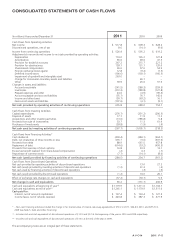

Avon 2011 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2011 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

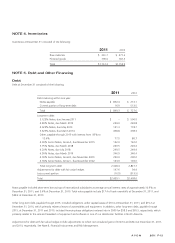

is being amortized over the life of the new 4.625% Notes. The carrying value of the 4.625% Notes represents the $125.0 principal amount,

net of the unamortized discount to face value and the premium related to the call option associated with the original notes totaling $3.7 at

December 31, 2011, and $6.3 at December 31, 2010.

The indentures and note purchase agreement under which the above notes were issued contain certain covenants, including limits on the

incurrence of liens and restrictions on the incurrence of sale/leaseback transactions and transactions involving a merger, consolidation or sale

of substantially all of our assets. At December 31, 2011, we were in compliance with all covenants in our indentures and note purchase

agreement. Such indentures and note purchase agreement do not contain any rating downgrade triggers that would accelerate the maturity

of our debt. However, we would be required to make an offer to repurchase the 2013 Notes, 2014 Notes, 2018 Notes, 2019 Notes, the

Series A Notes, the Series B Notes and the Series C Notes at a price equal to 101% of their aggregate principal amount, plus accrued and

unpaid interest in the event of a change in control involving Avon and a corresponding ratings downgrade to below investment grade.

Annual maturities of long-term debt (including unamortized discounts and premiums and excluding the adjustments for debt with fair value

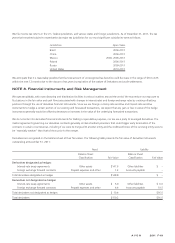

hedges) outstanding at December 31, 2011, are as follows:

2012 2013 2014 2015 2016

After

2017 Total

Maturities $16.9 $384.8 $509.1 $148.5 $5.9 $1,272.3 $2,337.5

Other Financing

We maintain a three-year, $1 billion revolving credit and competitive advance facility (“Credit Facility”), which expires in November 2013.

The interest rate on borrowings under this credit facility is based on LIBOR plus the appropriate margin reflecting our credit default swap rate

with a minimum and maximum based on our credit rating (the “CDS Spread”). The Credit Facility also allows for borrowing at an interest

rate based on the CDS Spread minus 1%, but not less than 0% per annum, plus the highest of prime, .5% plus the federal funds rate, or

1% plus one month LIBOR. The Credit Facility has an annual fee of $1.7, payable quarterly, based on our current credit ratings. The Credit

Facility contains various covenants, including a financial covenant that requires our interest coverage ratio (determined in relation to our

consolidated pretax income and interest expense) to equal or exceed 4:1. The Credit Facility also provides for possible increases by up to an

aggregate incremental principal amount of $250.0, subject to the consent of the affected lenders under the Credit Facility. The Credit

Facility may be used for general corporate purposes. There were no amounts outstanding under the Credit Facility at December 31, 2011, or

December 31, 2010.

We maintain a $1 billion commercial paper program. Under the program, we may issue from time to time unsecured promissory notes in the

commercial paper market in private placements exempt from registration under federal and state securities laws, for a cumulative face

amount not to exceed $1 billion outstanding at any one time and with maturities not exceeding 270 days from the date of issue. The

commercial paper short-term notes issued under the program are not redeemable prior to maturity and are not subject to voluntary

prepayment. The commercial paper program is supported by our three-year $1 billion revolving credit and competitive advance facility.

Outstanding commercial paper effectively reduces the amount available for borrowing under this credit facility. At December 31, 2011, there

was $709.0 outstanding under the commercial paper program.

At December 31, 2011 and December 31, 2010, we also had letters of credit outstanding totaling $23.4 and $16.4, respectively, which

primarily guarantee various insurance activities. In addition, we had outstanding letters of credit for trade activities and commercial

commitments executed in the ordinary course of business, such as purchase orders for normal replenishment of inventory levels.

A V O N 2011 F-15