Berkshire Hathaway 2001 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2001 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

48

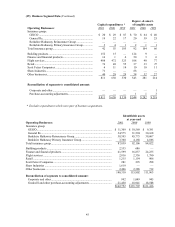

Management's Discussion (Continued)

Insurance — Underwriting (Continued)

A significant marketing strategy followed by all these businesses is the maintenance of extraordinary capital

strength. Statutory surplus as regards policyholders of Berkshire’ s insurance businesses totaled approximately

$27.2 billion at December 31, 2001. This superior capital strength creates opportunities, especially with respect to

reinsurance activities, to negotiate and enter into contracts of insurance specially designed to meet unique needs of

sophisticated insurance and reinsurance buyers. Additional information regarding Berkshire’ s insurance and

reinsurance operations follows.

GEICO

GEICO provides primarily private passenger automobile coverages to insureds in 48 states and the District

of Columbia. GEICO policies are marketed mainly by direct response methods in which customers apply for

coverage directly to the company over the telephone, through the mail or via the Internet. This is a significant

element in GEICO’ s strategy to be a low cost insurer and, yet, provide high value to policyholders.

GEICO's underwriting results for the past three years are summarized below.

— (dollars in millions) —

2001 2000 1999

Amount %Amount %Amount %

Premiums written ...................................................... $6,176 $5,778 $4,953

Premiums earned....................................................... $6,060 100.0 $5,610 100.0 $4,757 100.0

Losses and loss expenses .......................................... 4,842 79.9 4,809 85.7 3,815 80.2

Underwriting expenses.............................................. 997 16.5 1,025 18.3 918 19.3

Total losses and expenses.......................................... 5,839 96.4 5,834 104.0 4,733 99.5

Underwriting gain (loss) — pre-tax .......................... $ 221 $ (224) $ 24

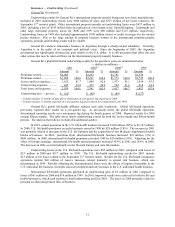

Premiums earned by GEICO in 2001 totaled $6,060 million, an 8.0% increase over 2000. Premiums

earned in 2000 exceeded premiums earned in 1999 by 17.9%. The growth in premiums earned during 2001 reflects

increased rates, partially offset by a slight reduction in policies-in-force. In response to the underwriting losses of

2000, GEICO implemented rate increases in many states and tightened underwriting resulting in the much improved

underwriting results in 2001.

Voluntary auto policies-in-force at December 31, 2001 declined 0.8% from December 31, 2000. In

comparison, voluntary policies-in-force increased 8.5% during 2000 and 21.5% during 1999. During 2001,

policies-in-force increased 1.6% in the preferred risk auto market and decreased 10.1% in the standard and

nonstandard auto lines. Voluntary auto new business sales in 2001 decreased 30.2% from 2000 due to decreased

advertising and a lower closure ratio.

Losses and loss adjustment expenses incurred increased 0.7% to $4,842 million in 2001. The loss ratio for

property and casualty insurance, which measures the portion of premiums earned that is paid or reserved for losses and

related claims handling expenses, was 79.9% in 2001 compared to 85.7% in 2000. The lower ratio reflects the effect of

premium rate increases and tightened underwriting standards. Additionally, the rate of increase in claim severity (the

cost per claim) slowed in 2001 and the frequency of accidents decreased in many coverages compared to the prior year.

The mild winter weather conditions during the fourth quarter of 2001 also contributed to the relatively low loss ratio.

Catastrophe losses added slightly less than 1 point to the loss ratio in each of the past three years.

GEICO’ s insurance subsidiaries are defendants in a number of class action lawsuits related to the use of

replacement repair parts not produced by the original auto manufacturer, the calculation of “total loss” value and

whether to pay diminished value as part of the settlement of certain claims. Management intends to vigorously

defend GEICO’ s position on these claim settlement procedures. However, these lawsuits are in various stages of

development and the ultimate outcome cannot be reasonably determined.

Underwriting expenses incurred in 2001 decreased $28 million (2.7%) from 2000, following an increase of

$107 million (11.7%) in 2000 over 1999. Advertising expense declined significantly in 2001 from 2000 following a

large increase in 2000 over 1999. Although advertising expense declined in 2001, the unit cost of acquiring new

business continued to increase in 2001 as fewer new policies were written in relation to quotes. Other underwriting

expenses for 2001 also reflect lower profit sharing expense in 2001.

Throughout 2001, GEICO focused on improving underwriting profitability, but did so at the expense of

growth. Entering 2002, rates are believed to be adequate in nearly all states and GEICO is in a better position to grow

as many competitors are expected to take rate increases.