Capital One 2001 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2001 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70

|

|

could have a material effect on the Company's consolidated financial

statements. Additionally, the regulators have broad discretion in

applying higher capital requirements. Regulators consider a range of

factors in determining capital adequacy, such as an institution's size,

quality and stability of earnings, interest rate risk exposure, risk

diversification, management expertise, asset quality, liquidity and

internal controls.

The most recent notifications received from the regulators categorized

the Bank and the Savings Bank as “well-capitalized.” To be categorized

as “well-capitalized,” the Bank and the Savings Bank must maintain

minimum capital ratios as set forth in the following table. As of

December 31, 2001, there were no conditions or events since the

notifications discussed above that management believes would have

changed either the Bank or the Savings Bank's capital category.

In November 2001, the four federal banking agencies (the “Agencies”)

adopted an amendment to the regulatory capital standards regarding

the treatment of certain recourse obligations, direct credit substitutes

(i.e., guarantees on third-party assets), residual interests in asset

securitizations, and other securitized transactions that expose

institutions primarily to credit risk. Effective January 1, 2002, this rule

amends the Agencies' regulatory capital standards to create greater

differentiation in the capital treatment of residual interests. Based on

the Company's analysis of the rule adopted by the Agencies, we do not

anticipate any material changes to our regulatory capital ratios when

the rule becomes effective.

On January 31, 2001, the Agencies issued “Expanded Guidance for

Subprime Lending Programs” (the “Guidelines”). The Guidelines,

while not constituting a formal regulation, provide guidance to the

federal bank examiners regarding the adequacy of capital and loan loss

reserves held by insured depository institutions engaged in subprime

lending. The Guidelines adopt a broad definition of “subprime” loans

which likely covers more than one-third of all consumers in the United

States. Because the Company’s business strategy is to provide credit

card products and other consumer loans to a wide range of consumers,

the examiners may view a portion of the Company’s loan assets as

“subprime.” Thus, under the Guidelines, bank examiners could require

the Bank or the Savings Bank to hold additional capital (up to one and

one-half to three times the minimally required level of capital, as set

forth in the Guidelines), or additional loan loss reserves, against such

assets. As described above, at December 31, 2001 the Bank and the

Savings Bank each met the requirements for a “well-capitalized”

institution, and management believes that each institution is holding

an appropriate amount of capital or loan loss reserves against higher

risk assets. Management also believes we have general risk

management practices in place that are appropriate in light of our

business strategy. Significantly increased capital or loan loss reserve

requirements, if imposed, however, could have a material impact on

the Company's consolidated financial statements.

In August 2000, the Bank received regulatory approval and established

a subsidiary bank in the United Kingdom. In connection with the

approval of its former branch office in the United Kingdom, the

Company committed to the Federal Reserve that, for so long as the

Bank maintains a branch or subsidiary bank in the United Kingdom,

the Company will maintain a minimum Tier 1 Leverage ratio of 3.0%.

As of December 31, 2001 and 2000, the Company's Tier 1 Leverage

ratio was 11.93% and 11.14%, respectively.

Additionally, certain regulatory restrictions exist that limit the ability of

the Bank and the Savings Bank to transfer funds to the Corporation.

As of December 31, 2001, retained earnings of the Bank and the

Savings Bank of $864,500 and $99,800, respectively, were available for

payment of dividends to the Corporation without prior approval by

the regulators. The Savings Bank, however, is required to give the OTS

at least 30 days advance notice of any proposed dividend and the OTS,

in its discretion, may object to such dividend.

Note L

Commitments and Contingencies

As of December 31, 2001, the Company had outstanding lines of credit

of approximately $142,600,000 committed to its customers. Of that

total commitment, approximately $97,400,000 was unused. While this

amount represented the total available lines of credit to customers, the

Company has not experienced, and does not anticipate, that all of its

customers will exercise their entire available line at any given point in

time. The Company generally has the right to increase, reduce, cancel,

alter or amend the terms of these available lines of credit at any time.

58 notes

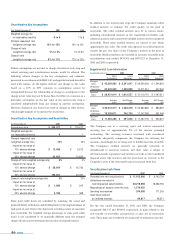

To Be “ Well-

Capitalized”

Minimum For Under Prompt

Capital Corrective

Adequacy Action

Ratios Purposes Provisions

December 31, 2001

Capital One Bank

Tier 1 Capital 12.95% 4.00% 6.00%

Total Capital 15.12 8.00 10.00

Tier 1 Leverage 12.09 4.00 5.00

Capital One, F.S.B.

Tier 1 Capital 9.27% 4.00% 6.00%

Total Capital 11.21 8.00 10.00

Tier 1 Leverage 8.86 4.00 5.00

December 31, 2000

Capital One Bank

Tier 1 Capital 9.30% 4.00% 6.00%

Total Capital 11.38 8.00 10.00

Tier 1 Leverage 10.02 4.00 5.00

Capital One, F.S.B.

Tier 1 Capital 8.24% 4.00% 6.00%

Total Capital 10.90 8.00 10.00

Tier 1 Leverage 6.28 4.00 5.00