Capital One 2001 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2001 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

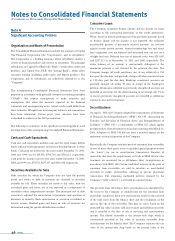

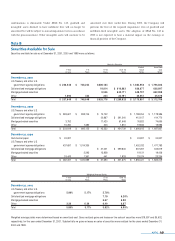

estimated excess finance charges and past-due fees over the sum of the

return paid to security holders, estimated contractual servicing fees

and credit losses. The Company periodically reviews the key

assumptions and estimates used in determining the interest-only strip.

Decreases in fair values below the carrying amount as a result of

changes in the key assumptions are recognized in servicing and

securitizations income, while increases in fair values as a result of

changes in key assumptions are recorded as unrealized gains.

Unrealized gains are included as a component of cumulative other

comprehensive income, on a net-of-tax basis, in accordance with the

provisions of SFAS No. 115, “Accounting for Certain Investments in

Debt and Equity Securities.” In accordance with EITF 99-20,

“Recognition of Interest Income and Impairment of Purchased and

Retained Beneficial Interests in Securitized Financial Assets,” the

interest component of cash flows attributable to retained interests in

securitizations is recorded in other interest income. See further

discussion of off-balance sheet securitizations in Note N to the

Consolidated Financial Statements.

Tr ansfers of receivables that do not meet the requirements of SFAS 140

for sales treatment are treated as secured borrowings, with the

transferred receivables remaining in consumer loans and the related

liability recorded in other borrowings. See discussion of secured

borrowings in Note E to the Consolidated Financial Statements.

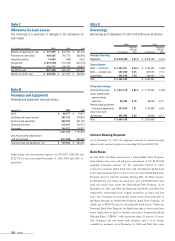

Allowance for Loan Losses

The allowance for loan losses is maintained at the amount estimated to

be sufficient to absorb probable losses, net of recoveries (including

recovery of collateral), inherent in the existing reported loan portfolio.

The provision for loan losses is the periodic cost of maintaining an

adequate allowance. The amount of allowance necessary is determined

primarily based on a migration analysis of delinquent and current

accounts. In evaluating the sufficiency of the allowance for loan losses,

management also takes into consideration the following factors: recent

trends in delinquencies and charge-offs including bankrupt, deceased

and recovered amounts; historical trends in loan volume; forecasting

uncertainties and size of credit risks; the degree of risk inherent in the

composition of the loan portfolio; economic conditions; credit

evaluations and underwriting policies.

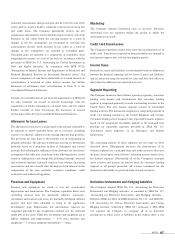

Premises and Equipment

Premises and equipment are stated at cost less accumulated

depreciation and amortization. The Company capitalizes direct costs

(including external costs for purchased software, contractors,

consultants and internal staff costs) for internally developed software

projects that have been identified as being in the application

development stage. Depreciation and amortization expenses are

computed generally by the straight-line method over the estimated

useful lives of the assets. Useful lives for premises and equipment are as

follows: buildings and improvements — 5-39 years; furniture and

equipment — 3-10 years;computers and software — 3 years.

Marketing

The Company expenses marketing costs as incurred. Television

advertising costs are expensed during the period in which the

advertisements are aired.

Credit Card Fraud Losses

The Company experiences fraud losses from the unauthorized use of

credit cards. Transactions suspected of being fraudulent are charged to

non-interest expense after a 60-day investigation period.

Income Taxes

Deferred tax assets and liabilities are determined based on differences

between the financial reporting and tax bases of assets and liabilities,

and are measured using the enacted tax rates and laws that will be in

effect when the differences are expected to reverse.

Segment Reporting

The Company maintains three distinct operating segments: consumer

lending, auto finance and international. The consumer lending

segment is comprised primarily of credit card lending activities in the

United States. The auto finance segment consists of automobile

lending activities. The international segment is comprised primarily of

credit card lending activities in the United Kingdom and Canada.

Consumer lending is the Company's only reportable business segment,

based on the quantitative thresholds applied to the managed loan

portfolio for reportable segments provided in SFAS No. 131,

"Disclosures about Segments of an Enterprise and Related

Information."

The accounting policies of these segments are the same as those

described above. Management measures the performance of its

business segments on a managed basis and makes resource allocation

decisions based upon several factors, including income before taxes,

less indirect expenses. Substantially all of the Company's managed

assets, revenue and income are derived from the consumer lending

segment in all periods presented. All revenue considered for the

quantitative thresholds are generated from external customers.

Derivative Instruments and Hedging Activities

The Company adopted SFAS No. 133, “Accounting for Derivative

Instruments and Hedging Activities,” as amended by SFAS No. 137,

“Accounting for Derivative Instruments and Hedging Activities –

Deferral of Effective Date of FASB Statement No. 133,” and SFAS No.

138, “Accounting for Certain Derivative Instruments and Certain

Hedging Activities,” (collectively,“SFAS 133”) on January 1, 2001. SFAS

133 required the Company to recognize all of its derivative

instruments as either assets or liabilities in the balance sheet at fair

notes 47