Berkshire Hathaway 2001 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2001 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

|

|

57

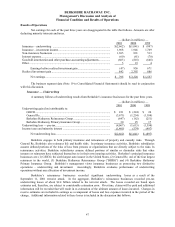

Goodwill amortization and other purchase-accounting adjustments

Goodwill amortization and other purchase-accounting adjustments reflect the after-tax effect on net

earnings with respect to the amortization of goodwill of acquired businesses and the amortization of fair value

adjustments to certain assets and liabilities which were recorded at the business acquisition dates. Amortization of

goodwill was $572 million in 2001, $715 million in 2000 and $477 million in 1999. Goodwill amortization in 2000

included a charge of $219 million to write-off the remaining goodwill related to Dexter Shoe (see Note 1(g) to the

Consolidated Financial Statements).

As a result of new accounting standards issued by the FASB in June 2001, accounting for goodwill has

changed. Goodwill arising from business acquisitions completed after July 1, 2001 is not subject to systematic

amortization. In addition, the systematic amortization of goodwill related to businesses acquired before June 30,

2001 will be discontinued effective January 1, 2002. The new accounting standards require that goodwill of

acquired businesses continue to be tested for impairment. Berkshire has not fully completed an assessment of the

new standards, however, adoption of the new standards is expected to have a significant impact on earnings.

Other purchase-accounting adjustments consist primarily of the amortization of the excess market value

over the historical cost of fixed maturity investments that existed as of the date of certain business acquisitions.

Such excess is included in Berkshire’ s cost of the investments and is being amortized over the estimated remaining

lives of the assets. The unamortized excess remaining in the cost of fixed maturity investments was $565 million at

December 31, 2001, $680 million at December 31, 2000 and $940 million at December 31, 1999.

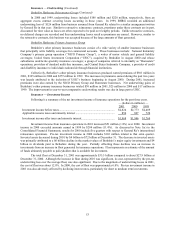

Realized Investment Gain

Realized investment gain has been a recurring element in Berkshire's net earnings for many years. The

amount — recorded when investments are sold, other-than-temporarily impaired or in certain situations, as required

by GAAP, when investments are marked-to-market with the corresponding gain or loss included in earnings — may

fluctuate significantly from period to period, with a meaningful effect upon Berkshire's consolidated net earnings.

However, the amount of realized investment gain or loss for any given period has no predictive value, and

variations in amount from period to period have no practical analytical value, particularly in view of the net

unrealized price appreciation now existing in Berkshire's consolidated investment portfolio.

While the effects of realized gains are often material to the Consolidated Statements of Earnings, such

gains often produce a minimal impact on Berkshire's total shareholders' equity. This is due to the fact that

Berkshire's investments are carried in prior periods' Consolidated Financial Statements at market value with

unrealized gains, net of tax, reported as a separate component of shareholders' equity.

Market Risk Disclosures

Berkshire's Consolidated Balance Sheet includes a substantial amount of assets and liabilities whose fair

values are subject to market risks. Berkshire’ s significant market risks are primarily associated with interest rates

and equity prices and to a lesser degree financial products. The following sections address the significant market

risks associated with Berkshire's business activities.

Interest Rate Risk

This section discusses interest rate risks associated with Berkshire’ s financial assets and liabilities.

Berkshire's management prefers to invest in equity securities or to acquire entire businesses based upon the

principles discussed in the following section on equity price risk. When unable to do so, management may

alternatively invest in bonds or other interest rate sensitive instruments. Berkshire's strategy is to acquire securities

that are attractively priced in relation to the perceived credit risk. Management recognizes and accepts that losses

may occur. Berkshire has historically utilized a modest level of corporate borrowings and debt. Further, Berkshire

strives to maintain the highest credit ratings so that the cost of debt is minimized. Berkshire utilizes derivative

products to manage interest rate risks to a very limited degree.

The fair values of Berkshire's fixed maturity investments and borrowings under investment agreements,

notes payable and other debt will fluctuate in response to changes in market interest rates. Increases and decreases

in prevailing interest rates generally translate into decreases and increases in fair values of those instruments.

Additionally, fair values of interest rate sensitive instruments may be affected by the credit worthiness of the issuer,

prepayment options, relative values of alternative investments, the liquidity of the instrument and other general

market conditions.