accordance with GAAP.

The Company’s ratio of indebtedness to its EBITDA was 2.7 to 1, and the ratio of its EBIT to total interest expense was 5.3 to

1, as of September 30, 2014. In addition to the financial covenants described above, the credit agreements and the note purchase

agreements contain customary representations and affirmative and negative covenants, including limitations on liens, sales of

assets, subsidiary indebtedness, mergers and similar transactions, changes in the nature of the business of the Company and

transactions with affiliates. If the Company fails to comply with the financial covenants referred to above or with other

43