Cigna 2008 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2008 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

101

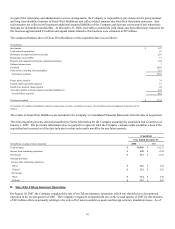

required hedge position on a real time basis. Although this hedge program does not qualify for GAAP hedge accounting, it is an

economic hedge because it is designed to and is effective in reducing equity market exposures resulting from this product. The results

of the futures contracts are included in other revenue and amounts reflecting corresponding changes in liabilities for these GMDB

contracts are included in benefits and expenses, consistent with GAAP when a premium deficiency exists.

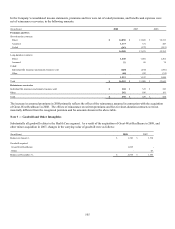

The Company had future policy benefit reserves for GMDB contracts of $1.6 billion as of December 31, 2008, and $848 million as of

December 31, 2007. The increase in reserves is primarily due to declines in the equity market driving down the value of the

underlying mutual fund investments.

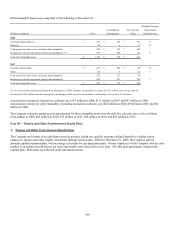

During 2008, the Company recorded additional benefits and expenses of $412 million pre-tax ($267 million after-tax) primarily to

strengthen GMDB reserves following an analysis of experience and reserve assumptions. The amounts were primarily due to:

• adverse impacts of overall market declines of $210 million pre-tax ($136 million after-tax). This is comprised of (a) $185 million

($120 million after-tax) related to the provision for partial surrenders, including $40 million ($26 million after-tax) for an increase

in the assumed election rates for future partial surrenders and (b) $25 million ($16 million after-tax) related to declines in the

values of contractholders’ non-equity investments such as bond funds, neither of which is included in the GMDB equity hedge

program;

• adverse volatility-related impacts due to turbulent equity market conditions. Volatility risk is not covered by the GMDB equity

hedge program. Also, the equity market volatility, particularly during the second half of the year impacted the effectiveness of

the hedge program. In aggregate, these volatility-related impacts totaled $182 million of the pre-tax charge ($118 million after-

tax). The GMDB equity hedge program is designed so that changes in the value of a portfolio of actively managed futures

contracts will offset changes in the liability resulting from equity market movements. In periods of equity market declines, the

liability will increase; the hedge program is designed to produce gains on the futures contracts to offset the increase in the

liability. However, the hedge program will not perfectly offset the change in the liability, in part because the market does not

offer futures contracts that exactly match the diverse mix of equity fund investments held by contractholders, and because there is

a time lag between changes in underlying contractholder mutual funds, and corresponding changes in the hedge position. In 2008,

the impact of this mismatch was higher than most prior periods due to the relatively large changes in market indices from day to

day. In addition, the number of futures contracts used in the hedge program is adjusted only when certain tolerances are exceeded

and in periods of highly volatile equity markets when actual volatility exceeds the expected volatility assumed in the liability

calculation, losses will result. These conditions have had an adverse impact on earnings, and during 2008, the increase in the

liability due to equity market movements was only partially offset by the results of the futures contracts; and

• adverse interest rate impacts. Interest rate risk is not covered by the GMDB equity hedge program, and the interest rate returns on

the futures contracts were less than the Company’s long-term assumption for mean investment performance generating $14

million of the pre-tax charge ($9 million after-tax).

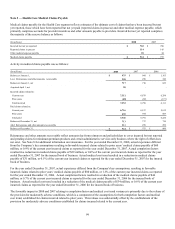

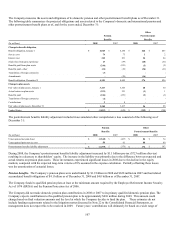

Management estimates reserves for GMDB exposures based on assumptions regarding lapse, partial surrender, mortality, interest rates

(mean investment performance and discount rate) and volatility. These assumptions are based on the Company’s experience and

future expectations over the long-term period. The Company monitors actual experience to update these reserve estimates as

necessary.

Lapse refers to the full surrender of an annuity prior to a contractholder’s death. Partial surrender refers to the fact that most

contractholders have the ability to withdraw substantially all of their mutual fund investments while retaining the death benefit

coverage in effect at the time of the withdrawal. Mean investment performance refers to market rates to be earned over the life of the

GMDB equity hedge program and market volatility refers to market fluctuations.

The determination of liabilities for GMDB requires the Company to make critical accounting estimates. The Company regularly

evaluates the assumptions used in establishing reserves and changes its estimates if actual experience or other evidence suggests that

earlier assumptions should be revised. If actual experience differs from the assumptions (including lapse, partial surrender, mortality,

interest rates and volatility) used in estimating these reserves, the resulting change could have a material adverse effect on the

Company’s consolidated results of operations, and in certain situations, could have a material adverse effect on the Company’s

financial condition.

The following provides information about the Company’s reserving methodology and assumptions for GMDB as of December 31,

2008:

• The reserves represent estimates of the present value of net amounts expected to be paid, less the present value of net future

premiums. Included in net amounts expected to be paid is the excess of the guaranteed death benefits over the values of the

contractholders’ accounts (based on underlying equity and bond mutual fund investments).