Capital One 2001 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2001 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

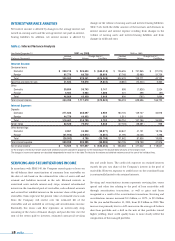

The amount of marketing expense allocated to various products or

businesses will influence the characteristics of our portfolio as various

products or businesses are characterized by different account growth,

loan growth and asset quality characteristics. Due in part to an increase

in our marketing efforts across the entire credit spectrum, we currently

expect continued strong loan growth in 2002, but expect account

growth, while remaining strong, to moderate compared to recent

quarters. Actual growth, however, may vary significantly depending on

our actual product mix and the level of attrition in our managed

portfolio, which is primarily affected by competitive pressures. Also

primarily as a result of our continued growth in superprime lending,

our increased offerings of introductory rate products, and an increase

in the Company’s liquidity portfolio during the fourth quarter, our net

interest margin decreased during 2001. We anticipate that net interest

margin may continue to fluctuate during 2002, based on continued

movement in the underlying components and due in part to the

scheduled repricing of certain introductory rate credit card products as

well as continuing shifts in our asset mix.

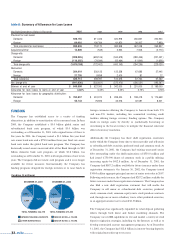

Impact of Delinquencies, Charge-Offs and Attrition

Our earnings are particularly sensitive to delinquencies and charge-offs

on our portfolio, and to the level of attrition resulting from

competition in the credit card industry. As delinquency levels fluctuate,

the resulting amount of past due and overlimit fees, which are

significant sources of our revenue, will also fluctuate. Further, the

timing of revenues from increasing or decreasing delinquencies

precedes the related impact of higher or lower charge-offs that

ultimately result from varying levels of delinquencies. Delinquencies

and net charge-offs are impacted by general economic trends in

consumer credit performance, including bankruptcies, the degree of

seasoning of our portfolio and our product mix.

As of December 31, 2001, we had the lowest managed net charge-off

rate among the top ten credit card issuers in the United States.

However, we expect delinquencies and charge-offs to increase in 2002,

primarily due to the continued seasoning of certain accounts, as well as

general economic factors. We caution that delinquency and charge-off

levels are not always predictable and may vary from projections and

from period to period. During an economic downturn or recession,

delinquencies and charge-offs are likely to increase more quickly. This

impact could be exacerbated by a decline in the loan growth rate. In

addition, competition in the credit card industry, as measured by the

volume of mail solicitations, remains very high. Competition can affect

our earnings by increasing attrition of our outstanding loans (thereby

reducing interest and fee income) and by making it more difficult to

retain and attract profitable customers.

Cautionary Factors

The strategies and objectives outlined above, and the other forward-

looking statements contained in this section, involve a number of risks

and uncertainties. Capital One cautions readers that any forward-

looking information is not a guarantee of future performance and that

actual results could differ materially. In addition to the factors

discussed above, among the other factors that could cause actual

results to differ materially are the following: continued intense

competition from numerous providers of products and services that

compete with our businesses; with respect to financial and other

products, changes in our aggregate accounts or consumer loan

balances and the growth rate thereof, including changes resulting from

factors such as shifting product mix, amount of our actual marketing

expenses and attrition of accounts and loan balances; any significant

disruption of, or loss of public confidence in, the U.S. mail system

affecting response rates or customer payments; an increase in credit

losses (including increases due to a worsening of general economic

conditions); our ability to continue to securitize our credit cards and

consumer loans and to otherwise access the capital markets at

attractive rates and terms to fund our operations and future growth;

difficulties or delays in the development, production, testing and

marketing of new products or services; losses associated with new

products or services or expansion internationally; financial, legal,

regulatory or other difficulties that may affect investment in, or the

overall performance of, a product or business, including changes in

existing laws to regulate further the credit card and consumer loan

industry and the financial services industry, in general, including the

flexibility of financial services companies to obtain, use and share

consumer data; the amount of, and rate of growth in, our expenses

(including salaries and associate benefits and marketing expenses) as

our business develops or changes or as we expand into new market

areas; the availability of capital necessary to fund our new businesses;

our ability to build the operational and organizational infrastructure

necessary to engage in new businesses or to expand internationally;

our ability to recruit experienced personnel to assist in the

management and operations of new products and services; and other

factors listed from time to time in the our SEC reports, including, but

not limited to, the Annual Report on Form 10-K for the year ended

December 31, 2001 (Part I, Item 1, Risk Factors).

38 md&a